|

시장보고서

상품코드

2038725

우주 물류 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Space Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

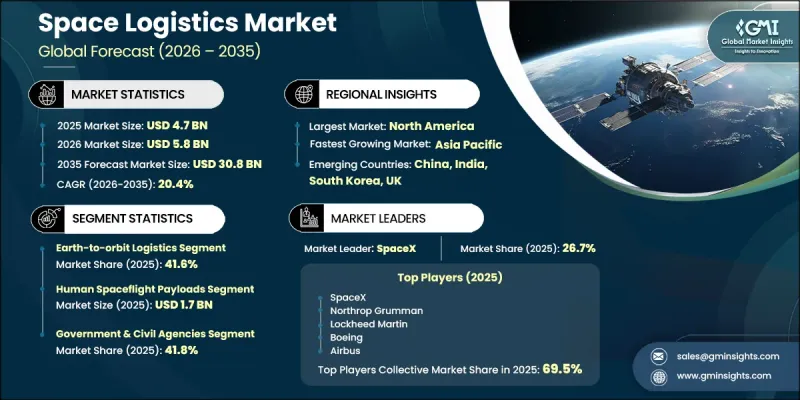

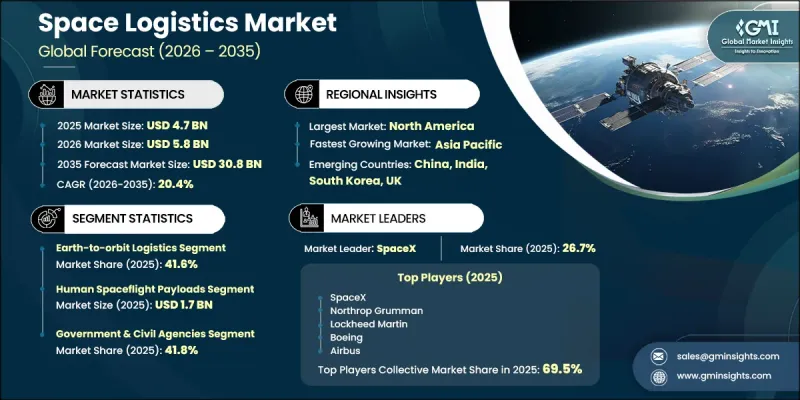

세계의 우주 물류 시장은 2025년에 47억 달러로 평가되었고, 20.4%의 연평균 복합 성장률(CAGR)로 확대될 전망이며, 2035년까지 308억 달러에 이를 것으로 예측됩니다.

이 시장은 대규모 위성 별자리 배치와 궤도 상에서의 운영을 효율적으로 조정해야 할 필요성이 증가함에 따라 성장하고 있습니다. 우주 활동이 더욱 복잡해짐에 따라 위성의 배치, 유지보수, 수명주기 관리를 지원하는 통합 물류 솔루션에 대한 수요가 증가하고 있습니다. 궤도상의 지속가능성과 우주쓰레기 감소에 대한 관심이 높아지면서 체계적인 우주 물류 프레임워크의 필요성이 더욱 가속화되고 있습니다. 또한, 정부 주도의 심우주 탐사 이니셔티브가 확대됨에 따라 지구 궤도를 넘어선 고급 공급망 기능에 대한 수요가 발생하고 있습니다. 궤도 유지보수, 연료 보급, 위성 수명 연장 기술 채택 확대도 시장 확대를 견인하고 있습니다. 우주선 설계, 추진 시스템 및 임무 계획의 지속적인 발전으로 보다 효율적이고 비용 효율적인 우주 운영이 가능해졌습니다. 민간 및 정부 이해관계자들이 우주 인프라에 대한 투자를 확대하는 가운데, 장기적인 우주 임무와 운영 효율성을 지원하기 위해 확장성, 신뢰성, 기술적으로 진보된 물류 시스템의 필요성이 더욱 중요해지고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 47억 달러 |

| 예측 시장 규모 | 308억 달러 |

| CAGR | 20.4% |

우주 물류 시장은 위성 컨스텔레이션의 전개가 가속화됨에 따라 더욱 견인되고 있습니다. 이를 위해서는 발사 일정 조정, 궤도상 위치 결정 및 임무 관리 능력이 요구됩니다. 보다 빈번하고 체계적인 우주 임무로의 전환에 따라 여러 임무에 걸쳐 지속적인 운영을 지원할 수 있는 첨단 물류 시스템에 대한 요구가 증가하고 있습니다. 이러한 변화하는 환경은 효율적인 페이로드 배치, 최적화된 궤도 교통 관리, 향상된 임무 조정을 가능하게 하는 확장 가능한 솔루션에 대한 수요를 견인하고 있습니다. 우주 임무가 점점 더 빈번하고 복잡해짐에 따라 물류 제공업체는 운영 효율을 보장하고 임무 위험을 줄이는 데 있어 매우 중요한 역할을 하고 있습니다.

