|

시장보고서

상품코드

2038735

콜드 가스 스프레이 코팅 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Cold Gas Spray Coating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

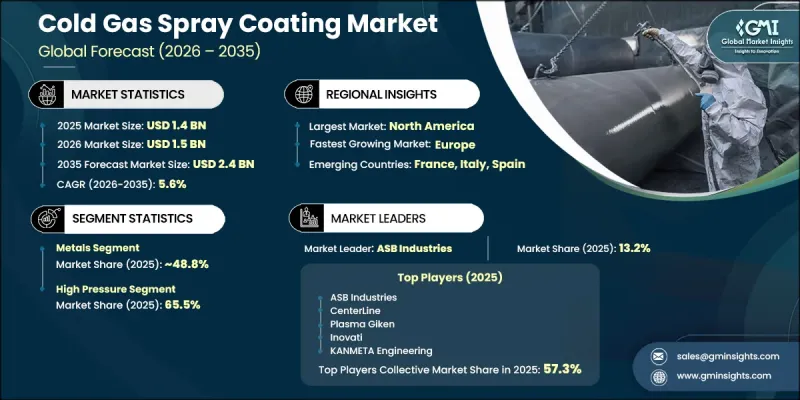

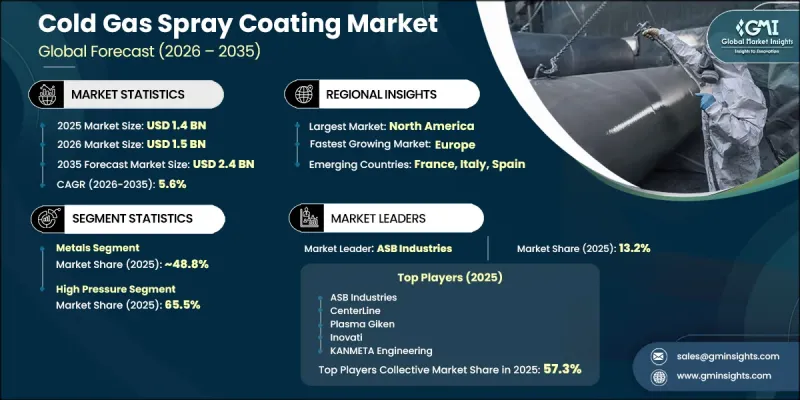

세계의 콜드 가스 스프레이 코팅 시장은 2025년에 14억 달러로 평가되었고 CAGR 5.6%로 성장하여 2035년까지 24억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 여러 산업 분야에서 고급 표면 보호 솔루션에 대한 수요가 증가함에 따라 주도되고 있습니다. 이러한 산업에서는 모재의 기계적 특성을 유지하면서 내구성을 높이는 코팅이 요구되고 있습니다. 콜드 가스 스프레이 기술은 상대적으로 낮은 온도에서 코팅을 증착하는 뚜렷한 장점이 있으며, 고밀도 및 내구성있는 보호 층을 형성하면서 기판의 무결성을 유지하는 데 도움이 됩니다. 이 공정은 기존 코팅 방식에 비해 열 응력을 최소화하기 때문에 높은 성능이 요구되는 응용 분야에서 더 높은 정밀도와 효율을 실현합니다. 재료의 수명 연장 및 유지 보수 요구 사항 감소에 대한 관심이 높아지면서 이 기술의 채택이 더욱 가속화되고 있습니다. 코팅 기술과 재료 과학의 끊임없는 발전으로 성능이 향상되고 각 산업은 엄격한 운영 요구 사항을 충족시킬 수 있게 되었습니다. 그 결과, 콜드 가스 분무 코팅은 첨단 표면 공학의 요구에 부응하는 신뢰할 수 있고 효율적인 솔루션으로서 강력한 지지를 받고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 14억 달러 |

| 예측 규모 | 24억 달러 |

| CAGR | 5.6% |

2025년에는 금속 부문이 48.8%의 점유율을 차지했습니다. 금속은 강도, 내구성 및 환경 악화에 대한 내성으로 인해 널리 활용되고 있습니다. 콜드 스프레이 공정은 금속 분말을 녹이지 않고 가속하여 코팅하기 때문에 기판의 구조적 특성을 유지한 채 코팅을 할 수 있습니다. 이를 통해 높은 정밀도와 신뢰성이 요구되는 섬세한 부품에 코팅을 적용할 수 있어 이 분야의 선도적 입지를 강화하고 있습니다.

