|

시장보고서

상품코드

2045795

건설기계 금융 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Construction Equipment Finance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

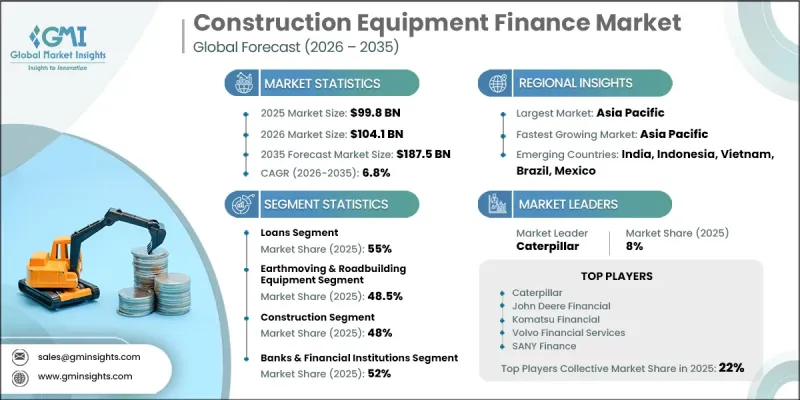

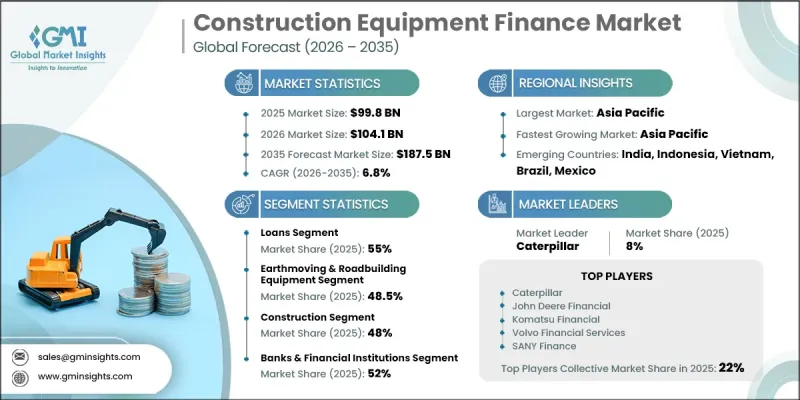

세계의 건설기계 금융 시장은 2025년에 998억 달러로 평가되었고, CAGR 6.8%로 성장할 전망이며, 2035년까지 1,875억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 선진국과 신흥국 모두에서 교통 인프라, 에너지 프로젝트, 주택 개발, 대규모 건설 활동에 대한 투자 증가에 의해 주도되고 있습니다. 자본 집약적인 건설 프로젝트에서 자금 조달 솔루션에 대한 의존도가 높아짐에 따라, 계약자 및 프로젝트 개발자는 재무 유연성을 높이고 유동성을 유지할 수 있는 건설기계 금융 모델을 채택하고 있습니다. 건설 기업들은 굴삭기, 크레인, 로더, 중장비 등 첨단 장비를 초기 투자 없이도 이용할 수 있도록 자금 조달 솔루션을 점점 더 많이 활용하고 있습니다. 대출 및 리스 계약과 같은 자금 조달 옵션을 통해 건설업체는 프로젝트의 동시 진행을 지원하면서 보유 장비의 현대화를 보다 효율적으로 진행할 수 있습니다. 건설 수익의 주기적 특성과 지불 주기의 지연도 기업이 운전 자금 관리의 최적화에 집중하도록 유도하고 있습니다. 자금 조달 솔루션을 통해 기업은 설비 비용을 장기적으로 분산시켜 당장의 재정적 압박을 완화하고 비즈니스 연속성을 향상시킬 수 있습니다. 세계 인프라 개발 이니셔티브의 확대와 건설 활동의 활성화는 여러 산업 분야에 걸쳐 건설기계 금융 서비스에 대한 장기적인 수요를 지속적으로 증가시키고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 998억 달러 |

