|

시장보고서

상품코드

2045698

담도 스텐트 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Biliary Stents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

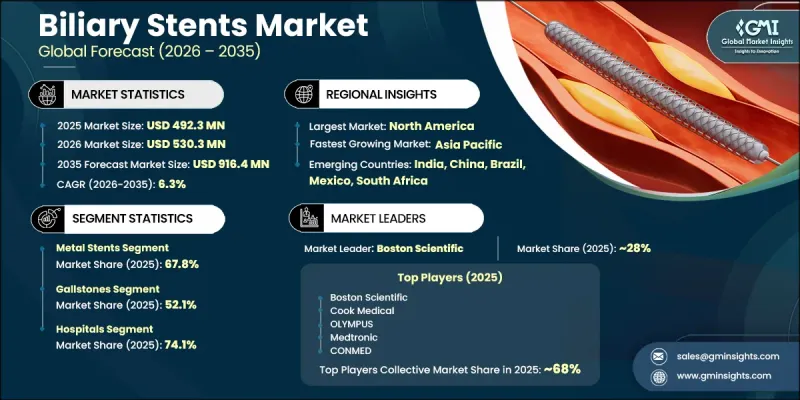

세계의 담관 스텐트 시장은 2025년에 4억 9,230만 달러로 평가되었고, CAGR 6.3%로 성장할 전망이며, 2035년까지 9억 1,640만 달러에 이를 것으로 예측됩니다.

담도 질환의 발생률 증가, 간췌장암 발병률 증가, 저침습적 치료법에 대한 선호도 증가로 인해 시장은 꾸준히 성장하고 있습니다. 담도 스텐트는 담관 폐쇄, 담관 협착, 누출, 간 및 췌장 질환과 관련된 염증성 질환을 앓고 있는 환자의 효과적인 담즙 배출을 돕기 위해 광범위하게 사용되고 있습니다. 첨단 중재시술의 사용 확대와 더불어 스텐트 기술 및 영상진단 시스템의 지속적인 개선이 세계 시장 성장을 견인하고 있습니다. 의료 인프라 확충과 전문 소화기 질환 치료에 대한 접근성 향상도 선진국과 신흥국 모두에서 도입을 더욱 촉진하고 있습니다. 또한, 고령화 및 생활습관 변화에 따른 만성질환 부담 증가로 인해 첨단 담도 관리 솔루션에 대한 수요는 지속적으로 증가하고 있습니다. 스텐트 소재, 유연성, 내구성 및 삽입 기술의 기술적 진보도 치료 결과를 개선하고 장기적인 시장 발전을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 4억 9,230만 달러 |

| 예측 시장 규모 | 9억 1,640만 달러 |

| CAGR | 6.3% |

담관 스텐트 시장은 의료진이 담관 합병증 치료를 위해 최소침습적 수술을 점점 더 많이 채택함에 따라 계속 확대되고 있습니다. ERCP나 PTC와 같은 기술은 회복 기간 단축, 수술 위험 최소화, 환자 예후 개선이 가능하기 때문에 널리 선호되고 있습니다. 췌장암, 간질환, 담도 감염 및 만성 염증성 질환의 유병률 증가로 인해 효과적인 스텐트 삽입술의 필요성이 크게 증가하고 있습니다. 악성 및 양성 질환으로 인한 담도 폐쇄는 종종 장기적인 배액 관리가 필요하며, 이는 제품 수요를 더욱 촉진하고 있습니다. 또한, 유연성 향상, 이동 방지 기능, 생체 적합성 향상 등 스텐트 설계의 개선이 임상 현장에서의 채택 확대에 기여하고 있습니다. 의료비 증가와 고급 소화기내과 서비스의 보급도 이 산업에 유리한 성장 기회를 창출하고 있습니다.

