|

시장보고서

상품코드

2045713

자동차용 TIC 서비스 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive TIC Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

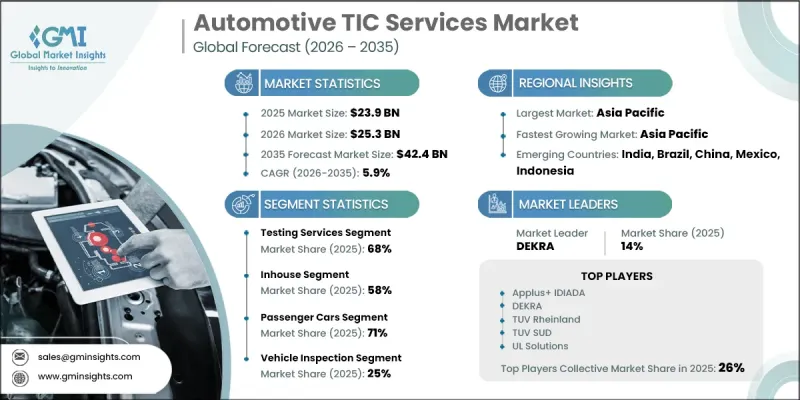

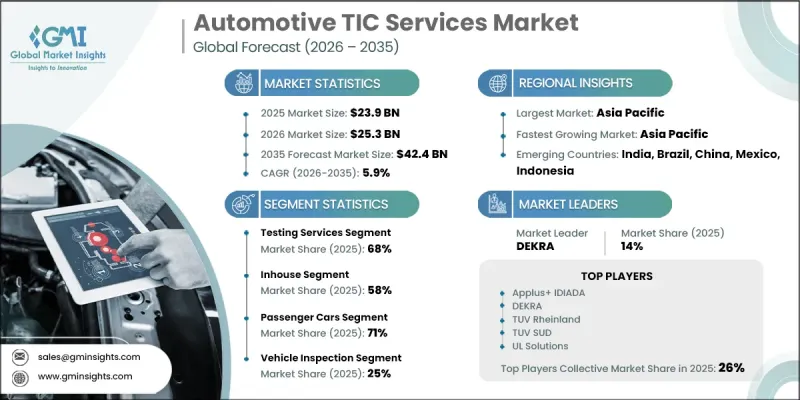

세계의 자동차용 TIC 서비스 시장은 2025년에 239억 달러로 평가되었고 CAGR 5.9%로 성장하여 2035년까지 424억 달러에 이를 것으로 추정되고 있습니다.

규제 당국이 차량 안전, 배기가스 규제, 사이버 보안 요건에 대한 엄격한 기준을 계속 강화함에 따라 시장은 확대되고 있으며, 시험, 검사, 인증 서비스에 대한 의존도가 높아지고 있습니다. 자동차 제조 및 공급망의 세계화는 여러 지역에 걸친 표준화된 컴플라이언스 프레임워크의 필요성을 더욱 높이고 있습니다. 전기 모빌리티의 급속한 발전은 특히 배터리 성능, 열효율, 충전 시스템 등의 분야에서 전문적인 검증 능력에 대한 수요를 증가시키고 있습니다. 동시에 차량에 첨단 소프트웨어 시스템의 통합이 진행됨에 따라 업계의 초점은 커넥티드 기술 및 지능형 기술에 대한 지속적인 검증 프로세스로 이동하고 있습니다. 이 부문의 디지털 전환은 연구 방법론에도 영향을 미치고 있으며, 고급 시뮬레이션 툴을 통해 효율성이 향상되고 개발 기간이 단축되고 있습니다. 또한, 상용차 운영업체들은 운영 신뢰성을 높이고, 규정 준수를 보장하며, 성능을 최적화하기 위해 TIC 서비스를 점점 더 많이 활용하고 있으며, 이는 전체 자동차 생태계의 지속적인 시장 성장에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 239억 달러 |

