|

시장보고서

상품코드

2038786

선외기 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Outboard Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

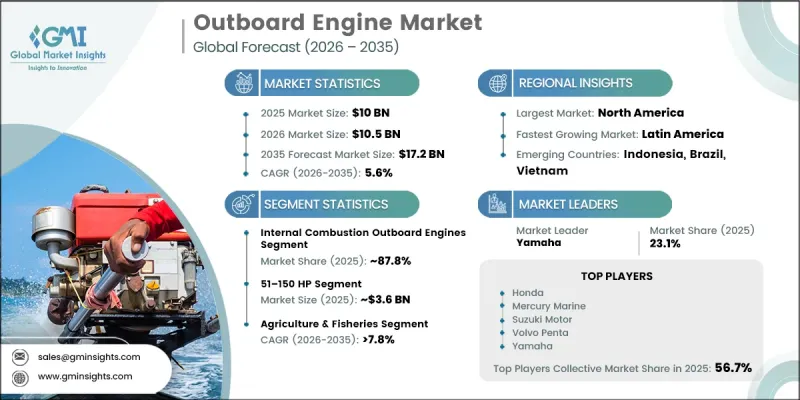

세계의 선외기 시장은 2025년에 100억 달러로 평가되었고, CAGR 5.6%로 성장할 전망이며, 2035년까지 172억 달러에 이를 것으로 추정되고 있습니다.

시장의 성장은 특히 레크리에이션용 보트 및 낚시 활동이 계속 확대되고 있는 해안 지역을 중심으로 해양 관광의 인기가 높아지고 있는 것에 힘입은 바 있습니다. 또한, 각 지역 정부도 해양관광 인프라 구축에 투자하고 있어 선외기(선외기 모터라고도 함)에 대한 수요가 더욱 증가하고 있습니다. 또한, 상업적 어업과 정부 해상 업무의 안정적인 수요가 시장의 장기적인 안정성을 뒷받침하고 있습니다. 소형 선박은 기동성과 비용 효율성으로 인해 널리 사용되고 있으며, 이는 어업 분야에서 선외기의 채택을 계속 촉진하고 있습니다. 해양 당국과 해안 경비대도 고속 성능, 얕은 수심에서의 운용 적합성, 유지 보수 및 교체 용이성 때문에 이 엔진에 의존하고 있습니다. 동시에 이 시장의 제품 개발은 엄격한 배출가스 규제와 연비 기준의 영향을 점점 더 강하게 받고 있습니다. 주요 국가의 환경 당국이 제정한 규제 프레임워크는 첨단 연료 분사 시스템과 4행정 엔진 기술로의 전환을 가속화하여 구식 2행정 구성을 대체하고 산업 전반의 현대화를 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 100억 달러 |

| 예측 시장 규모 | 172억 달러 |

| CAGR | 5.6% |

2025년에는 내연기관 부문이 시장 점유율의 87.8%를 차지했으며, 88억 달러 시장 규모를 창출했습니다. 이 부문은 강력한 출력, 운영상의 신뢰성, 그리고 광범위한 선박용 연료 공급 인프라가 구축되어 있어 여전히 지배적인 위치를 유지하고 있습니다. 특히 4행정 내연기관 시스템은 레크리에이션, 상업용, 정부 관련 선박 운용에서 안정적인 마력을 발휘할 수 있다는 점에서 선호되고 있습니다. 해상 운항 및 장거리 항해에서 우수한 성능으로 인해 신흥 전기 대체 기술과 비교하여 지속적으로 널리 채택되고 있습니다.

51-150마력 부문은 2025년 36.4%의 점유율을 차지했으며, 시장 규모는 36억 달러에 달했습니다. 이 마력 범위는 연비 효율과 작동 출력의 균형이 잘 잡혀 있어 널리 선호되고 있습니다. 레저용 보트와 소규모 상업용 보트 모두를 효과적으로 지원하며, 다양한 선종에 적합한 추진력을 제공합니다. 중형 레크리에이션용 보트 및 유틸리티 수상 선박에서 다용도로 사용할 수 있어 비용 효율적인 선박용 추진 솔루션을 찾는 개인 사용자 및 소규모 사업자들 사이에서 널리 채택되고 있는 카테고리입니다.

