|

시장보고서

상품코드

2045754

산업용 송풍기 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Blower Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

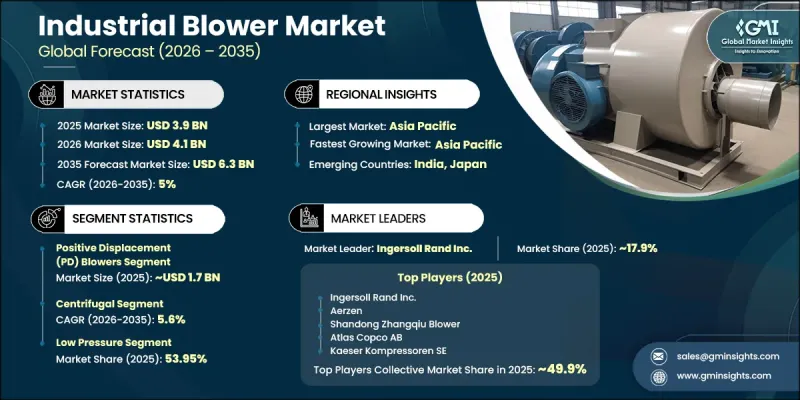

세계의 산업용 송풍기 시장은 2025년에 39억 달러로 평가되었고, CAGR 5%로 성장할 전망이며, 2035년까지 63억 달러에 이를 것으로 예측됩니다.

시장 확대는 전 세계 폐수 처리 및 물 관리 인프라의 정비에 의해 뒷받침되고 있습니다. 도시 인구 증가와 급속한 도시화 추세로 인해 지자체와 산업체들은 폐수 처리 시설의 갱신 및 확장에 대한 압박을 받고 있으며, 산업용 송풍기는 폭기 및 생물학적 처리 공정에서 중요한 역할을 하고 있습니다. 북미, 유럽 연합(EU), 아시아태평양의 환경 규제로 인해 폐수 품질 기준이 더욱 엄격해지면서 처리 시설에서 산업용 송풍기의 도입이 크게 증가하고 있습니다. 동시에 빠르게 발전하는 경제권에서 스마트 물 인프라 및 신규 하수처리 프로젝트에 대한 투자 확대가 장기적인 수요를 뒷받침하고 있습니다. 또한 아시아태평양, 중동, 라틴아메리카의 산업화도 철강 제조, 시멘트 생산, 화학 처리, 식음료 생산, 발전 등 다양한 분야에서 송풍기 시스템에 대한 강력한 수요를 창출하고 있습니다. 중국, 인도, 인도네시아, 중동 국가들의 정부 주도의 인프라 확장 프로그램은 산업단지, 에너지 시스템, 제조 시설에 대한 대규모 투자를 통해 시장 성장을 더욱 촉진하고 있으며, 이는 산업용 송풍기가 제공하는 효율적인 공기 처리 및 가스 운송 기술에 의존하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 39억 달러 |

| 예측 시장 규모 | 63억 달러 |

| CAGR | 5% |

용적식(PD) 송풍기 시장은 2025년 17억 달러 규모에 달했으며, 2026-2035년 연평균 3.7%의 성장률을 보일 것으로 전망됩니다. 이 부문은 작동의 신뢰성, 적응성, 중간 압력 수준에서 안정적인 기류를 필요로 하는 다양한 산업 분야에서 사용되면서 선두 자리를 지키고 있습니다. 용적식 송풍기는 폐수 폭기 시스템, 공기 수송 작업, 화학제품 제조, 광물 처리 용도 등에 널리 사용되고 있습니다. 다양한 압력 조건에서도 안정적인 풍량을 공급할 수 있어 중요한 산업 공정에 매우 적합합니다. 또한, 전 세계 산업 부문에 도입된 기존 PD 송풍기 시스템의 방대한 설치 실적은 지속적인 업데이트 및 유지보수 수요를 창출하여 제조업체의 안정적인 수익원으로 작용하고 있습니다.

원심식 송풍기 부문은 2025년 53%의 점유율을 차지했으며, 2026-2035년 연평균 5.6%의 성장률을 보일 것으로 예측됩니다. 원심식 송풍기는 폐수 처리, 화학 처리, 발전 등의 분야에서 연속적이고 대유량의 공기 공급 용도 분야에서 높은 효율을 발휘하기 때문에 시장을 독점하고 있습니다. 이 시스템은 회전하는 임펠러를 이용하여 기류를 발생시키고 운동 에너지를 압력으로 변환하여 다양한 산업 환경에서 효율적인 성능을 발휘합니다. 무급유 운전, 낮은 유지보수 요구 사항, 에너지 효율적인 구동 시스템과의 호환성으로 인해 운영 비용 절감에 중점을 둔 사업자들이 점점 더 많이 선호하고 있습니다. 도시 하수처리 인프라 및 대규모 폭기 시스템에 대한 투자 확대는 원심식 송풍기 기술의 선도적 지위를 더욱 공고히 하고 있습니다.