| 예측 시장 규모 | 424억 달러 |

| CAGR | 5.9% |

시험 서비스 부문은 2025년 68%의 점유율을 차지해, 2026-2035년 연평균 5.4%의 성장률을 보일 것으로 전망됩니다. 이러한 서비스는 안전, 성능 및 배출가스 관련 요구사항 준수를 보장하기 위해 제어 환경과 실제 운영 환경 모두에서 차량 시스템, 부품 및 완성된 유닛을 평가하는 데 중점을 둡니다. 그 범위에는 규제 당국의 승인을 지원하고 제품의 신뢰성을 유지하기 위해 설계된 여러 검증 프로세스가 포함됩니다.

사내 부문은 2025년 58%의 점유율을 차지해, 2035년까지 연평균 4.9%의 성장률을 보일 것으로 전망됩니다. 자동차 제조업체는 사내 TIC(테스트, 검사 및 인증) 기능을 통해 테스트 및 인증 워크플로우를 완벽하게 관리할 수 있으며, 이를 통해 실행 속도를 높이고 데이터 보안을 강화하며 사내 개발 프로세스와의 일관성을 향상시킬 수 있습니다. 그러나 이러한 역량을 유지하려면 고도의 인프라, 기술 전문성, 지속적인 시스템 업그레이드에 대한 막대한 투자가 필요하기 때문에 일관된 테스트 요구사항이 있는 대규모 제조업체에게 더 현실적인 선택이 될 수 있습니다.

미국 자동차 TIC 서비스 시장은 2025년 51억 달러에 달해, 2026년부터 2035년까지 연평균 6.3%의 성장률을 보일 것으로 예측됩니다. 시장 성장은 안전, 배기가스 규제 준수, 첨단 차량 검증 요건을 중시하는 강력한 규제 환경에 의해 뒷받침되고 있습니다. 전기자동차 안전 표준에 대한 관심이 높아지고, 컴플라이언스 프레임워크가 진화함에 따라 미국 전역의 종합적인 TIC 서비스에 대한 수요는 더욱 강화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 산업 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 서비스별, 2022-2035년

제6장 시장 추정 및 예측 : 소싱별, 2022-2035년

제7장 시장 추정 및 예측 : 차량별, 2022-2035년

제8장 시장 추정 및 예측 : 용도별, 2022-2035년

제9장 시장 추정 및 예측 : 지역별, 2022-2035년

제10장 기업 개요

JHS 26.06.11The Global Automotive TIC Services Market was valued at USD 23.9 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 42.4 billion by 2035.

The market is expanding as regulatory authorities continue to enforce stricter standards related to vehicle safety, emissions control, and cybersecurity requirements, increasing the reliance on testing, inspection, and certification services. The globalization of automotive manufacturing and supply chains is further driving the need for standardized compliance frameworks across multiple regions. Rapid advancements in electric mobility are strengthening demand for specialized validation capabilities, particularly in areas such as battery performance, thermal efficiency, and charging systems. At the same time, the growing integration of advanced software systems in vehicles is shifting industry focus toward continuous validation processes for connected and intelligent technologies. Digital transformation within the sector is also influencing testing methodologies, with advanced simulation tools improving efficiency and reducing development timelines. In addition, commercial fleet operators are increasingly leveraging TIC services to enhance operational reliability, ensure compliance, and optimize performance, contributing to sustained market growth across the automotive ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.9 Billion |

| Forecast Value | $42.4 Billion |

| CAGR | 5.9% |

The testing services segment accounted for 68% share in 2025 and is expected to grow at a CAGR of 5.4% from 2026 to 2035. These services focus on assessing vehicle systems, components, and complete units under both controlled and operational environments to ensure adherence to safety, performance, and emission requirements. The scope includes multiple validation processes designed to support regulatory approvals and maintain product reliability.

The in-house segment held a share of 58% in 2025 and is projected to grow at a CAGR of 4.9% through 2035. Internal TIC capabilities enable automotive manufacturers to retain full control over testing and certification workflows, resulting in faster execution, improved data security, and better alignment with internal development processes. However, such capabilities require substantial investments in advanced infrastructure, technical expertise, and continuous system upgrades, making them more viable for large-scale manufacturers with consistent testing needs.

