|

시장보고서

상품코드

2045780

배연 탈황 시스템 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Flue Gas Desulfurization System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

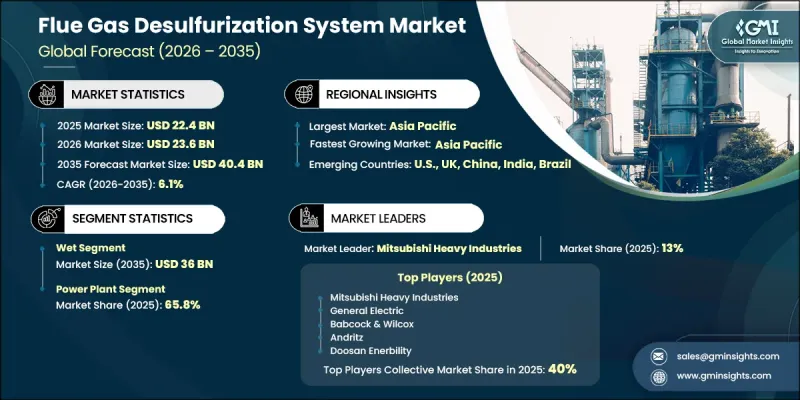

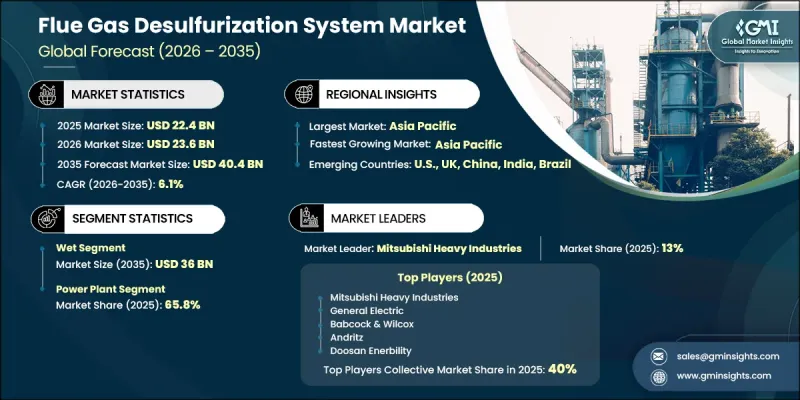

세계의 배연 탈황 시스템 시장은 2025년에 224억 달러로 평가되었고, CAGR 6.1%로 성장할 전망이며, 2035년까지 404억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 배출량과 환경 지속가능성에 대한 압력이 지속적으로 증가하고 있는 세계 에너지 수요 증가에 의해 주도되고 있습니다. 급속한 경제발전으로 산업 활동이 증가하면서 대기오염물질 배출량이 증가함에 따라 효과적인 배출 가스 제어 솔루션의 필요성이 높아지고 있습니다. 정부와 규제 당국은 더욱 엄격한 환경 정책을 시행하고 있으며, 산업계에 유해한 배출을 제한하기 위해 첨단 기술을 도입하도록 압박하고 있습니다. 산업 인프라의 확대와 대규모 생산시설에 대한 투자 증가는 오염도 상승에 더욱 기여하고 있으며, 대기질 관리를 매우 중요한 우선순위로 삼고 있습니다. 환경 문제에 대한 관심이 높아짐에 따라 산업계는 업무 관행 개선을 통해 유해 물질 배출을 줄여야 한다는 압력이 점점 더 커지고 있습니다. 이로 인해 다양한 분야에서 배연 탈황 시스템 및 관련 기술의 도입이 가속화되고 있습니다. 또한, 산업계가 진화하는 환경 기준을 충족시키면서 운영 성능을 유지할 수 있는 신뢰할 수 있는 솔루션을 찾고 있는 가운데, 지속적인 혁신과 시스템 효율성 향상도 시장 확대를 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 224억 달러 |

| 예측 시장 규모 | 404억 달러 |

| CAGR | 6.1% |

습식 배연 탈황 시스템 시장은 2035년까지 360억 달러에 달할 것으로 예측됩니다. 이러한 시스템의 도입 확대는 주로 엄격한 배출 규제와 산업 폐기물의 효율적인 관리의 필요성에 의해 주도되고 있습니다. 황 관련 오염 물질에 대한 높은 제거 효율로 인해, 엄격한 규정 준수 요건에 직면한 업계에서 이러한 시스템이 우선적으로 선택되고 있습니다. 환경 기준이 계속 강화됨에 따라 이러한 시스템에 대한 수요는 꾸준히 증가할 것으로 예측됩니다.

2035년에는 발전소용 용도 부문이 65.8%의 점유율을 차지할 것으로 예측됩니다. 이러한 시스템은 발전 공정에서 발생하는 배출 수준을 제어하기 위해 널리 도입되고 있습니다. 오염물질 배출을 줄이는 역할은 환경 기준 준수를 보장하는 동시에 지속 가능한 에너지 발전을 뒷받침하는 역할을 합니다. 경제 성장과 산업 확장에 따른 전력 수요 증가는 발전 용량 증가로 이어져 배출 제어 기술의 채택을 촉진하고 있습니다.