2025년 기준 고압 부문은 65.5%의 점유율을 차지했습니다. 고압 시스템은 입자 속도를 향상시키고, 더 견고한 결합, 코팅 밀도 향상 및 표면 품질 향상을 가져옵니다. 이러한 특성으로 인해 이러한 시스템은 다양한 산업 분야에서 일관된 고성능 결과를 달성하는 데 매우 효과적입니다. 신뢰할 수 있는 결과를 제공하는 능력은 상업적 환경에서 광범위한 채택에 기여하고 있습니다.

2025년 북미 콜드 가스 스프레이 코팅 시장 규모는 4억 2,160만 달러로 평가되었습니다. 이 지역의 성장은 고성능 코팅 기술에 대한 수요 증가와 산업 제조 공정의 지속적인 발전으로 뒷받침되고 있습니다. 엄격한 규제 기준과 장기적인 재료 성능에 대한 요구는 첨단 코팅 솔루션의 채택을 촉진하고 있습니다. 혁신과 인프라에 대한 지속적인 투자는 이 지역 시장 전망을 더욱 견고하게 만들고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 재료별, 2022-2035년

제6장 시장 추산 및 예측 : 기술별, 2022-2035년

제7장 시장 추산 및 예측 : 용도별, 2022-2035년

제8장 시장 추산 및 예측 : 최종 이용 산업별, 2022-2035년

제9장 시장 추산 및 예측 : 지역별, 2022-2035년

제10장 기업 개요

JHS 26.05.29The Global Cold Gas Spray Coating Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 2.4 billion by 2035.

Market growth is driven by rising demand for advanced surface protection solutions across multiple industrial sectors. These industries require coatings that enhance durability while preserving the mechanical properties of base materials. Cold gas spray technology offers a distinct advantage by depositing coatings at relatively low temperatures, which helps maintain substrate integrity while forming dense and durable protective layers. This process minimizes thermal stress compared to conventional coating methods, allowing for greater precision and efficiency in applications that demand high performance. Increasing focus on improving material longevity and reducing maintenance requirements is further accelerating adoption. Continuous advancements in coating techniques and material science are enhancing performance capabilities, enabling industries to meet stringent operational requirements. As a result, cold gas spray coating is gaining strong traction as a reliable and efficient solution for advanced surface engineering needs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 5.6% |

The metals segment accounted for 48.8% share in 2025. Metals are widely utilized due to their strength, durability, and resistance to environmental degradation. The cold spray process accelerates metal powders without melting them, enabling coating application while preserving the structural properties of the substrate. This approach supports the use of coatings on sensitive components that require high precision and reliability, reinforcing the segment's leading position.

The high-pressure segment held a share of 65.5% in 2025. High-pressure systems enable faster particle velocities, resulting in stronger bonding, improved coating density, and enhanced surface quality. These characteristics make such systems highly effective for achieving consistent and high-performance results across a range of industrial applications. Their ability to deliver reliable outcomes has contributed to widespread adoption in commercial environments.

North America Cold Gas Spray Coating Market was valued at USD 421.6 million in 2025 Growth in the region is supported by increasing demand for high-performance coating technologies and ongoing advancements in industrial manufacturing processes. Strict regulatory standards and the need for long-lasting material performance are encouraging the adoption of advanced coating solutions. Continued investment in innovation and infrastructure is further strengthening the regional market outlook.

