|

시장보고서

상품코드

2045766

폐 스텐트 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Lung Stent Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

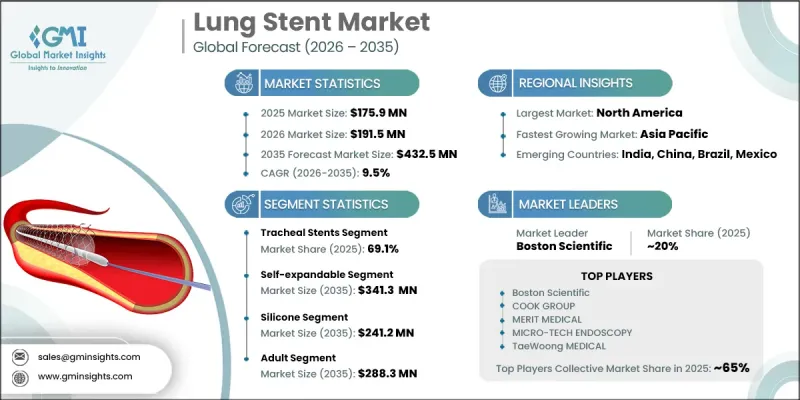

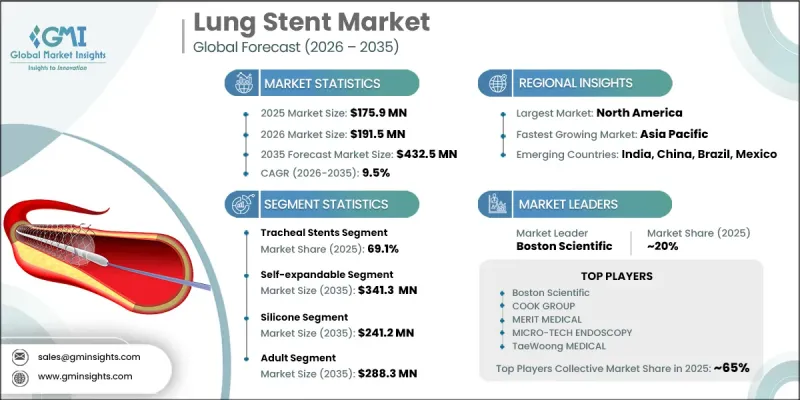

세계의 폐 스텐트 시장은 2025년에 1억 7,590만 달러로 평가되었고, CAGR 9.5%로 성장할 전망이며, 2035년까지 4억 3,250만 달러에 이를 것으로 추정되고 있습니다.

폐 스텐트 산업의 성장은 전 세계 호흡기 질환의 부담 증가, 폐암 유병률 증가, 만성 호흡기 합병증 발생률 증가에 의해 뒷받침되고 있습니다. 일반적으로 기도 스텐트라고 불리는 폐 스텐트는 중증 호흡기 질환, 외상, 감염 또는 구조적 이상으로 인해 기도가 좁아지거나 막힌 환자에서 기도의 개통성을 회복하고 유지하도록 설계된 특수 이식형 의료기기입니다. 이러한 장치는 다양한 임상적 요구 사항을 충족하고 환자의 장기적인 치료 결과를 개선하기 위해 실리콘, 금속 합금 및 하이브리드 재료를 사용하여 제조됩니다. 또한 저침습적 폐 치료법의 발전과 의료시설 전반에 걸친 중재적 호흡기 기술의 채택 확대도 시장에 긍정적인 영향을 미치고 있습니다. 조기 호흡기 중재에 대한 인식이 높아지고 고급 의료 서비스에 대한 접근성이 개선된 것도 시장 확대에 기여하고 있습니다. 또한, 첨단 비혈관용 스텐트 기술 개발에 대한 공공 및 민간 기관의 투자가 증가하면서 제품 혁신이 가속화되고 있습니다. 또한, 만성폐쇄성폐질환(COPD) 및 결핵 치료 후 기도 협착 사례 증가도 전 세계적으로 폐 스텐트 시술에 대한 지속적인 수요를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 1억 7,590만 달러 |

| 예측 시장 규모 | 4억 3,250만 달러 |

| CAGR | 9.5% |

2025년 기관 스텐트 부문은 중증 기관 합병증 환자의 효과적인 기도 안정화 및 즉각적인 기류 회복에 대한 요구가 증가함에 따라 69.1%의 점유율을 차지했습니다. 기관 스텐트는 복잡한 호흡기 중재술에서 중심기도의 개통을 유지하는 데 매우 중요한 역할을 하기 때문에 폐 스텐트 시장의 주요 제품군으로 자리매김하고 있습니다. 이 스텐트는 기도 압박, 구조적 기도 허탈 및 장기적인 지원이 필요한 심각한 호흡기 폐쇄를 동반한 시술에 널리 사용되고 있습니다. 뛰어난 위치 안정성, 신뢰할 수 있는 구조적 무결성, 즉각적인 임상적 개선을 가져오는 능력으로 인해 병원과 전문 호흡기 치료 센터에서의 채택이 확대되고 있습니다.