미국 선외기 시장은 2025년 35억 달러에 달했으며, 2026-2035년 연평균 4.4%의 성장률을 보일 것으로 예측됩니다. 이 나라는 뿌리 깊은 보트 문화와 광범위한 내륙 및 해안 수로 네트워크 덕분에 여전히 가장 큰 국내 시장으로 남아 있습니다. 레크리에이션 목적의 보트 이용이 활발하고 등록 보트 수가 많기 때문에 선외기에 대한 수요는 안정적입니다. 또한, 미국 전역의 호수, 강, 해안 지역, 특히 고출력 및 4행정 엔진 카테고리에서 엔진 판매의 지속적인 확대에 크게 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 추진 방식 및 에너지 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 마력별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 점화 방식별(2022-2035년)

제9장 시장 추산 및 예측 : 수로별(2022-2035년)

제10장 시장 추산 및 예측 : 판매 채널별(2022-2035년)

제11장 시장 추산 및 예측 : 지역별(2022-2035년)

제12장 기업 개요

AJY 26.06.11The Global Outboard Engine Market was valued at USD 10 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 17.2 billion by 2035.

Market growth is supported by the rising popularity of marine tourism, particularly across coastal regions, where recreational boating and fishing activities continue to expand. Governments across various regions are also investing in marine-based tourism infrastructure, further strengthening demand for outboard engines, also known as outboard motors. In addition, steady demand from commercial fishing and government maritime operations is sustaining long-term market stability. Small watercraft remain widely used due to their mobility and cost efficiency, which continues to support outboard engine adoption across fishing applications. Maritime authorities and coastal security agencies also rely on these engines due to their high-speed capability, shallow water operation advantage, and ease of maintenance and replacement. At the same time, product development in this market is increasingly influenced by strict emissions regulations and fuel efficiency standards. Regulatory frameworks established by environmental authorities in major economies are accelerating the transition toward advanced fuel injection systems and four-stroke engine technologies, replacing older two-stroke configurations and driving modernization across the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10 Billion |

| Forecast Value | $17.2 Billion |

| CAGR | 5.6% |

The internal combustion engine segment accounted for 87.8% share in 2025, generating USD 8.8 billion. This segment remains dominant due to its strong power output, operational reliability, and established fueling infrastructure that supports a wide range of marine applications. Four-stroke internal combustion systems are particularly preferred for their ability to deliver consistent horsepower across recreational, commercial, and government marine operations. Their strong performance in offshore conditions and long-distance marine travel continues to make them more widely adopted compared to emerging electric alternatives.

The 51-150 HP segment held 36.4% share in 2025, valued at USD 3.6 billion. This horsepower range is widely preferred due to its balanced combination of fuel efficiency and operational power. It effectively supports both recreational boating and small-scale commercial use, offering suitable propulsion for a variety of vessel types. Its versatility across mid-sized recreational boats and utility watercraft makes it a widely adopted category among both individual users and small business operators seeking cost-effective marine propulsion solutions.

U.S. Outboard Engine Market reached USD 3.5 billion in 2025 and is projected to grow at a CAGR of 4.4% from 2026 to 2035. The country continues to represent the largest national market due to its strong boating culture and extensive network of inland and coastal waterways. High levels of recreational boating activity and a large registered boat population support consistent demand for outboard engines. In addition, lakes, rivers, and coastal zones across the country contribute significantly to sustained engine sales, particularly in higher horsepower and four-stroke engine categories.

