|

시장보고서

상품코드

2038696

물류 자동화 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Logistics Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

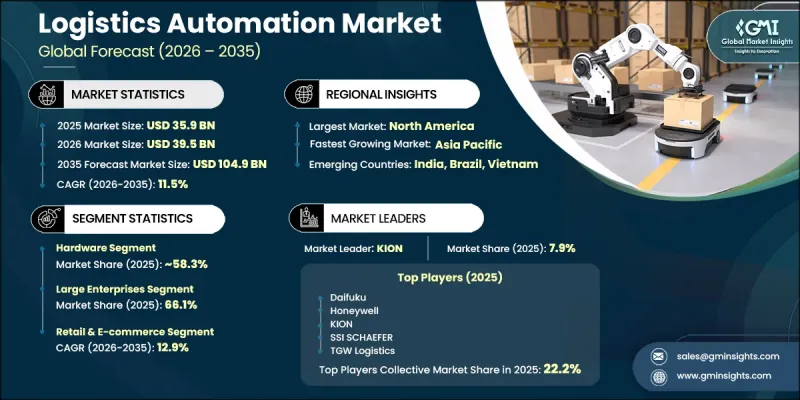

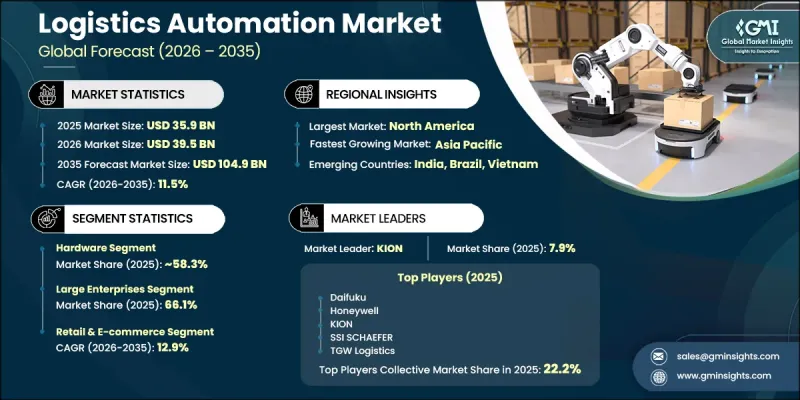

세계의 물류 자동화 시장은 2025년에 359억 달러로 평가되었고, CAGR 11.5%로 성장할 전망이며, 2035년까지 1,049억 달러에 이를 것으로 예측됩니다.

이러한 시장 확대는 물류가 각국 경제에서 전략적으로 중요한 위치를 차지하고 있기 때문입니다. 물류는 많은 국가에서 국내총생산(GDP)에 크게 기여하고 있기 때문입니다. 정부와 이해관계자들은 생산성, 효율성, 그리고 국제 경쟁력을 높이기 위해 물류 인프라 구축에 점점 더 많은 투자를 하고 있습니다. 또한, 미국 경제 통계를 추적하는 연방 통계 당국이 지적한 바와 같이, 물류 및 운송은 미국 경제의 생산량에서 핵심적인 요소를 형성하고 있습니다. 현대의 물류 업무는 빠르게 지능형 자동화로 전환되고 있으며, AI와 머신러닝 기술은 고립된 최적화 도구에서 완전히 통합된 오케스트레이션 시스템으로 진화하고 있습니다. 이러한 플랫폼은 현재 재고, 인력, 운송을 실시간으로 조정하여 엔드투엔드 워크플로우를 관리하고 있습니다. 창고 관리 및 실행 시스템은 업무 수요와 시스템 부하에 따라 자율 주행 로봇, 작업자, 자동화 스테이션에 동적으로 작업을 할당합니다. 운송 관리 시스템에서는 교통 상황, 운송업체 가동 상황 등 실시간 데이터 입력을 활용하여 경로 결정을 최적화하는 사례가 늘고 있습니다. 또한, 조사 결과에 따르면, 효과적인 시스템 통합과 인력 적응이 동반된다면 자동화 수준과 로봇 도입 밀도를 높여 업무 효율성이 크게 향상될 수 있는 것으로 나타났습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 359억 달러 |