중국의 산업용 송풍기 시장은 2025년 5억 9,940만 달러에 달했으며, 2035년까지 6.3%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 광범위한 산업 기반, 하수 처리 인프라의 급속한 확장, 철강, 시멘트, 화학, 식품 가공 등 주요 부문의 활발한 제조 활동으로 인해 이 나라는 계속해서 주요 성장 거점이 되고 있습니다. 수처리 기준 향상에 초점을 맞춘 국가적 환경 이니셔티브와 규제 프레임워크에 따라 지자체 및 산업 용도 분야에서 산업용 송풍기 시스템에 대한 수요가 크게 증가하고 있습니다. 국내 제조업체들은 현지 요구사항에 맞는 비용 효율적인 솔루션으로 입지를 강화하고 있는 반면, 세계 기업들은 고성능 및 기술적으로 진보된 제품 부문에서 확고한 입지를 유지하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 산업 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 유형별(2022-2035년)

제6장 시장 추정 및 예측 : 기술별(2022-2035년)

제7장 시장 추정 및 예측 : 압력별(2022-2035년)

제8장 시장 추정 및 예측 : 최종 용도별(2022-2035년)

제9장 시장 추정 및 예측 : 유통 채널별(2022-2035년)

제10장 시장 추정 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

AJY 26.06.15The Global Industrial Blower Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 6.3 billion by 2035.

Market expansion is supported by the worldwide development of wastewater treatment and water management infrastructure. Increasing urban populations and rapid urbanization trends are compelling municipal authorities and industrial operators to upgrade and expand wastewater treatment facilities, where industrial blowers play a critical role in aeration and biological treatment processes. Environmental regulations across North America, the European Union, and Asia Pacific are enforcing stricter effluent quality standards, which is significantly increasing deployment of industrial blowers in treatment plants. At the same time, rising investments in smart water infrastructure and new sewage treatment projects in rapidly developing economies are sustaining long-term demand. Industrialization across Asia Pacific, the Middle East, and Latin America is also generating strong demand for blower systems across diverse sectors such as steel manufacturing, cement production, chemical processing, food and beverage production, and power generation. Government-led infrastructure expansion programs in countries including China, India, Indonesia, and Middle Eastern economies are further supporting market growth through large-scale investments in industrial parks, energy systems, and manufacturing facilities that rely on efficient air handling and gas movement technologies provided by industrial blowers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 5% |

The positive displacement (PD) blowers segment accounted for USD 1.7 billion in 2025 and is projected to grow at a CAGR of 3.7% from 2026 to 2035. This segment continues to lead due to its operational reliability, adaptability, and wide usage across industries requiring steady airflow at moderate pressure levels. Positive displacement blowers are extensively utilized in wastewater aeration systems, pneumatic conveying operations, chemical manufacturing, and mineral processing applications. Their ability to deliver consistent airflow under varying pressure conditions makes them highly suitable for critical industrial processes. Additionally, the large installed base of existing PD blower systems across global industries is generating continuous replacement and maintenance demand, providing a stable revenue stream for manufacturers.

The centrifugal blower segment held a share of 53% in 2025 and is anticipated to grow at a CAGR of 5.6% from 2026 to 2035. Centrifugal blowers dominate the market because of their high efficiency in continuous, high-volume airflow applications across sectors such as wastewater treatment, chemical processing, and power generation. These systems utilize rotating impellers to generate airflow and convert kinetic energy into pressure, enabling efficient performance across a wide range of industrial conditions. Their oil-free operation, low maintenance requirements, and compatibility with energy-efficient drive systems make them increasingly preferred by operators focused on reducing operational costs. Growing investments in municipal wastewater treatment infrastructure and large-scale aeration systems continue to reinforce the leadership position of centrifugal blower technology.

China Industrial Blower Market captured USD 599.4 million in 2025, with a CAGR of 6.3% through 2035. The country remains a key growth hub due to its extensive industrial base, rapid expansion of wastewater treatment infrastructure, and strong manufacturing activity across major sectors such as steel, cement, chemicals, and food processing. National environmental initiatives and regulatory frameworks focused on improving water treatment standards are significantly boosting demand for industrial blower systems in municipal and industrial applications. Domestic manufacturers continue to strengthen their presence with cost-efficient solutions tailored to local requirements, while global players maintain strong positions in high-performance and technologically advanced product segments.

