|

시장보고서

상품코드

2038704

우유 대체품 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Milk Alternatives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

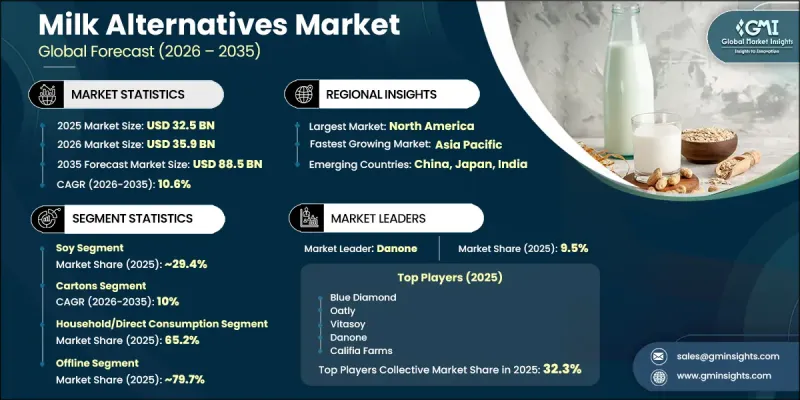

세계의 우유 대체품 시장은 2025년에 325억 달러로 평가되었고, CAGR 10.6%로 성장할 전망이며, 2035년까지 885억 달러에 이를 것으로 추정되고 있습니다.

이 시장은 식물성 영양에 대한 식습관 변화와 유당불내증 및 유제품 과민증에 대한 소비자의 인식이 높아짐에 따라 강력하고 지속적인 성장세를 보이고 있습니다. 비건, 플렉시테리언과 같은 라이프스타일의 확산으로 세계 시장 전체에서 유제품을 사용하지 않는 음료에 대한 수요가 더욱 증가하고 있습니다. 또한, 기존 유제품 생산에 따른 환경 문제에 대한 우려도 지속가능한 식생활로의 전환을 부추기고 있습니다. 시장은 지속적인 제품 혁신, 맛의 개선, 기존 유제품과 매우 유사한 영양 성분의 배합으로 인해 지속적으로 혜택을 누리고 있습니다. 소매 시장 침투 확대와 외식 산업에서의 채택 확대는 이 카테고리의 성장을 더욱 촉진하고 우유 대체 식품을 주류 식품 선택으로 자리 잡게 하는 데 기여하고 있습니다. 업계 전반의 전망은 소비자의 기대치 변화와 제품 다양화에 힘입어 보다 건강하고 지속가능하며 윤리적인 소비 습관으로 꾸준히 전환하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 325억 달러 |

| 예측 시장 규모 | 885억 달러 |

| CAGR | 10.6% |

우유 대체품 카테고리에는 일상적인 소비에서 기존 유제품을 대체할 수 있도록 설계된 다양한 식물성 음료가 포함됩니다. 이 제품들은 유당불내증, 유제품 알레르기가 있거나 비건, 채식주의자, 채식주의자 등 다양한 사람들에게 널리 사용되고 있습니다. 또한, 저칼로리, 저포화지방산 식품을 찾는 건강 지향적인 소비자들에게도 인기가 높습니다. 각 제조업체들은 우유와 영양적 동등성을 높이기 위해 칼슘, 비타민D, 비타민B12 등 필수 영양소를 첨가하는 경향이 강해지고 있습니다. 직접 음용뿐만 아니라 요리, 제과, 음료의 제조에도 널리 이용되고 있으며, 그 사용 범위는 더욱 확대되고 있습니다. 카페, 레스토랑, 가정 내 주방에서의 채택이 진행되면서 시장 침투와 장기적인 수요를 더욱 촉진하고 있습니다.

대두 부문은 2025년 29.4%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 10%로 성장할 것으로 전망됩니다. 콩을 원료로 한 우유는 높은 단백질 함량과 가성비를 바탕으로 가장 확고한 식물성 대체품 중 하나로 자리 잡고 있습니다. 오랜 시장에서의 존재감과 일관된 영양 프로파일은 소비자의 강한 신뢰를 유지하는 데 도움이 되었습니다. 두유는 광범위하게 이용 가능하고 다재다능한 선택지이며, 신규 및 기존 식물성 음료 소비자 모두에게 선호되는 선택지가 되고 있습니다.

종이팩 부문은 2025년 58.8%의 점유율을 차지했으며, 2026-2035년 연평균 복합 성장률(CAGR) 10%를 나타낼 것으로 예측됩니다. 지속가능성과 편의성이 점점 더 중요시되는 가운데, 포장의 혁신은 대체 유제품 산업에서 매우 중요한 역할을 하고 있습니다. 종이팩 포장은 가벼운 구조, 보관의 용이성, 그리고 친환경 소비 트렌드와의 높은 친화력으로 인해 여전히 주류의 지위를 유지하고 있습니다. 재활용 가능성과 환경 부하 감소는 지속가능성을 중시하는 제조업체와 소비자에게 선호되는 선택이 되고 있습니다. 포장 디자인의 지속적인 발전으로 상품 진열의 매력과 기능성이 더욱 향상되고 있습니다.

북미의 우유 대체품 시장은 2025년 34.1%의 점유율을 차지했습니다. 이 지역에서는 웰니스 및 지속 가능한 라이프스타일에 대한 인식이 높아지면서 건강 지향적, 유기농, 식물성 제품에 대한 소비자의 선호가 두드러지고 있습니다. 자동화 및 스마트 패키징 솔루션을 포함한 생산 공정의 기술 발전으로 효율성이 향상되고 환경에 미치는 영향이 감소하고 있습니다. 또한, 이 지역에서는 지속 가능한 조달 관행과 친환경 패키징에 대한 투자도 증가하고 있습니다. 이러한 추세는 탄탄한 소매 인프라와 변화하는 식품 선호도와 함께 북미 전역 시장 성장을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 원료별(2022-2035년)

제6장 시장 추산 및 예측 : 포장 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 유통 채널별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.11The Global Milk Alternatives Market was valued at USD 32.5 billion in 2025 and is estimated to grow at a CAGR of 10.6% to reach USD 88.5 billion by 2035.