| 예측 시장 규모 | 1,049억 달러 |

| CAGR | 11.5% |

2025년에는 하드웨어 부문이 58.3%의 점유율을 차지했으며, 210억 달러 시장 규모를 창출할 것으로 예측됩니다. 이는 컨베이어, 자동 창고 시스템(AS/RS), 팔레타이징 장치, 자율 이동 로봇, 무인 운반차(AGV), 로봇식 리프트 설비 등 물리적 자동화 인프라가 자본 집약적이기 때문입니다. 하드웨어는 여전히 물류 자동화의 기반 계층이며, 소프트웨어 통합에 앞서 많은 선행 투자가 필요합니다. 이러한 시스템은 창고 관리 및 실행 플랫폼과 밀접하게 통합되어 있으며, 경로 효율성, 작업 부하 분산 및 예측 유지 보수 기능을 강화하기 위해 점점 더 많은 인공지능을 통합하고 있습니다.

2025년 기준 대기업 부문은 66.1%의 점유율을 차지했으며, 시장 규모는 238억 달러에 달했습니다. 이러한 선도적 지위는 대규모 자동화 도입에 따른 막대한 자본 수요로 인해 일반적으로 재무구조가 탄탄한 조직에서만 도입이 가능하기 때문입니다. 주요 도입 기업으로는 여러 시설에 걸쳐 운영되는 세계 소매 체인, 주요 전자상거래 기업, 제3자 물류 제공업체 등이 있습니다. 이들 기업은 장기적인 투자 주기를 관리하고 분산된 창고 네트워크 전체에 고도의 자동화 기술을 도입하는 데 유리한 위치에 있으며, 소규모 시장 진출기업보다 분명한 우위를 점하고 있습니다.

미국의 물류 자동화 시장은 2025년 109억 달러에 달했으며, 2026-2035년 연평균 12.3%의 성장률을 보일 것으로 예측됩니다. 중국의 고도로 발달한 물류 생태계는 자동화 기술에 대한 강력한 투자를 지속적으로 유치하고 있습니다. 이러한 성장은 전자상거래의 급속한 성장, 창고업의 노동력 부족, 그리고 로봇공학 및 AI 기반 시스템의 광범위한 도입에 의해 뒷받침되고 있습니다. 업계 조사에 따르면, 이 지역 물류 의사결정권자의 상당수가 인공지능에 대한 의존도가 높아질 것으로 예상하는 한편, 자동화된 공급망의 사이버 보안 위험에 대한 우려도 커지고 있는 것으로 나타났습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 컴포넌트별(2022-2035년)

제6장 시장 추산 및 예측 : 용도별(2022-2035년)

제7장 시장 추산 및 예측 : 기업 규모별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.11The Global Logistics Automation Market was valued at USD 35.9 billion in 2025 and is estimated to grow at a CAGR of 11.5% to reach USD 104.9 billion by 2035.

The market expansion is influenced by the strategic importance of logistics in national economies, as it significantly contributes to gross domestic product (GDP) across multiple countries. Governments and private stakeholders are increasingly investing in upgrading logistics infrastructure to improve productivity, efficiency, and global competitiveness. Logistics and transportation also form a core component of economic output in the United States, as highlighted by federal statistical authorities responsible for national economic data tracking. Modern logistics operations are rapidly shifting toward intelligent automation, where AI and machine learning technologies are evolving from isolated optimization tools into fully integrated orchestration systems. These platforms now manage end-to-end workflows by coordinating inventory, labor, and transportation in real time. Warehouse management and execution systems dynamically assign tasks across autonomous mobile robots, manual workers, and automated stations based on operational demand and system load. Transportation management systems are increasingly using live data inputs such as traffic conditions and carrier availability to optimize routing decisions. Research findings also indicate that higher levels of automation and robotics density significantly improve operational efficiency when supported by effective system integration and workforce adaptation.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $35.9 Billion |