Key companies operating in the Global Cold Gas Spray Coating Market include ASB Industries, CenterLine, Inovati, Plasma Giken, Hannecard, Cadorath, KANMETA Engineering, ECK Pte Ltd, A&A Coatings, Dycomet, UCT Coatings, and Evology Manufacturing. Companies in the cold gas spray coating market are focusing on strengthening their competitive position through innovation, strategic partnerships, and process optimization. Industry participants are investing in advanced equipment and material technologies to improve coating performance, efficiency, and application precision. Collaborations with industrial clients help companies develop tailored solutions that meet specific operational requirements. Many firms are also expanding their global footprint and enhancing distribution networks to reach a wider customer base. In addition, continuous research and development efforts are enabling the introduction of improved coating techniques that align with evolving industry standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased demand for anti-corrosion coating in marine & energy sector

- 3.2.1.2 Expanding applications in aerospace & defense for lightweight component

- 3.2.1.3 Growing adoption in automotive sector for performance enhancement

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High equipment & operational costs

- 3.2.2.2 Technical challenge with ceramic & polymer deposition

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for surface protection in aerospace and automotive industries

- 3.2.3.2 Increasing adoption in biomedical and electronics manufacturing for precision coatings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By material

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Metals

- 5.2.1 Aluminum

- 5.2.2 Copper

- 5.2.3 Nickel

- 5.2.4 Titanium

- 5.2.5 Zinc

- 5.2.6 Stainless steel

- 5.2.7 Nickel-base alloys (Inconel, Hastelloy)

- 5.2.8 Others (tantalum, silver, magnesium)

- 5.3 Ceramics

- 5.3.1 Aluminum oxide (alumina)

- 5.3.2 Silicon carbide

- 5.3.3 Others

- 5.4 Composites

- 5.4.1 Metal-metal (copper-tungsten, copper-chromium)

- 5.4.2 Metal-carbide (aluminum-silicon carbide)

- 5.4.3 Metal-oxide (aluminum-alumina)

- 5.4.4 Others

- 5.5 Polymers

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 High Pressure

- 6.3 Low Pressure

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Corrosion protection

- 7.2.1 Marine & offshore applications

- 7.2.2 Oil & gas infrastructure

- 7.2.3 Automotive underbody protection

- 7.3 Wear resistance

- 7.3.1 High-wear industrial components

- 7.3.2 Machinery & tooling

- 7.4 Thermal barrier coatings

- 7.4.1 Gas turbine components

- 7.4.2 Engine parts

- 7.4.3 Bond coats for ceramic top coats

- 7.5 Dimensional restoration

- 7.5.1 Component repair & refurbishment

- 7.5.2 Mating surface restoration

- 7.5.3 Ultra-thick deposit applications

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.2.1 Commercial aircraft

- 8.2.2 Military aircraft

- 8.2.3 Spacecraft & satellites

- 8.2.4 Ground support equipment

- 8.3 Automotive

- 8.3.1 Passenger vehicles

- 8.3.2 Commercial vehicles

- 8.3.3 Electric vehicles

- 8.4 Industrial equipment

- 8.4.1 Heavy machinery

- 8.4.2 Manufacturing equipment

- 8.4.3 Mining equipment

- 8.5 Electronics

- 8.5.1 Electronic components

- 8.5.2 Semiconductor manufacturing equipment

- 8.5.3 Printed circuit boards

- 8.6 Energy

- 8.7 Medical

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 ASB Industries

- 10.2 CenterLine

- 10.3 Inovati

- 10.4 Plasma Giken

- 10.5 Hannecard

- 10.6 Cadorath

- 10.7 KANMETA Engineering

- 10.8 ECK Pte Ltd

- 10.9 A&A Coatings

- 10.10 Dycomet

- 10.11 UCT Coatings

- 10.12 Evology Manufacturing