Key companies operating in the Outboard Engine Market include Yamaha, Honda, Brunswick, Suzuki Motor, Volvo Penta, Yanmar, Torqeedo, Tohatsu, Oxe Marine, and Parsun Power Machine. Companies in the Outboard Engine Market are focusing on developing fuel-efficient and low-emission propulsion systems to comply with tightening environmental regulations. Significant investments in engine electrification and hybrid propulsion technologies are being made to align with future sustainability goals. Manufacturers are also enhancing product durability and corrosion resistance to improve performance in harsh marine environments. Expansion of service networks and aftermarket support is being prioritized to strengthen customer retention and long-term brand loyalty. Strategic collaborations with boat manufacturers are enabling better product integration and increased market penetration. In addition, companies are focusing on lightweight engine designs and advanced fuel injection systems to improve performance efficiency. Digital monitoring solutions and smart engine diagnostics are also being introduced to enhance user experience and predictive maintenance capabilities across marine applications.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Horsepower

- 2.2.4 Application

- 2.2.5 Ignition

- 2.2.6 Waterways

- 2.2.7 Sales channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing recreational boating and water sports activities

- 3.2.1.2 Increasing demand for fuel-efficient and eco-friendly engines

- 3.2.1.3 Expansion of commercial and industrial marine operations

- 3.2.1.4 Technological advancements in outboard engine design and performance

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Stringent marine emission regulations

- 3.2.2.2 Limited range for electric outboards

- 3.2.3 Market opportunities

- 3.2.3.1 Electrification & hybrid integration

- 3.2.3.2 Demand for portable outboards in emerging markets

- 3.2.3.3 Growth in eco-tourism & sustainable boating

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Advanced fuel injection systems

- 3.3.1.2 Corrosion-resistant materials for saltwater use

- 3.3.1.3 Digital engine monitoring & smart controls

- 3.3.2 Emerging technologies

- 3.3.2.1 Electric & hybrid outboard propulsion

- 3.3.2.2 Lightweight composite materials

- 3.3.2.3 Modular & portable power units

- 3.3.2.4 Connected outboards (IoT Integration)

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - EPA engine emission standards

- 3.6.1.2 Canada - Transport Canada Marine Safety

- 3.6.2 Europe

- 3.6.2.1 EU - European Commission - Recreational Craft Directive (RCD)

- 3.6.2.2 Germany - Federal Maritime and Hydrographic Agency (BSH)

- 3.6.3 Asia Pacific

- 3.6.3.1 China - China Classification Society (CCS)

- 3.6.3.2 Australia - Australian Maritime Safety Authority (AMSA)

- 3.6.4 Latin America

- 3.6.4.1 Brazil - Brazilian Navy Directorate of Ports and Coasts (DPC)

- 3.6.4.2 Mexico - Secretariat of Environment and Natural Resources (SEMARNAT)

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE - UAE Ministry of Energy and Infrastructure

- 3.6.5.2 Saudi Arabia - Saudi Ports Authority

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Trade Data Analysis (Driven by Paid Database)

- 3.10.1 Import/Export Volume & Value Trends

- 3.10.2 Key Trade Corridors & Tariff Impact

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Installed Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

- 3.12 Cost breakdown analysis

- 3.13 Impact of AI & Generative AI on the Market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Propulsion/Energy Type, 2022- 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Internal combustion

- 5.2.1 2-stroke

- 5.2.2 4-stroke

- 5.3 Electric propulsion

- 5.4 Natural gas (LPG/CNG)

Chapter 6 Market Estimates & Forecast, By Horsepower, 2022- 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Up to 50 HP

- 6.3 51-150 HP

- 6.4 Above 150 HP

Chapter 7 Market Estimates & Forecast, By Application, 2022- 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Government

- 7.2.1 Military

- 7.2.2 Coast guard

- 7.2.3 Patrol

- 7.2.4 Rescue

- 7.2.5 Public service vessels

- 7.2.6 Emergency & disaster relief vessels

- 7.3 Recreational & personal use

- 7.3.1 Water sports (skiing, wakeboarding, sport boating)