2025년에는 금속 스텐트 부문이 67.8%의 점유율을 차지한 것으로 평가되었습니다. 금속 스텐트는 우수한 방사형 강도, 장기적인 내구성 및 낮은 폐색 위험으로 인해 계속해서 선도적인 위치를 유지하고 있습니다. 자가 확장형 금속 스텐트는 담관 개통 기간을 연장하고 재개입의 필요성을 줄이기 때문에 악성 담도 폐쇄 관리에서 점점 더 선호되고 있습니다. 담관암과 췌장 악성종양 발생률이 증가함에 따라 완화 치료 및 장기적인 질병 관리 분야에서 이러한 첨단 스텐트 솔루션의 채택이 더욱 가속화되고 있습니다.

담석 부문은 2025년에 52.1%의 점유율을 차지한 것으로 평가되었으며, 2026-2035년 4억 7,580만 달러에 달할 것으로 예측됩니다. 담석 관련 합병증 유병률 증가는 전 세계 담도 스텐트 수요에 크게 기여하고 있습니다. 건강에 해로운 식습관, 비만, 좌식 생활습관 등의 요인으로 인해 담석 형성 및 담도 폐쇄의 발생이 증가하고 있습니다. 스텐트 삽입을 통한 내시경 치료는 담즙의 흐름을 회복하고 증상을 완화하며 담도 폐쇄 및 염증성 질환과 관련된 합병증을 최소화하는 데 중요한 역할을 계속하고 있습니다.

북미의 담도 스텐트 시장은 2025년 35% 점유율을 차지한 것으로 평가되었습니다. 이 지역은 담도 질환, 췌장 질환 및 간 담도암의 높은 유병률로 인해 업계 성장에 기여하는 주요 원천이 되고 있습니다. 비만, 대사 장애, 노화에 따른 건강 합병증 증가는 지역 전체에서 첨단 담도 치료 기술에 대한 수요 증가를 뒷받침하고 있습니다. 또한, 북미는 고도로 발달된 의료 시스템, 첨단 인터벤션 기술의 적극적인 도입, 그리고 전문적인 내시경 검사의 광범위한 이용이 가능하다는 이점을 누리고 있습니다. 의료 혁신과 고급 소화기 서비스에 대한 투자 확대는 이 지역 시장 확대를 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 용도별(2022-2035년)

제7장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

AJY 26.06.09The Global Biliary Stents Market was valued at USD 492.3 million in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 916.4 million by 2035.

The market is witnessing steady expansion due to the growing occurrence of biliary tract disorders, rising incidence of hepatopancreatic cancers, and increasing preference for minimally invasive treatment procedures. Biliary stents are widely used to manage bile duct blockages and support effective bile drainage in patients suffering from biliary strictures, leaks, and inflammatory conditions linked to liver and pancreatic diseases. The growing use of advanced interventional procedures, combined with ongoing improvements in stent technology and diagnostic imaging systems, is strengthening market growth worldwide. Expanding healthcare infrastructure and rising access to specialized gastroenterology treatments are further supporting adoption across both developed and emerging economies. In addition, the increasing burden of chronic diseases associated with aging populations and changing lifestyle patterns continues to elevate demand for advanced biliary management solutions. Technological progress in stent materials, flexibility, durability, and placement techniques is also improving treatment outcomes and supporting long-term market development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $492.3 Million |

| Forecast Value | $916.4 Million |

| CAGR | 6.3% |

The biliary stents market continues to expand as healthcare providers increasingly adopt minimally invasive procedures for the treatment of bile duct complications. Techniques such as ERCP and PTC have become widely preferred due to their ability to reduce recovery time, minimize surgical risks, and improve patient outcomes. The growing prevalence of pancreatic cancer, liver disorders, biliary infections, and chronic inflammatory conditions is significantly increasing the need for effective stenting procedures. Biliary obstruction caused by malignant and benign conditions frequently requires long-term drainage management, further strengthening product demand. In addition, improvements in stent design, including enhanced flexibility, anti-migration features, and better biocompatibility, are contributing to greater clinical adoption. Rising healthcare spending and broader availability of advanced gastroenterology services are also creating favorable growth opportunities for the industry.