자가 확장형 부문은 CAGR 9.6%를 기록하며, 2035년까지 3억 4,130만 달러에 달할 것으로 예측됩니다. 자가 확장형 폐 스텐트는 유연성, 불규칙한 기도 구조에 대한 적응성, 삽입 후 지속적인 반경 방향 지지력을 제공하는 능력으로 인해 여전히 높은 지지를 받고 있습니다. 이 스텐트는 압박된 기도나 해부학적으로 문제가 있는 기도에도 효과적으로 적응하고 최소 침습적 치료 접근이 가능하기 때문에 복잡한 기도 시술에 널리 사용되고 있습니다. 기관지경을 이용한 삽입 기술과의 호환성을 통해 의료기관 전반에서 임상적 수용도가 크게 향상되었습니다. 합금 성분, 구조적 성능 및 스텐트 엔지니어링의 지속적인 개선으로 시술의 정확성과 체내 안정성이 더욱 향상되고 있습니다.

2025년 북미의 폐 스텐트 시장은 43.1%의 점유율을 차지했습니다. 이 지역 시장은 미국과 캐나다 전역의 높은 호흡기 질환 유병률과 폐암 진단 건수 증가로 인해 지속적인 수혜를 받고 있습니다. 탄탄한 의료 인프라, 첨단 호흡기 치료 능력, 전문 폐 치료 서비스의 광범위한 이용 가능성은 지역 전체에서 폐 스텐트 기술의 사용을 확대하는 데 도움이 되고 있습니다. 북미에서는 임상의의 높은 전문성과 첨단 기도 관리 기술에 대한 인식이 높아짐에 따라 중재적 호흡기 치료의 도입률도 높은 임베디드니다. 또한, 유리한 상환제도와 호흡기 의료 기술에 대한 투자 확대가 시장 침투를 촉진하고 있습니다. 기관지경 검사의 지속적인 기술 혁신, 환자 검진 프로그램의 개선, 의료비 증가도 이 지역 시장 확대에 더욱 기여하고 있습니다. 호흡기 치료의 성과 향상과 기도 폐쇄로 인한 합병증 감소에 대한 관심이 높아지면서 북미 전역에서 폐 스텐트에 대한 수요가 지속해서 증가할 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별(2022-2035년)

제6장 시장 추산 및 예측 : 디바이스 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 소재별(2022-2035년)

제8장 시장 추산 및 예측 : 환자별(2022-2035년)

제9장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

AJY 26.06.15The Global Lung Stent Market was valued at USD 175.9 million in 2025 and is estimated to grow at a CAGR of 9.5% to reach USD 432.5 million by 2035.

Growth in the lung stents industry is supported by the increasing burden of respiratory disorders, rising prevalence of lung cancer, and growing occurrence of chronic airway complications worldwide. Lung stents, commonly referred to as airway stents, are specialized implantable medical devices designed to restore and maintain airway openness in patients experiencing airway narrowing or obstruction caused by severe respiratory conditions, trauma, infections, or structural abnormalities. These devices are manufactured using silicone, metal alloys, and hybrid materials to address diverse clinical requirements and improve long-term patient outcomes. The market is also benefiting from advancements in minimally invasive pulmonary procedures and increasing adoption of interventional pulmonology techniques across healthcare facilities. Growing awareness regarding early respiratory intervention and improved access to advanced healthcare services are further contributing to market expansion. In addition, rising investments from both public and private organizations in the development of advanced non-vascular stent technologies are accelerating product innovation. Increasing cases of chronic obstructive pulmonary disease and airway narrowing following tuberculosis treatment are also creating sustained demand for lung stent procedures globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $175.9 Million |

| Forecast Value | $432.5 Million |

| CAGR | 9.5% |

The tracheal stents segment accounted for a share of 69.1% in 2025, supported by the growing need for effective airway stabilization and immediate restoration of airflow in patients with severe tracheal complications. Tracheal stents continue to represent the leading product category in the lung stents market because of their critical role in maintaining central airway patency in complex respiratory interventions. These stents are extensively used in procedures involving airway compression, structural airway collapse, and severe respiratory obstruction requiring long-term support. Their strong positional stability, reliable structural integrity, and ability to deliver immediate clinical improvement have increased their adoption across hospitals and specialty respiratory care centers.