U.S. Automotive TIC Services Market reached USD 5.1 billion in 2025 and is expected to grow at a CAGR of 6.3% between 2026 and 2035. Market growth is supported by a strong regulatory environment that emphasizes safety, emissions compliance, and advanced vehicle validation requirements. Increasing focus on electric vehicle safety standards and evolving compliance frameworks are further strengthening demand for comprehensive TIC services across the country.

Key companies operating in the Automotive TIC Services Market include Applus+, Bureau Veritas, CATARC, DEKRA, Element Materials Technology, Eurofins, Intertek, SGS, TUV Rheinland, TUV SUD, and UL Solutions. Companies in the Automotive TIC Services Market are adopting a range of strategic initiatives to reinforce their competitive positioning and expand their market footprint. They are increasing investments in advanced testing infrastructure, particularly for electric vehicles, connected systems, and emerging automotive technologies. Strategic partnerships and collaborations with automotive manufacturers are being pursued to accelerate innovation and ensure early integration into development cycles. Firms are also expanding their global presence to support multinational clients and meet regional compliance requirements efficiently. Emphasis on digitalization, including the adoption of simulation tools and data-driven testing methods, is improving operational efficiency and reducing turnaround times.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Sourcing

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent regulatory compliance

- 3.2.1.2 Globalization of the automotive industry

- 3.2.1.3 Rising demand for vehicle performance testing

- 3.2.1.4 Consumer demand for quality assurance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced TIC equipment

- 3.2.2.2 Complex regulatory environment

- 3.2.3 Market opportunities

- 3.2.3.1 Growth opportunities in emerging markets

- 3.2.3.2 Development of electric and autonomous vehicles

- 3.2.3.3 Expansion of commercial vehicle TIC services

- 3.2.3.4 Integration of advanced technologies in TIC services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 National Highway Traffic Safety Administration

- 3.6.1.2 Environmental Protection Agency

- 3.6.2 Europe

- 3.6.2.1 European Commission

- 3.6.2.2 United Nations Economic Commission for Europe

- 3.6.3 Asia Pacific

- 3.6.3.1 Ministry of Industry and Information Technology

- 3.6.3.2 Ministry of Road Transport and Highways

- 3.6.4 Latin America

- 3.6.4.1 Agencia Nacional de Transportes Terrestres

- 3.6.4.2 Secretaria de Infraestructura, Comunicaciones y Transportes

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Standards, Metrology and Quality Organization

- 3.6.5.2 National Regulator for Compulsory Specifications

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 Gen AI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Testing services

- 5.3 Inspection services

- 5.4 Certification services

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Sourcing, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 In-house

- 6.3 Outsourced

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Vehicle inspection

- 8.3 Emission testing

- 8.4 Component testing

- 8.5 Telematics

- 8.6 ADAS

- 8.7 Homologation testing

- 8.8 Fuels, fluids and lubricants

- 8.9 Electric systems and components

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Bureau Veritas

- 10.1.2 DEKRA

- 10.1.3 Eurofins Scientific

- 10.1.4 Element Materials Technology

- 10.1.5 Intertek

- 10.1.6 SGS

- 10.1.7 TUV Rheinland

- 10.1.8 TUV SUD

- 10.1.9 UL Solutions

- 10.2 Regional players

- 10.2.1 Applus+ IDIADA

- 10.2.2 Automotive Research Association of India

- 10.2.3 CATARC

- 10.2.4 China Automotive Technology and Research Center

- 10.2.5 Japan Automobile Research Institute

- 10.2.6 Korea Testing Laboratory

- 10.2.7 SOCOTEC

- 10.2.8 TUV NORD

- 10.3 Emerging players

- 10.3.1 ALS

- 10.3.2 CSA

- 10.3.3 MISTRAS