|

시장보고서

상품코드

2045781

생수 포장 시장 : 성장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Bottled Water Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

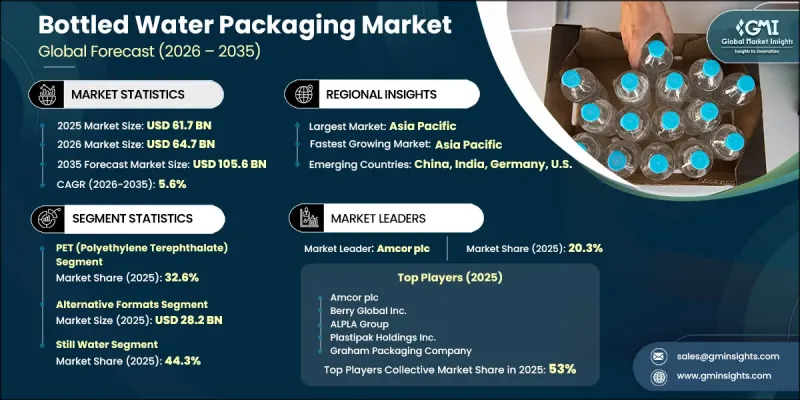

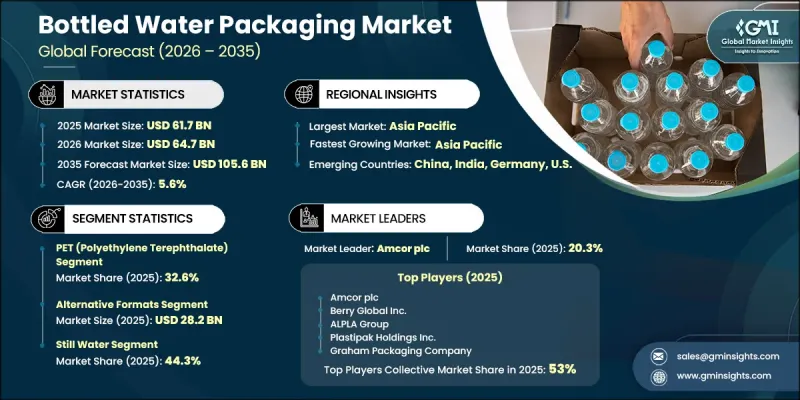

세계의 생수 포장 시장은 2025년에 617억 달러로 평가되었고, CAGR 5.6%로 성장할 전망이며, 2035년까지 1,056억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 소비자들이 건강, 위생, 안전한 수분 보충 솔루션에 대한 관심이 높아짐에 따라 포장된 식수 소비가 증가함에 따라 시장 성장에 힘입고 있습니다. 급속한 도시화와 라이프스타일의 변화도 이동 중 소비에 적합한 휴대성이 높고 편리한 패키지 형태에 대한 수요 증가에 기여하고 있습니다. 조직화된 소매점 및 편의점과 같은 유통 채널을 포함한 소매 인프라의 확장은 제품의 접근성을 지속적으로 향상시켜 전 세계 포장에 대한 수요를 강화하고 있습니다. 또한, 개인 브랜드 제조업체와 지역 생수 브랜드의 부상도 시장에 긍정적인 영향을 미치고 있으며, 이는 여러 제품 카테고리에서 포장량을 증가시키고 있습니다. 포장 효율과 재료 최적화의 지속적인 발전은 생산 능력을 향상시키는 동시에 재료 사용량과 환경에 미치는 영향을 줄임으로써 업계의 확장을 더욱 촉진하고 있습니다. 제조업체들이 지속가능성 목표와 업무 효율성에 초점을 맞추고 있는 가운데, 가볍고 비용 효율적인 포장 솔루션의 중요성이 점점 더 커지고 있습니다. 위생적인 포장 음료와 실용적인 포장 형태에 대한 소비자의 선호도가 높아짐에 따라 선진국과 신흥 시장 모두에서 수요가 증가하고 있으며, 생수 포장 산업은 꾸준히 발전하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 617억 달러 |