| Forecast Value | $104.9 Billion |

| CAGR | 11.5% |

The hardware segment accounted for 58.3% share in 2025, generating USD 21 billion attributed to the capital-intensive nature of physical automation infrastructure, including conveyors, automated storage and retrieval systems, palletizing units, autonomous mobile robots, automated guided vehicles, and robotic lift equipment. Hardware remains the foundational layer of logistics automation, requiring significant upfront investment before software integration. These systems are closely integrated with warehouse control and execution platforms, which increasingly incorporate artificial intelligence to enhance routing efficiency, workload distribution, and predictive maintenance capabilities.

The large enterprises segment held a 66.1% share in 2025, valued at USD 23.8 billion. This leadership position is driven by the high capital requirements associated with large-scale automation deployments, which are typically accessible to financially strong organizations. Major adopters include global retail chains, e-commerce leaders, and third-party logistics providers that operate across multiple facilities. These enterprises are better positioned to manage long investment cycles and implement advanced automation technologies across distributed warehouse networks, giving them a clear advantage over smaller market participants.

U.S. Logistics Automation Market reached USD 10.9 billion in 2025 and is projected to grow at a CAGR of 12.3% from 2026 to 2035. The country's highly developed logistics ecosystem continues to attract strong investments in automation technologies. Growth is supported by rapid expansion of e-commerce, increasing labor shortages in warehouse operations, and widespread adoption of robotics and AI-driven systems. Industry surveys indicate that a significant share of logistics decision-makers in the region expect growing reliance on artificial intelligence while also highlighting rising concerns around cybersecurity risks in automated supply chains.

Key companies operating in the Logistics Automation Industry include ABB, Honeywell, Daifuku, KION (Dematic), SSI SCHAEFER, KUKA, Korber, KNAPP, TGW Logistics, and Symbotic. Companies in the Logistics Automation Market are focusing on expanding their technology portfolios by integrating advanced artificial intelligence, machine learning, and robotics into end-to-end supply chain solutions. Many players are investing heavily in scalable automation systems that support flexible warehouse configurations and real-time decision-making capabilities. Strategic partnerships with e-commerce platforms, logistics service providers, and industrial operators are helping firms expand deployment opportunities across multiple sectors. Companies are also prioritizing software-hardware integration to improve system interoperability and operational efficiency. In addition, continuous investment in predictive analytics, digital twin technologies, and cloud-based warehouse management systems is strengthening performance optimization.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Application

- 2.2.4 Organization Size

- 2.2.5 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-Commerce Growth & Last-Mile Delivery Demands

- 3.2.1.2 Labor Shortage & Rising Operational Costs

- 3.2.1.3 Need for Real-Time Visibility & Supply Chain Resilience

- 3.2.1.4 Advancements in AI, IoT & Robotics Technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Capital Investment & ROI Uncertainties

- 3.2.2.2 Integration Complexity with Legacy Systems

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging Markets Adoption in Asia Pacific & Latin America

- 3.2.3.2 SME Market Penetration Through Cloud-Based Solutions

- 3.2.3.3 Autonomous Vehicles & Drone Delivery Integration

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technologies

- 3.3.1.1 Radio Frequency Identification (RFID)

- 3.3.1.2 Automated Storage and Retrieval Systems (AS/RS)

- 3.3.1.3 Robotic Process Automation (RPA)

- 3.3.2 Emerging technologies

- 3.3.2.1 Autonomous Mobile Robots (AMRs)

