|

시장보고서

상품코드

2045709

지오멤브레인 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Geomembrane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

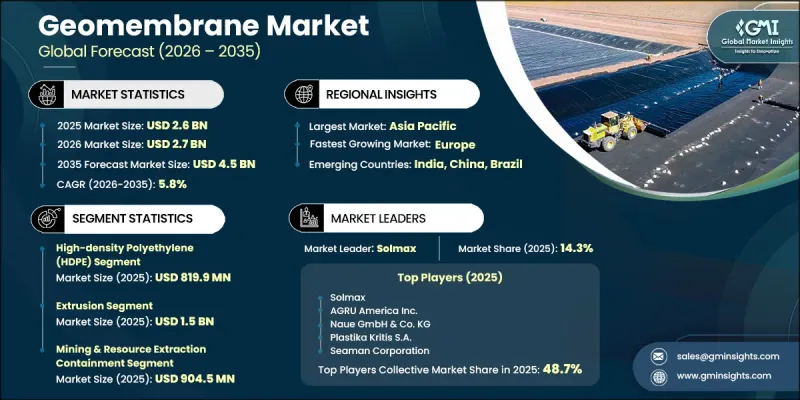

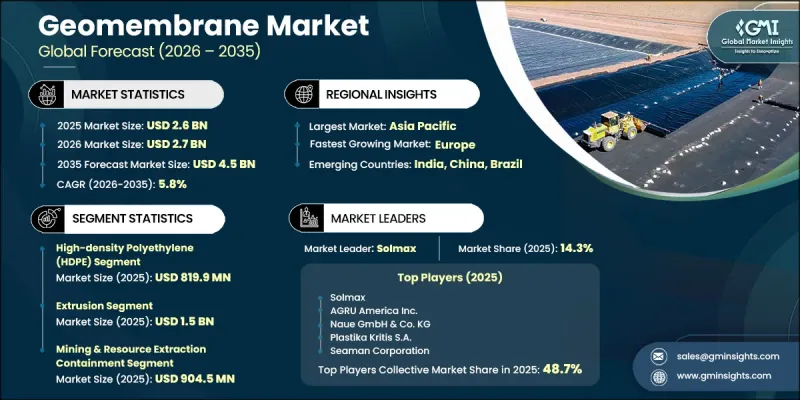

세계의 지오멤브레인 시장은 2025년에 26억 달러로 평가되었고, CAGR 5.8%로 성장할 전망이며, 2035년까지 45억 달러에 이를 것으로 예측됩니다.

지오멤브레인은 다양한 수지를 중합하여 압출 성형 및 캘린더 가공 공정을 거쳐 유연하고 내구성이 뛰어난 시트로 가공한 저투수성 합성 라이너입니다. 불투수성 구조로 인해 우수한 봉쇄 및 차단 성능을 발휘하기 때문에 확실한 환경 보호 및 유체 봉쇄가 요구되는 용도에 필수적인 소재입니다. 이러한 재료는 누출, 침투, 오염을 효과적으로 방지할 수 있기 때문에 폐기물 관리, 광업, 물 인프라 등의 산업에서 널리 사용되고 있습니다. 또한, 화학물질, 자외선, 가혹한 환경 조건에 대한 높은 내성을 가지고 있어 지표면과 지하 모두에 적합합니다. 지속 가능한 엔지니어링 솔루션에 대한 수요가 증가함에 따라 환경 친화적인 프로젝트에서 채택이 더욱 확대되고 있습니다. 고분자 화학 및 제조 공정의 지속적인 기술 발전으로 제품의 성능이 향상되고 두께, 유연성, 기계적 강도를 정밀하게 제어할 수 있게 되었습니다. 압출 성형 및 캘린더링 기술의 발전으로 인장 강도, 펑크 저항성, 내구성이 뛰어난 지오멤브레인을 생산할 수 있게 되어 광산 봉쇄 및 폐기물 관리 시스템과 같은 가혹한 용도 분야에서 성능이 향상되었습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 26억 달러 |

| 예측 시장 규모 | 45억 달러 |

| CAGR | 5.8% |

고밀도 폴리에틸렌(HDPE) 부문은 2025년 8억 1,990만 달러를 차지했습니다. 이 부문은 우수한 불투수성, 내화학성, 매립지 및 광산 작업의 가혹한 봉쇄 용도에 적합하다는 장점으로 인해 지속적으로 성장하고 있습니다. HDPE 배합 기술의 지속적인 발전으로 제품의 내구성이 향상되고, 버진 수지와 재생 수지를 모두 사용하여 비용 효율성과 지속가능성 목표를 달성할 수 있게 되었습니다. 이러한 특성으로 인해 HDPE는 지오멤브레인 시장에서 가장 널리 사용되는 재료 유형으로 그 입지를 더욱 확고히 하고 있습니다.

압출 성형 부문은 2025년에 15억 달러에 달한 것으로 평가되었습니다. 이 제조 공정은 엄격한 품질 요구 사항을 충족하는 균일한 두께와 높은 기계적 강도를 가진 지오멤브레인을 생산할 수 있기 때문에 강한 추진력을 보이고 있습니다. 다층 공압출 기술을 포함한 첨단 압출 시스템에 대한 수요가 증가함에 따라 제품의 성능 특성이 더욱 향상되고 있습니다. 이러한 기술적 진보는 다양한 산업 및 환경 용도 분야에 적합한 고품질 지오멤브레인 생산을 뒷받침하고 있습니다.