The metal stents segment accounted for 67.8% share in 2025. The segment continues to maintain a leading position due to the superior radial strength, long-term durability, and lower risk of blockage associated with metal-based stents. Self-expandable metal stents are increasingly preferred for managing malignant biliary obstructions because they provide prolonged duct patency and reduce the need for repeated interventions. The growing incidence of bile duct cancers and pancreatic malignancies is further accelerating the adoption of these advanced stenting solutions in palliative care and long-term disease management.

The gallstones segment held a share of 52.1% in 2025 and is anticipated to reach USD 475.8 million during 2026-2035. The rising prevalence of gallstone-related complications is significantly contributing to the demand for biliary stents globally. Factors, including unhealthy dietary habits, obesity, and sedentary lifestyles, are increasing the occurrence of gallstone formation and associated biliary obstructions. Endoscopic treatment approaches involving stent placement continue to play an essential role in restoring bile flow, relieving symptoms, and minimizing complications linked to biliary blockages and inflammatory conditions.

North America Biliary Stents Market held a 35% share in 2025. The region remains a major contributor to industry growth due to the high prevalence of biliary diseases, pancreatic disorders, and hepatobiliary cancers. Increasing rates of obesity, metabolic disorders, and age-related health complications are supporting the rising demand for advanced biliary treatment procedures across the region. North America also benefits from a highly developed healthcare system, strong adoption of advanced interventional technologies, and widespread availability of specialized endoscopic procedures. Growing investments in healthcare innovation and advanced gastroenterology services continue to strengthen regional market expansion.

Prominent companies operating in the Global Biliary Stents Industry include Allium Medical, Becton, Dickinson and Company, Boston Scientific, CONMED, Cook Medical, Cordis, ELLA - CS, ENDO-FLEX, M.I Tech, Medtronic, Merit Medical Systems, MICRO-TECH, OLYMPUS, S&G Biotech, and Taewoong Medical. Companies operating in the biliary stents market are focusing on product innovation, strategic collaborations, and expansion of minimally invasive treatment portfolios to strengthen their market presence. Leading manufacturers are investing heavily in research and development activities to improve stent flexibility, durability, biocompatibility, and anti-migration capabilities. Many organizations are also introducing advanced self-expandable metal stents designed to improve long-term drainage performance and reduce procedure-related complications. In addition, companies are expanding partnerships with hospitals, gastroenterology centers, and healthcare providers to increase product accessibility and strengthen distribution networks. Geographic expansion into emerging healthcare markets, combined with rising investments in training programs for interventional procedures, is further supporting business growth.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of biliary disorders and chronic liver diseases

- 3.2.1.2 Growing adoption of minimally invasive procedures

- 3.2.1.3 Technological advancements in stent design

- 3.2.1.4 Expanding clinical applications of endoscopic luminal stenting

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of stents and associated procedures

- 3.2.2.2 Complications and risks related to bile duct stents

- 3.2.3 Market opportunities

- 3.2.3.1 Development of biodegradable and drug-eluting stents

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by primary research)

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.11 Value chain analysis (Driven by primary research)

- 3.12 Investment & funding analysis (Driven by primary research)

- 3.13 Consumer insights (Driven by primary research)

- 3.14 Treatment infrastructure & clinical adoption landscape

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Metal stents

- 5.3 Polymer stents

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Gallstones

- 6.3 Pancreatic cancer

- 6.4 Bilio-pancreatic leakages

- 6.5 Benign biliary strictures

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Allium Medical

- 9.2 Becton, Dickinson and Company

- 9.3 Boston Scientific

- 9.4 CONMED

- 9.5 Cook Medical

- 9.6 Cordis

- 9.7 ELLA - CS

- 9.8 ENDO-FLEX

- 9.9 M.I Tech

- 9.10 Medtronic

- 9.11 Merit Medical Systems

- 9.12 MICRO-TECH

- 9.13 OLYMPUS

- 9.14 S&G Biotech

- 9.15 Taewoong Medical