미국의 배연 탈황 시스템 시장은 배출량 감축을 위한 정부의 투자 및 노력 증가에 힘입어 2025년 21억 달러로 평가되었습니다. 환경 성능 향상에 초점을 맞춘 다양한 프로그램이 첨단 기술 도입을 촉진하고 있으며, 시스템 도입을 보다 비용 효율적으로 만들고 있습니다. 이러한 추세는 향후 몇 년 동안 시장 확대를 위한 기회로 작용할 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 기술별(2022-2035년)

제6장 시장 규모 및 예측 : 용도별(2022-2035년)

제7장 시장 규모 및 예측 : 지역별(2022-2035년)

제8장 기업 개요

AJY 26.06.15The Global Flue Gas Desulfurization System Market was valued at USD 22.4 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 40.4 billion by 2035.

Market growth is driven by the rising global demand for energy, which continues to place pressure on emission levels and environmental sustainability. Rapid economic development has increased industrial activity, leading to higher volumes of air pollutants and intensifying the need for effective emission control solutions. Governments and regulatory bodies are enforcing stricter environmental policies, compelling industries to adopt advanced technologies to limit harmful emissions. Expanding industrial infrastructure and increasing investments in large-scale production facilities are further contributing to elevated pollution levels, making air quality management a critical priority. As environmental concerns gain prominence, industries are under growing pressure to reduce emissions of harmful substances through improved operational practices. This has accelerated the adoption of flue gas desulfurization systems and related technologies across multiple sectors. Continuous innovation and improved system efficiency are also supporting market expansion, as industries seek reliable solutions to meet evolving environmental standards while maintaining operational performance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $22.4 Billion |

| Forecast Value | $40.4 Billion |

| CAGR | 6.1% |

The wet flue gas desulfurization system segment is expected to reach USD 36 billion by 2035. The increasing adoption of these systems is largely driven by stringent emission regulations and the need for efficient management of industrial waste streams. Their ability to deliver high removal efficiency for sulfur-related pollutants has made them a preferred choice across industries facing strict compliance requirements. As environmental standards continue to tighten, demand for these systems is expected to rise steadily.

The power plant applications segment accounted for a share of 65.8% in 2035. These systems are widely deployed to control emission levels generated during power production processes. Their role in reducing pollutant output ensures compliance with environmental norms while supporting sustainable energy generation. Rising electricity demand, driven by economic growth and industrial expansion, has led to increased capacity additions in power generation, thereby boosting the adoption of emission control technologies.

U.S. Flue Gas Desulfurization System Market was valued at USD 2.1 billion in 2025, supported by increasing government investments and initiatives aimed at reducing emissions. Various programs focused on improving environmental performance are encouraging the adoption of advanced technologies, making system deployment more cost-effective. These developments are expected to create favorable opportunities for market expansion in the coming years.

Key companies operating in the Global Flue Gas Desulfurization System Market include Mitsubishi Heavy Industries, General Electric, Babcock & Wilcox, Thermax, Andritz, Doosan Enerbility, Valmet, GEA Group, KC Cottrell, Longking Environmental Protection, Hamon, Kawasaki Heavy Industries, Marsulex Environmental Technologies, Ducon Infratechnologies, AirPoll Technologies, Alstom, Chiyoda, KEPCO, Beijing SPC Environment Protection Tech, GKD, and Ljungstrom. Companies in the flue gas desulfurization system market are implementing strategic initiatives to strengthen their competitive position and expand their global presence. They are focusing on continuous investment in research and development to enhance system efficiency and performance. Strategic partnerships and collaborations are being pursued to expand technological capabilities and enter new markets. Many players are also prioritizing cost optimization and process improvements to deliver competitive solutions. Expanding manufacturing capacities and strengthening supply chain networks are key focus areas for meeting growing demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Technology trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Stringent regulatory framework toward SOx emissions

- 3.3.1.2 Growing electricity demand

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High installation cost

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Cost structure analysis of FGD

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.10 Investment analysis & future prospects

- 3.11 Impact of AI & Generative AI on the market (Solution Core)

- 3.11.1 AI-driven production optimization

- 3.11.2 Predictive maintenance & fault detection

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East & Africa

- 4.2.1.5 Latin America

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.4.1 key developments

- 4.4.2 Merger & acquisition

- 4.4.3 Partnership & collaboration

- 4.4.4 New product launched

- 4.5 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Wet

- 5.3 Dry

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Power plants

- 6.3 Chemical & petrochemical

- 6.4 Cement

- 6.5 Metal processing & mining

- 6.6 Manufacturing

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Indonesia

- 7.4.6 Australia

- 7.4.7 Vietnam

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.5.4 Nigeria

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 AirPoll Technologies

- 8.2 Alstom

- 8.3 Andritz

- 8.4 Babcock & Wilcox

- 8.5 Beijing SPC Environment Protection Tech

- 8.6 Chiyoda

- 8.7 Doosan Enerbility

- 8.8 Ducon Infratechnologies

- 8.9 GEA Group

- 8.10 General Electric

- 8.11 GKD

- 8.12 Hamon

- 8.13 Kawasaki Heavy Industries

- 8.14 KC Cottrell

- 8.15 KEPCO

- 8.16 Ljungstrom

- 8.17 Longking Environmental Protection

- 8.18 Marsulex Environmental Technologies

- 8.19 Mitsubishi Heavy Industries

- 8.20 Thermax

- 8.21 Valmet