The self-expandable segment is anticipated to register a CAGR of 9.6% and reach USD 341.3 million by 2035. Self-expandable lung stents remain highly preferred due to their flexibility, adaptability to irregular airway structures, and ability to provide continuous radial support after placement. These stents are widely used in complex airway procedures because they can conform effectively to compressed or anatomically challenging airway passages while supporting minimally invasive treatment approaches. Their compatibility with bronchoscopic deployment techniques has significantly increased clinical acceptance across healthcare institutions. Continuous improvements in alloy composition, structural performance, and stent engineering have further enhanced procedural precision and in-body stability.

North America Lung Stent Market accounted for 43.1% share in 2025. The regional market continues to benefit from the high prevalence of respiratory diseases and the growing number of lung cancer diagnoses across the United States and Canada. Strong healthcare infrastructure, advanced respiratory treatment capabilities, and widespread availability of specialized pulmonary care services are supporting increased utilization of lung stent technologies throughout the region. North America also demonstrates high adoption of interventional pulmonology procedures, supported by strong clinician expertise and growing awareness regarding advanced airway management techniques. In addition, favorable reimbursement structures and increasing investments in respiratory healthcare technologies are strengthening market penetration. Ongoing innovation in bronchoscopic procedures, improved patient screening programs, and rising healthcare expenditure are further contributing to regional market expansion. The increasing focus on improving respiratory care outcomes and reducing complications associated with airway obstruction is expected to support continued demand for lung stents across North America.

Major companies operating in the Global Lung Stent Market include Boston Scientific, TaeWoong MEDICAL, Teleflex, Renata Medical, HEALTH MICROPORT MEDICAL, EFER ENDOSCOPY, MICRO-TECH ENDOSCOPY, ENDO-FLEX, MERIT MEDICAL, Peytant, COOK GROUP, mi-TECH, NOVATECH, Standard Sci Tech, STENING, and HOOD LABORATORIES. Companies participating in the lung stent market are implementing several strategic initiatives to strengthen their market presence and expand their competitive positioning. Leading manufacturers are investing heavily in research and development activities to improve stent flexibility, biocompatibility, structural durability, and deployment accuracy for complex airway procedures. Businesses are also focusing on product innovation involving hybrid materials, minimally invasive delivery systems, and patient-specific airway solutions to enhance clinical outcomes. Strategic collaborations with hospitals, respiratory care centers, and interventional pulmonology specialists are helping companies improve product adoption and expand their distribution networks. In addition, manufacturers are increasing investments in emerging healthcare markets to strengthen geographic reach and capitalize on growing respiratory care demand.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Device type trends

- 2.2.4 Material trends

- 2.2.5 Patient trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of lung cancer

- 3.2.1.2 Growing incidence of COPD and post-tuberculosis stenosis

- 3.2.1.3 Increasing investments by the public and private organizations for the development of non-vascular stents

- 3.2.1.4 Growing preference for minimally invasive surgeries for respiratory disorders

- 3.2.1.5 Technological advancements in stent design

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of alternative substitute treatment

- 3.2.2.2 Stringent regulations

- 3.2.3 Opportunities

- 3.2.3.1 Integration of digital health and remote monitoring

- 3.2.3.2 Expansion in emerging healthcare markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pricing trend analysis

- 3.6 Technology and innovation landscape (Driven by Primary Research)

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Future market trends (Driven by Primary Research)

- 3.8 Reimbursement scenario

- 3.9 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by Primary Research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Tracheal stents

- 5.3 Bronchial stents

- 5.4 Laryngeal stents

Chapter 6 Market Estimates and Forecast, By Device Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Self-expandable

- 6.3 Balloon-expandable

Chapter 7 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Silicone

- 7.3 Metal

- 7.3.1 Stainless steel

- 7.3.2 Nitinol

- 7.4 Hybrid

Chapter 8 Market Estimates and Forecast, By Patient, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Adult

- 8.3 Pediatric

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Boston Scientific

- 11.2 COOK GROUP

- 11.3 EFER ENDOSCOPY

- 11.4 ENDO-FLEX

- 11.5 HEALTH MICROPORT MEDICAL

- 11.6 HOOD LABORATORIES

- 11.7 MERIT MEDICAL

- 11.8 MICRO-TECH ENDOSCOPY

- 11.9 mi-TECH

- 11.10 NOVATECH

- 11.11 Peytant

- 11.12 Renata Medical

- 11.13 Standard Sci Tech

- 11.14 STENING

- 11.15 TaeWoong MEDICAL

- 11.16 Teleflex