북미의 지오멤브레인 시장은 2025년 7억 4,140만 달러로 평가되었고, 2035년까지 13억 달러로 성장할 것으로 예측됩니다. 이 지역의 성장은 주로 폐기물 관리 및 광업 분야에서 신뢰할 수 있는 봉쇄 솔루션에 대한 수요 증가와 점점 더 엄격해지는 환경 보호 규제에 의해 주도되고 있습니다. 시장 확대는 첨단 폴리머 기술 채택, 시공 기술 향상, 지역 내 품질 보증 시스템 강화로 인해 더욱 가속화되고 있습니다. 이러한 요인들이 결합되어 북미에서 지오멤브레인의 사용이 꾸준히 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 원재료별(2022-2035년)

제6장 시장 추산 및 예측 : 기술별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 사용 산업별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.09The Global Geomembrane Market was valued at USD 2.6 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 4.5 billion by 2035.

Geomembranes are low-permeability synthetic liners produced through the polymerization of various resins into flexible, durable sheets using extrusion and calendering processes. Their impermeable structure delivers strong containment and barrier performance, making them essential for applications that require reliable environmental protection and fluid containment. These materials are widely used across industries such as waste management, mining, and water infrastructure due to their effectiveness in preventing leakage, seepage, and contamination. They also offer strong resistance to chemicals, ultraviolet exposure, and harsh environmental conditions, making them suitable for both surface and subsurface applications. Growing demand for sustainable engineering solutions has further strengthened their adoption in environmentally sensitive projects. Continuous technological improvements in polymer chemistry and manufacturing processes have enhanced product performance, allowing precise control over thickness, flexibility, and mechanical strength. Advancements in extrusion and calendering technologies have enabled the production of geomembranes with superior tensile strength, puncture resistance, and durability, improving their performance in demanding applications such as mining containment and waste management systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.6 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 5.8% |

The high-density polyethylene (HDPE) segment accounted for USD 819.9 million in 2025. This segment continues to expand due to its strong impermeability, chemical resistance, and suitability for demanding containment applications in landfills and mining operations. Ongoing advancements in HDPE formulation have improved product durability, while the use of both virgin and recycled resins is supporting cost efficiency and sustainability goals. These characteristics continue to reinforce HDPE as the most widely used material type in the geomembrane market.

The extrusion segment reached USD 1.5 billion in 2025. This manufacturing process is gaining strong traction due to its ability to produce geomembranes with uniform thickness and high mechanical strength that comply with strict quality requirements. Increasing demand for advanced extrusion systems, including multi-layer co-extrusion technologies, is further enhancing product performance characteristics. These technological advancements are supporting the production of high-quality geomembranes suitable for a wide range of industrial and environmental applications.

North America Geomembrane Market is expected to grow from USD 741.4 million in 2025 to USD 1.3 billion by 2035. Growth in the region is primarily driven by rising demand from the waste management and mining sectors for reliable containment solutions, alongside increasingly stringent environmental protection regulations. Market expansion is further supported by the adoption of advanced polymer technologies, improved installation expertise, and stronger quality assurance frameworks across the region. These factors are collectively contributing to the steady growth of geomembrane usage in North America.

Key companies operating in the Global Geomembrane Market include Solmax, AGRU America, Naue GmbH & Co. KG, Seaman Corporation, ATARFIL, S.L, Carlisle SynTec Systems, Plastika Kritis S.A., Global Synthetics, Sotrafa, Juta Ltd, Istanbul Teknik, and Shanghai Yingfan Engineering Material Co., Ltd. Companies in the geomembrane market are focusing on multiple strategic initiatives to strengthen their market position and enhance competitiveness. Leading manufacturers are investing heavily in research and development to improve polymer formulations, enhance durability, and increase resistance to environmental stress. Product innovation is centered on developing high-performance geomembranes with improved tensile strength, flexibility, and puncture resistance. Many players are also integrating recycled materials into production processes to support sustainability goals and reduce environmental impact. Expansion of manufacturing capacity and strengthening of global distribution networks are helping companies improve supply efficiency and reach emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Raw Material

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By raw material

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Raw Material, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 High-Density Polyethylene (HDPE)

- 5.3 Linear Low-Density Polyethylene (LLDPE)

- 5.4 Polyvinyl Chloride (PVC)

- 5.5 Ethylene Propylene Diene Monomer (EPDM)

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Extrusion

- 6.3 Calendering

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Waste Management & Landfill Containment Systems

- 7.3 Mining & Resource Extraction Containment

- 7.4 Water Infrastructure & Municipal Applications

- 7.5 Industrial & Chemical Containment Applications

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Environmental Services & Waste Management Industry

- 8.3 Mining & Natural Resources Industry

- 8.4 Water Utilities & Treatment Facilities

- 8.5 Municipal & Government Infrastructure

- 8.6 Industrial Manufacturing & Chemical Processing

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AGRU America, Inc

- 10.2 ATARFIL, S.L

- 10.3 Carlisle SynTec Systems

- 10.4 Global Synthetics

- 10.5 Istanbul Teknik

- 10.6 Juta Ltd

- 10.7 Naue GmbH & Co. KG

- 10.8 Plastika Kritis S.A.

- 10.9 Seaman Corporation

- 10.10 Shanghai Yingfan Engineering Material Co., Ltd

- 10.11 Solmax

- 10.12 Sotrafa