- 3.3.2.2 Artificial Intelligence (AI)-Driven Predictive Logistics Platforms

- 3.3.2.3 Drone-Based Delivery Systems

- 3.3.2.4 Digital Twins for Supply Chain Optimization

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 US - Federal Motor Carrier Safety Administration (FMCSA)

- 3.5.1.2 US - Occupational Safety and Health Administration (OSHA)

- 3.5.1.3 Canada - Transport Canada

- 3.5.2 Europe

- 3.5.2.1 EU - Directorate-General for Mobility and Transport (DG MOVE)

- 3.5.2.2 Germany - Federal Ministry for Digital and Transport (BMDV)

- 3.5.3 Asia Pacific

- 3.5.3.1 China - China Federation of Logistics & Purchasing (CFLP)

- 3.5.3.2 India - Directorate of Logistics (DoL)

- 3.5.4 Latin America

- 3.5.4.1 Brazil - National Land Transport Agency (ANTT)

- 3.5.4.2 Mexico - General Bureau of Standards

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE - National Association of Freight and Logistics (NAFL)

- 3.5.5.2 Saudi Arabia - The Ministry of Transport and Logistics Services

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent landscape (Driven by Primary Research)

- 3.9 Investment & funding analysis

- 3.10 Cost breakdown analysis

- 3.10.1 Research & development costs

- 3.10.2 Manufacturing & hardware production costs

- 3.10.3 Software development & licensing costs

- 3.10.4 Deployment, installation & customer integration costs

- 3.11 Intermodal Logistics Integration

- 3.11.1 Multi-modal transportation automation

- 3.11.2 Port & terminal automation integration

- 3.11.3 Rail-road-air connectivity & data interoperability

- 3.11.4 Cross-border logistics automation challenges

- 3.12 Cybersecurity & Data Infrastructure

- 3.12.1 Cybersecurity risks in automated logistics networks

- 3.12.2 Cloud infrastructure and secure data integration

- 3.12.3 IoT security challenges in smart logistics operations

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Autonomous Robots

- 5.2.2 Automated Storage & Retrieval Systems (AS/RS)

- 5.2.3 Automated Sorting Systems

- 5.2.4 Conveyor Systems

- 5.2.5 De-palletizing/Palletizing Systems

- 5.2.6 Automatic Identification & Data Collection (AIDC)

- 5.3 Software

- 5.3.1 Warehouse Management System (WMS)

- 5.3.2 Transportation Management System (TMS)

- 5.4 Services

- 5.4.1 Consulting

- 5.4.2 Deployment & Integration

- 5.4.3 Support & Maintenance

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Warehouse & Storage Management

- 6.3 Transportation Management

Chapter 7 Market Estimates and Forecast, By Organization Size, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Large Enterprises

- 7.3 Small & Medium Enterprises (SMEs)

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Manufacturing

- 8.3 Retail & E-Commerce

- 8.4 Food & Beverage

- 8.5 Healthcare & Pharmaceuticals

- 8.6 Automotive

- 8.7 Post & Parcel

- 8.8 Oil & Gas

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Norway

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.4.6 Indonesia

- 9.4.7 Singapore

- 9.4.8 Vietnam

- 9.4.9 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Chile

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Daifuku

- 10.1.2 KION Group

- 10.1.3 Honeywell

- 10.1.4 SSI SCHAEFER Group

- 10.1.5 Toyota Industries

- 10.1.6 Rockwell Automation

- 10.1.7 KNAPP

- 10.1.8 KUKA Global (Midea)

- 10.1.9 ABB

- 10.1.10 Beumer Group

- 10.1.11 Korber

- 10.1.12 TGW Logistics

- 10.2 Regional players

- 10.2.1 FORTNA

- 10.2.2 WITRON

- 10.2.3 Fives Group

- 10.2.4 SAVOYE

- 10.2.5 FANUC

- 10.3 Emerging players

- 10.3.1 Locus Robotics

- 10.3.2 GreyOrange

- 10.3.3 Symbotic