- 7.3.2 Recreational fishing

- 7.3.3 Fitness & outdoor activity boating

- 7.3.4 Tourism & rental fleets

- 7.3.4.1 Leisure & sport tourism

- 7.3.5 Private pleasure craft (yachting/tender use)

- 7.4 Industrial

- 7.4.1 Goods transport

- 7.4.2 Passenger transport

- 7.4.3 Offshore operations & support vessels

- 7.4.4 Workboats

- 7.5 Agriculture & fisheries

- 7.5.1 Inland fishery boats

- 7.5.2 Aquaculture support vessels

- 7.5.3 Irrigation & rural utility boats

Chapter 8 Market Estimates & Forecast, By Ignition, 2022- 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Electric

- 8.3 Manual

Chapter 9 Market Estimates & Forecast, By Waterways, 2022- 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Seagoing

- 9.2.1 Government

- 9.2.1.1 Military

- 9.2.1.2 Coast guard

- 9.2.1.3 Patrol

- 9.2.1.4 Rescue

- 9.2.1.5 Public service vessels

- 9.2.1.6 Emergency & disaster relief vessels

- 9.2.2 Recreational & personal use

- 9.2.2.1 Water sports (skiing, wakeboarding, sport boating)

- 9.2.2.2 Recreational fishing

- 9.2.2.3 Fitness & outdoor activity boating

- 9.2.2.4 Tourism & rental fleets

- 9.2.2.4.1 Leisure & sport tourism

- 9.2.2.5 Private pleasure craft (yachting/tender use)

- 9.2.3 Industrial

- 9.2.3.1 Goods transport

- 9.2.3.2 Passenger transport

- 9.2.3.3 Offshore operations & support vessels

- 9.2.3.4 Workboats

- 9.2.4 Agriculture & fisheries

- 9.2.4.1 Inland fishery boats

- 9.2.4.2 Aquaculture support vessels

- 9.2.4.3 Irrigation & rural utility boats

- 9.2.1 Government

- 9.3 Inland

- 9.3.1 Government

- 9.3.1.1 Military

- 9.3.1.2 Coast guard

- 9.3.1.3 Patrol

- 9.3.1.4 Rescue

- 9.3.1.5 Public service vessels

- 9.3.1.6 Emergency & disaster relief vessels

- 9.3.2 Recreational & personal use

- 9.3.2.1 Water sports (skiing, wakeboarding, sport boating)

- 9.3.2.2 Recreational fishing

- 9.3.2.3 Fitness & outdoor activity boating

- 9.3.2.4 Tourism & rental fleets

- 9.3.2.4.1 Leisure & sport tourism

- 9.3.2.5 Private pleasure craft (yachting/tender use)

- 9.3.3 Industrial

- 9.3.3.1 Goods transport

- 9.3.3.2 Passenger transport

- 9.3.3.3 Offshore operations & support vessels

- 9.3.3.4 Workboats

- 9.3.4 Agriculture & fisheries

- 9.3.4.1 Inland fishery boats

- 9.3.4.2 Aquaculture support vessels

- 9.3.4.3 Irrigation & rural utility boats

- 9.3.1 Government

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022- 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Hungary

- 11.3.9 Greece

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Yamaha Motor

- 12.1.2 Mercury Marine

- 12.1.3 Honda Motor

- 12.1.4 Suzuki Motor

- 12.1.5 Tohatsu

- 12.1.6 Volvo Penta

- 12.1.7 Torqeedo

- 12.1.8 Parsun Power Machine

- 12.1.9 Hidea Power Machinery

- 12.1.10 Selva

- 12.2 Regional players

- 12.2.1 Hangkai

- 12.2.2 Changchai Company

- 12.2.3 Cox Powertrain

- 12.2.4 ePropulsion

- 12.2.5 Aquawatt

- 12.2.6 Briggs & Stratton

- 12.3 Emerging players

- 12.3.1 Caudwell Marine

- 12.3.2 Zhejiang Anqidi Power Machinery

- 12.3.3 Jinhua Himarine Machinery

- 12.3.4 Boatee