지구-궤도 물류 분야는 2025년 41.6%의 점유율을 차지했으며, 발사 운영 및 탑재체 운송을 지원하는 데 있어 필수적인 역할을 담당할 것으로 보입니다. 이 분야는 우주 물류 가치사슬의 근간을 이루며, 장비와 위성을 지구에서 지정된 궤도로 운송하는 것을 가능하게 합니다. 위성 네트워크의 확대와 우주 기반 서비스에 대한 수요 증가에 따른 발사 횟수 증가가 이 부문의 강력한 성장을 뒷받침하고 있습니다. 재사용 가능한 발사 시스템의 도입과 발사 기술의 발전은 효율성을 더욱 높이고 비용을 절감하여 지구에서 궤도까지의 물류의 중요성을 더욱 강조하고 있습니다.

소모품 및 추진제 부문은 궤도상 급유 및 임무 기간 연장에 대한 수요 증가로 인해 2026-2035년 연평균 23.5%의 성장률을 보일 것으로 예측됩니다. 우주 임무가 장기화되고 복잡해짐에 따라 효율적인 연료 관리 및 저장 솔루션에 대한 요구가 증가하고 있습니다. 고도화된 추진 시스템과 연료 보급 기술로 인해 우주선의 장기 운용이 가능해져 잦은 발사의 필요성이 줄어들고 있습니다. 연료 저장, 이송 시스템 및 모듈식 공급 솔루션의 혁신은 지속 가능하고 유연한 우주 운영 개발을 더욱 촉진하고 있습니다.

북미의 우주 물류 시장은 우주 탐사에 대한 강력한 투자와 첨단 기술력에 힘입어 2025년 54.8%의 점유율을 차지했습니다. 이 지역은 정부 및 민간 조직이 차세대 우주 물류 솔루션 개발에 적극적으로 기여하고 있는 우주 생태계의 혜택을 누리고 있습니다. 위성 배치, 궤도 서비스, 심우주 임무 지원에 대한 수요 증가가 시장 성장을 주도하고 있습니다. 발사 시스템의 지속적인 발전과 우주 프로그램에 대한 강력한 자금 지원은 이 지역 세계 시장에서의 선도적 지위를 더욱 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 서비스 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 페이로드 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 궤도별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.11The Global Space Logistics Market was valued at USD 4.7 billion in 2025 and is estimated to grow at a CAGR of 20.4% to reach USD 30.8 billion by 2035.

The market is experiencing growth driven by the large-scale deployment of satellite constellations and the increasing need for efficient coordination of orbital operations. As space activities become more complex, demand is rising for integrated logistics solutions that support satellite deployment, servicing, and lifecycle management. Growing focus on orbital sustainability and debris mitigation is further accelerating the need for structured space logistics frameworks. Additionally, expanding government-led deep space exploration initiatives are creating demand for advanced supply chain capabilities beyond Earth's orbit. The increasing adoption of in-orbit servicing, refueling, and satellite life-extension technologies is also strengthening market expansion. Continuous advancements in spacecraft design, propulsion systems, and mission planning are enabling more efficient and cost-effective space operations. As both commercial and government stakeholders increase investments in space infrastructure, the need for scalable, reliable, and technologically advanced logistics systems is becoming critical to support long-term space missions and operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.7 Billion |

| Forecast Value | $30.8 Billion |

| CAGR | 20.4% |

The space logistics market is further driven by the accelerating pace of satellite constellation deployment, which requires coordinated launch scheduling, orbital positioning, and mission management capabilities. The shift toward more frequent and structured space missions is increasing the need for advanced logistics systems that can support continuous operations across multiple missions. This evolving landscape is driving demand for scalable solutions that enable efficient payload deployment, optimized orbital traffic management, and improved mission coordination. As space missions become more frequent and complex, logistics providers are playing a crucial role in ensuring operational efficiency and reducing mission risks.