Major companies operating in the Global Industrial Blower Market include Atlas Copco AB, Ingersoll Rand Inc., Kaeser Kompressoren SE, Aerzen, Xylem Inc., Chart Industries, Sulzer Ltd., Busch Group, Piller Blowers & Compressors GmbH, Ebara Corporation, APG-Neuros, Taiko Kikai Industries Co., Ltd., Elektror airsystems GmbH, Shandong Zhangqiu Blower Co., Ltd., Atlantic Blowers, New York Blower Company, Kay International, Savio Srl, Continental Blower LLC, Anlet Co., Ltd., and Pollrich GmbH. Companies in the industrial blower market are focusing on several strategic initiatives to strengthen their market position and improve long-term competitiveness. Leading manufacturers are investing in advanced engineering technologies to enhance blower efficiency, durability, and energy performance across industrial applications. Product innovation efforts are centered on developing low-maintenance, energy-efficient systems equipped with smart monitoring capabilities and automation features. Companies are also expanding their global manufacturing and distribution networks to better serve growing demand in emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Pressure

- 2.2.5 End-use

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid expansion of wastewater treatment and water management infrastructure globally

- 3.2.1.2 Rising industrialization and manufacturing activity across emerging economies

- 3.2.1.3 Growing deployment of high-speed turbo blowers in energy-efficient aeration applications

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High capital costs and long procurement cycles for industrial-grade blower systems

- 3.2.2.2 Increasing competition from low-cost regional manufacturers reducing pricing power

- 3.2.3 Opportunities

- 3.2.3.1 Growing adoption of smart, IoT-enabled blowers with predictive maintenance capabilities

- 3.2.3.2 Expansion of oil & gas and power generation infrastructure in developing markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (2021-2024) (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium/value/cost-plus) (driven by primary research)

- 3.9.3 Regional price variations

- 3.9.4 Price sensitivity analysis by end-user segment

- 3.10 Trade data analysis (driven by paid data base)

- 3.10.1 Import/export volume and value trends by region (driven by paid data base)

- 3.10.2 Key trade corridors and tariff impact analysis (driven by paid data base)

- 3.10.3 HS code classification (8414.80, 8414.59)

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases and adoption roadmap by segment

- 3.11.3 Predictive maintenance and failure prediction

- 3.11.4 Energy optimization and performance tuning

- 3.11.5 Design optimization and CFD simulation

- 3.11.6 Supply chain and demand forecasting

- 3.11.7 Risks, limitations and regulatory considerations

- 3.12 Capacity and production landscape (driven by primary research)

- 3.12.1 Installed manufacturing capacity by region and key producer (driven by primary research)

- 3.12.2 Capacity utilization rates and expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Positive Displacement (PD) Blowers

- 5.3 Centrifugal Blowers

- 5.4 High Speed Turbo Blowers

- 5.5 Multistage Centrifugal Blowers

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Centrifugal

- 6.3 Axial

Chapter 7 Market Estimates & Forecast, By Pressure, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low Pressure

- 7.3 Medium Pressure

- 7.4 High Pressure

Chapter 8 Market Estimates & Forecast, By End-Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Food & Beverage

- 8.3 Wastewater Treatment

- 8.4 Cement Plant

- 8.5 Steel Plant

- 8.6 Mining

- 8.7 Power Plant

- 8.8 Chemical

- 8.9 Oil and Gas

- 8.10 Aerospace and Defense

- 8.11 Pulp and Paper

- 8.12 Water Treatment Plant

- 8.13 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 Atlas Copco AB

- 11.1.2 Ingersoll Rand Inc.

- 11.1.3 Kaeser Kompressoren SE

- 11.1.4 Aerzen

- 11.1.5 Xylem Inc.

- 11.1.6 Chart Industries

- 11.1.7 Sulzer Ltd.

- 11.2 Regional Champions

- 11.2.1 Shandong Zhangqiu Blower Co., Ltd.

- 11.2.2 Busch Group

- 11.2.3 Piller Blowers & Compressors GmbH

- 11.2.4 Ebara Corporation

- 11.2.5 APG-Neuros

- 11.2.6 Taiko Kikai Industries Co., Ltd.

- 11.2.7 Elektror airsystems GmbH

- 11.3 Emerging & Specialized Players

- 11.3.1 Atlantic Blowers

- 11.3.2 New York Blower Company

- 11.3.3 Kay International

- 11.3.4 Savio Srl

- 11.3.5 Continental Blower LLC

- 11.3.6 Anlet Co., Ltd.

- 11.3.7 Pollrich GmbH