The market has been witnessing strong and sustained growth, driven by shifting dietary preferences toward plant-based nutrition and increasing consumer awareness regarding lactose intolerance and dairy sensitivities. Rising adoption of vegan and flexitarian lifestyles has further strengthened demand for dairy-free beverage options across global markets. Environmental concerns related to traditional dairy production have also contributed to the shift toward sustainable food consumption patterns. The market continues to benefit from continuous product innovation, improved taste profiles, and enhanced nutritional formulations that closely replicate conventional dairy. Expanding retail penetration and foodservice adoption have further supported category growth, making milk alternatives a mainstream dietary choice. The overall industry outlook reflects a steady transition toward healthier, sustainable, and ethically driven consumption habits supported by evolving consumer expectations and product diversification.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $32.5 Billion |

| Forecast Value | $88.5 Billion |

| CAGR | 10.6% |

The milk alternatives category includes a wide range of plant-based beverages designed to replace traditional dairy products in everyday consumption. These products are widely used by individuals who are lactose intolerant, allergic to dairy, or following vegan and vegetarian diets. They also appeal to health-conscious consumers seeking lower-calorie and reduced saturated fat options. Manufacturers increasingly fortify these beverages with essential nutrients, including calcium, vitamin D, and vitamin B12, to improve their nutritional equivalence to cow's milk. Beyond direct consumption, these products are extensively used in cooking, baking, and beverage preparation, further expanding their application scope. Their growing adoption across cafes, restaurants, and household kitchens continues to reinforce market penetration and long-term demand.

The soy segment accounted for 29.4% share in 2025 and is projected to grow at a CAGR of 10% through 2035. Soy-based milk remains one of the most established plant-based alternatives, supported by its high protein content and cost-effectiveness. Its long-standing presence in the market and consistent nutritional profile have helped maintain strong consumer trust. Soy milk continues to serve as a widely accessible and versatile option, making it a preferred choice among both new and existing consumers of plant-based beverages.

The cartons segment held a 58.8% share in 2025 and is expected to grow at a CAGR of 10% during 2026 to 2035. Packaging innovation plays a crucial role in the milk alternatives industry, with increasing emphasis on sustainability and convenience. Carton packaging remains dominant due to its lightweight structure, ease of storage, and strong alignment with environmentally responsible consumption trends. Its recyclability and reduced environmental footprint make it a preferred choice among manufacturers and consumers focused on sustainability. Continued advancements in packaging design are further enhancing product shelf appeal and functionality.

North America Milk Alternatives Industry accounted for a 34.1% share in 2025. The region demonstrates high consumer preference for health-focused, organic, and plant-based products, supported by increasing awareness of wellness and sustainable living practices. Technological advancements in production processes, including automation and smart packaging solutions, are improving efficiency and reducing environmental impact. The region is also witnessing growing investment in sustainable sourcing practices and eco-friendly packaging initiatives. These developments, combined with strong retail infrastructure and evolving dietary preferences, continue to strengthen market growth across North America.

Key players operating in the Global Milk Alternatives Market include Oatly, Danone, Califia Farms, Blue Diamond, Ripple Foods, Vitasoy, Elmhurst 1925, Good Karma Foods, Minor Figures, Miyoko's Creamery, nutpods, milkadamia, Kikkoman, and DREAM Plant Based. Companies in the Milk Alternatives Market are focusing on product innovation, portfolio expansion, and sustainability-driven strategies to strengthen their competitive position. Manufacturers are investing heavily in research and development to enhance taste, texture, and nutritional profiles, making plant-based beverages more comparable to traditional dairy. Expansion of product lines across multiple plant sources is helping companies cater to diverse consumer preferences. Strategic partnerships with retail chains and foodservice providers are improving product accessibility and market penetration. Brands are also prioritizing sustainable sourcing and eco-friendly packaging solutions to align with environmental expectations. Digital marketing and influencer collaborations are being used to strengthen brand visibility and consumer engagement. Additionally, companies are focusing on regional expansion and pricing strategies to capture emerging demand across both developed and developing markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Packaging type

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Soy

- 5.3 Almond

- 5.4 Coconut

- 5.5 Oats

- 5.6 Rice

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cartons

- 6.3 Glass bottles

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage processing

- 7.2.1 Ice cream & frozen desserts

- 7.2.2 Bakery & confectionery

- 7.2.3 Nutritional beverages & protein shakes

- 7.2.4 Others

- 7.3 Food service/HoReCa

- 7.3.1 Cafes & coffee shops

- 7.3.2 Restaurants

- 7.3.3 Hotels & catering

- 7.4 Household/direct consumption

- 7.4.1 Drinking

- 7.4.2 Cooking & baking

- 7.4.3 Cereal & breakfast applications

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce

- 8.2.2 Brand websites

- 8.3 Offline

- 8.3.1 Supermarkets/hypermarkets

- 8.3.2 Specialty stores

- 8.3.3 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Blue Diamond

- 10.2 Califia Farms

- 10.3 Danone

- 10.4 DREAM Plant Based

- 10.5 Elmhurst 1925

- 10.6 Good Karma Foods

- 10.7 Kikkoman

- 10.8 milkadamia

- 10.9 Minor Figures

- 10.10 Miyoko's Creamery

- 10.11 nutpods

- 10.12 Oatly

- 10.13 Ripple Foods

- 10.14 Vitasoy