The earth-to-orbit logistics segment accounted for 41.6% share in 2025, reflecting its essential role in supporting launch operations and payload delivery. This segment forms the backbone of the space logistics value chain, enabling the transportation of equipment and satellites from Earth to designated orbits. Increasing launch frequency, driven by the expansion of satellite networks and growing demand for space-based services, is supporting strong growth in this segment. The adoption of reusable launch systems and advancements in launch technologies are further enhancing efficiency and reducing costs, reinforcing the importance of earth-to-orbit logistics.

The consumables and propellants segment is expected to grow at a CAGR of 23.5% during 2026-2035, driven by rising demand for in-orbit refueling and extended mission capabilities. As space missions become longer and more complex, the need for efficient fuel management and storage solutions is increasing. Advanced propulsion systems and refueling technologies are enabling spacecraft to operate for extended durations, reducing the need for frequent launches. Innovations in fuel storage, transfer systems, and modular delivery solutions are further supporting the development of sustainable and flexible space operations.

North America Space Logistics Market accounted for 54.8% share in 2025, supported by strong investment in space exploration and advanced technological capabilities. The region benefits from a well-established space ecosystem, with both government and private organizations actively contributing to the development of next-generation space logistics solutions. Increasing demand for satellite deployment, in-orbit servicing, and deep-space mission support is driving market growth. Continuous advancements in launch systems, coupled with strong funding for space programs, are further strengthening the region's leadership position in the global market.

Key companies operating in the Space Logistics Market include SpaceX, Boeing, Lockheed Martin, Northrop Grumman, Airbus, Mitsubishi Heavy Industries, Rocket Lab, Relativity Space, Sierra Space, Astroscale, D-Orbit, Momentus, Atomos Space, Impulse Space, and Orbit Fab. Companies in the space logistics market are focusing on strategic initiatives to strengthen their competitive position and expand their global footprint. A major emphasis is placed on developing advanced in-orbit servicing capabilities, including refueling, maintenance, and satellite life-extension solutions. Firms are investing heavily in research and development to improve propulsion systems, autonomous operations, and mission planning technologies. Strategic partnerships with government agencies, satellite operators, and launch service providers are helping companies secure long-term contracts and expand service offerings. Businesses are also prioritizing reusable spacecraft technologies and modular logistics platforms to enhance cost efficiency and scalability. Geographic expansion and increased investment in launch infrastructure are further supporting growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Service type trends

- 2.2.2 Payload type trends

- 2.2.3 Orbit trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid satellite constellation deployments driving logistics demand

- 3.2.1.2 Space debris mitigation requirements increasing orbital servicing demand

- 3.2.1.3 Government lunar exploration missions requiring supply chain support

- 3.2.1.4 Commercial in-orbit servicing and refueling market expansion

- 3.2.1.5 Reusable launch systems increasing frequency of orbital logistics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of in-orbit servicing infrastructure deployment

- 3.2.2.2 Limited on-orbit refueling technology standardization globally

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging lunar logistics and deep-space supply chains

- 3.2.3.2 Satellite life-extension and servicing subscription models expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Service Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Earth-to-orbit logistics

- 5.3 Orbital transportation services

- 5.4 On-orbit servicing & assembly (OSAM/ISAM)

- 5.5 End-of-life & sustainability services

- 5.6 Mission & logistics operations support

Chapter 6 Market Estimates and Forecast, By Payload Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Space systems

- 6.3 Human spaceflight payloads

- 6.4 Consumables & propellants

- 6.5 Infrastructure payloads

Chapter 7 Market Estimates and Forecast, By Orbit, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Low earth orbit (LEO)

- 7.3 Medium earth orbit (MEO)

- 7.4 Geostationary orbit (GEO/GSO)

- 7.5 Beyond GEO

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Commercial operators

- 8.3 Government & civil agencies

- 8.4 Defense & intelligence

- 8.5 Space infrastructure developers

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 SpaceX

- 10.1.2 Northrop Grumman

- 10.1.3 Lockheed Martin

- 10.1.4 Boeing

- 10.1.5 Airbus

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Rocket Lab

- 10.2.1.2 Sierra Space

- 10.2.1.3 Momentus

- 10.2.1.4 Impulse Space

- 10.2.2 Asia Pacific

- 10.2.2.1 Mitsubishi Heavy Industries

- 10.2.3 Europe

- 10.2.3.1 D-Orbit

- 10.2.3.2 Astroscale

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Orbit Fab

- 10.3.2 Relativity Space

- 10.3.3 Atomos Space