| 예측 시장 규모 | 1,056억 달러 |

| CAGR | 5.6% |

PET(폴리에틸렌 테레프탈레이트) 부문은 2025년 32.6%의 점유율을 차지했습니다. PET 포장은 경량 구조, 비용 효율성, 우수한 차단 성능으로 인해 지속적인 수요를 유지하고 있습니다. 이 소재는 대량 생산, 효율적인 운송 및 기존 재활용 시스템과의 호환성을 지원하여 일반 소매 시장 및 상업용 시장에서 생수 제품에 선호되는 포장 솔루션이 되었습니다. 경량 포장과 재활용 가능한 소재에 대한 관심이 높아지면서 전 세계 생수 포장 산업 전반에 걸쳐 PET 병의 채택이 더욱 가속화되고 있습니다.

일회용 병 시장은 2026-2035년 연평균 복합 성장률(CAGR) 6%를 나타낼 것으로 예측됩니다. 이 부문 시장 성장은 현대 도시 생활 방식에 부합하는 휴대용 음료 포장 솔루션에 대한 수요 증가와 충동 구매 행동 증가에 의해 주도되고 있습니다. 일회용 병은 편리성, 취급 용이성 및 빠르게 움직이는 소매 환경에 적합하며, 프리미엄 및 주류 생수 모두에 매우 적합합니다. 여행, 업무, 야외 활동 중 포장된 음료의 소비 증가는 전 세계적으로 일회용 생수 포장에 대한 강력한 수요를 지속적으로 뒷받침하고 있습니다.

북미의 생수 포장 시장은 2025년 31.4%의 점유율을 차지했습니다. 신뢰할 수 있고 위생적인 패키지 식수 솔루션에 대한 소비자의 선호도가 높아지면서 이 지역 시장은 지속적으로 성장하고 있습니다. 잘 구축된 소매 유통 시스템과 도시 및 교외 인구의 높은 생수 보급률은 PET 병, 캡, 멀티팩 솔루션과 같은 1차 포장 제품에 대한 안정적인 수요를 뒷받침하고 있습니다. 편의성, 제품 안전성, 지속 가능한 포장 기술에 대한 관심이 높아지면서 북미 전역 시장 성장에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 소재 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 포장 형태별(2022-2035년)

제7장 시장 추산 및 예측 : 보틀 사이즈별(2022-2035년)

제8장 시장 추산 및 예측 : 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.15The Global Bottled Water Packaging Market was valued at USD 61.7 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 105.6 billion by 2035.

Market growth is fueled by rising consumption of packaged drinking water as consumers increasingly prioritize health, hygiene, and safe hydration solutions. Rapid urbanization and changing lifestyles are also contributing to higher demand for portable and convenient packaging formats suitable for on-the-go consumption. Expanding retail infrastructure, including organized retail stores and convenience distribution channels, continues to improve product accessibility and strengthen packaging demand worldwide. The market is also benefiting from the growing presence of private-label manufacturers and regional bottled water brands, which are increasing packaging volumes across multiple product categories. Continuous advancements in packaging efficiency and material optimization are further supporting industry expansion by improving production capabilities while reducing material usage and environmental impact. Lightweight and cost-effective packaging solutions are becoming increasingly important as manufacturers focus on sustainability goals and operational efficiency. The bottled water packaging industry continues to evolve steadily as consumer preference for hygienic packaged beverages and practical packaging formats strengthens demand across both developed and emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $61.7 Billion |

| Forecast Value | $105.6 Billion |

| CAGR | 5.6% |

The PET (polyethylene terephthalate) segment held a 32.6% share in 2025. PET packaging continues to maintain strong demand due to its lightweight structure, cost-effectiveness, and excellent barrier performance. The material supports high-volume manufacturing, efficient transportation, and compatibility with established recycling systems, making it the preferred packaging solution for bottled water products across mass-market retail and institutional applications. Increasing emphasis on lightweight packaging and recyclable materials is further strengthening the adoption of PET bottles throughout the global bottled water packaging industry.

The single-use bottles segment is expected to grow at a CAGR of 6% during 2026-2035. Market growth within this segment is driven by increasing demand for portable beverage packaging solutions that align with modern urban lifestyles and rising impulse purchasing behavior. Single-use bottle formats offer convenience, easy handling, and compatibility with fast-moving retail environments, making them highly suitable for both premium and mainstream bottled water products. Growing consumption of packaged beverages during travel, work, and outdoor activities continues to support strong demand for single-use bottled water packaging globally.

North America Bottled Water Packaging Market accounted for 31.4% share in 2025. The regional market continues to grow due to strong consumer preference for reliable and hygienic packaged drinking water solutions. Well-established retail distribution systems and high bottled water penetration across urban and suburban populations are supporting consistent demand for primary packaging products, including PET bottles, closures, and multipack solutions. Increasing focus on convenience, product safety, and sustainable packaging technologies is also contributing to market growth throughout North America.

Major companies operating in the Global Bottled Water Packaging Market include Amcor plc, Berry Global Inc., ALPLA Group, Plastipak Holdings Inc., Graham Packaging Company, Gerresheimer AG, O-I Glass Inc., Ardagh Group, Verallia, Ball Corporation, Crown Holdings Inc., Silgan Holdings Inc., RPC Group, RETAL Industries Ltd., and Resilux NV. Companies operating in the bottled water packaging market are adopting several strategic initiatives to strengthen their market position and expand their global footprint. Manufacturers are investing heavily in sustainable packaging technologies, including lightweight bottle designs, recyclable materials, and reduced plastic usage to meet evolving environmental regulations and consumer preferences. Many companies are also expanding production capacities and improving supply chain efficiency to address rising global demand for bottled water packaging solutions. Strategic mergers, acquisitions, and partnerships are helping businesses broaden their geographic reach and diversify product portfolios. In addition, packaging manufacturers are focusing on innovation in barrier technologies, packaging durability, and eco-friendly materials to improve product performance and sustainability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging format trends

- 2.2.3 Bottle size trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumption of bottled water as a hygiene and health necessity

- 3.2.1.2 Urbanization and on-the-go consumption patterns

- 3.2.1.3 Expansion of retail and convenience store networks

- 3.2.1.4 Strong penetration of private-label and regional water brands

- 3.2.1.5 Continuous innovation in lightweight and cost-efficient packaging formats

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising regulatory and environmental pressure on plastic packaging

- 3.2.2.2 Volatility in raw material and resin prices

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of alternative and refill-enabled packaging systems

- 3.2.3.2 Growth of institutional and bulk packaged water formats

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 PET (polyethylene terephthalate)

- 5.3 HDPE (high-density polyethylene)

- 5.4 Glass

- 5.5 Aluminum

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Packaging Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Single-use bottles

- 6.3 Returnable large jugs

- 6.4 Cans

- 6.5 Alternative formats

Chapter 7 Market Estimates and Forecast, By Bottle Size, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Small format (less than 330 ml)

- 7.3 Single-serve (330 ml to 500 ml)

- 7.4 Medium format (501 ml to 1 liter)

- 7.5 Family size (1.1 to 2 liters)

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Still water

- 8.3 Sparkling water

- 8.4 Value-added water

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor plc

- 10.1.2 Berry Global Inc.

- 10.1.3 ALPLA Group

- 10.1.4 Plastipak Holdings Inc.

- 10.1.5 Graham Packaging Company

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 O-I Glass Inc.

- 10.2.1.2 Ball Corporation

- 10.2.1.3 Crown Holdings Inc.

- 10.2.1.4 Silgan Holdings Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 RETAL Industries Ltd.

- 10.2.3 Europe

- 10.2.3.1 Gerresheimer AG

- 10.2.3.2 Ardagh Group

- 10.2.3.3 Verallia

- 10.2.3.4 RPC Group (part of Berry Global)

- 10.2.3.5 Resilux NV

- 10.2.1 North America