| 예측 시장 규모 | 1,875억 달러 |

| CAGR | 6.8% |

대출 부문은 55%의 점유율을 차지하고 있으며, 2026-2035년 동안 CAGR 6.4%를 나타낼 것으로 예측됩니다. 기관투자자 및 정부 지원 프로그램을 통해 자금을 조달하는 대규모 인프라 프로젝트에 참여하는 대형 건설업체 및 조직들 사이에서 대출을 통한 자금 조달은 여전히 널리 선호되고 있습니다. 인프라 확장에 대한 투자 증가는 중장비 구매를 지원하기 위해 설계된 구조화 된 기간 대출에 대한 견고한 수요에 기여하고 있습니다. 또한, 금리 환경의 변화로 인해 차입자는 상환의 유연성을 높이고 현금 흐름 관리를 개선할 수 있는 하이브리드 자금 조달 구조를 원하고 있습니다.

토공 및 도로 건설 장비 부문은 2025년 48.5%의 점유율을 차지했으며, 2035년까지 연평균 5.5%의 성장률을 보일 것으로 전망됩니다. 굴삭기, 로더, 불도저, 그레이더와 같은 장비 카테고리는 인프라 개발, 도시 건설, 광업 등 다양한 분야에서 활용되고 있어, 앞으로도 강력한 자금 조달 수요가 예상됩니다. 높은 장비 취득 비용과 사용 주기의 과밀화로 인해 계약자 및 건설회사가 기계 구매 및 갱신 시 금융 솔루션을 이용하는 주요 요인이 되고 있습니다.

미국의 건설기계 금융 시장은 2025년 209억 달러 규모에 달했으며, 2026-2035년 연평균 7.1%의 견조한 성장이 예상됩니다. 미국에서는 금융기관, 제조업체, 산업단체 간의 강력한 협력에 힘입어 고도로 발달된 건설기계 금융 생태계가 유지되고 있습니다. 인프라 현대화 프로젝트 증가와 건설 활동의 확대가 미국 전역의 금융 거래량 증가에 기여하고 있습니다. 또한, 디지털 대출 플랫폼은 계약자 및 중소기업을 위한 심사 절차를 간소화하여 건설기계 금융 솔루션에 보다 빠르고 편리하게 접근할 수 있게 해줍니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 산업 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 자금 조달 형태별(2022-2035년)

제6장 시장 추정 및 예측 : 기기별(2022-2035년)

제7장 시장 추정 및 예측 : 산업 부문별(2022-2035년)

제8장 시장 추정 및 예측 : 프로바이더별(2022-2035년)

제9장 시장 추정 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.15The Global Construction Equipment Finance Market was valued at USD 99.8 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 187.5 billion by 2035.

Market growth is driven by rising investments in transportation infrastructure, energy projects, housing development, and large-scale construction activities across both developed and emerging economies. Increasing reliance on financing solutions for capital-intensive construction projects is encouraging contractors and project developers to adopt equipment financing models that improve financial flexibility and preserve liquidity. Construction businesses are increasingly utilizing financing solutions to access advanced machinery such as excavators, cranes, loaders, and heavy-duty equipment without requiring substantial upfront capital expenditure. Financing options, including loans and leasing arrangements, are enabling contractors to modernize fleets more efficiently while supporting simultaneous project execution. The cyclical nature of construction revenues and delayed payment cycles are also encouraging companies to focus on optimized working capital management. Financing solutions allow businesses to distribute equipment costs over extended periods, reducing immediate financial pressure and improving operational continuity. Growing infrastructure development initiatives and expanding construction activity worldwide continue to strengthen long-term demand for construction equipment financing services across multiple industry sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $99.8 Billion |

| Forecast Value | $187.5 Billion |

| CAGR | 6.8% |

The loans segment held a 55% share and is expected to grow at a CAGR of 6.4% from 2026 to 2035. Loan-based financing remains widely preferred among large contractors and organizations involved in major infrastructure projects supported by institutional or government-backed funding programs. Increasing investment in infrastructure expansion is contributing to strong demand for structured term loans designed to support heavy equipment acquisition. In addition, changing interest rate environments are encouraging borrowers to seek hybrid financing structures that provide greater repayment flexibility and improved cash flow management.

The earthmoving and roadbuilding equipment segment held a 48.5% share in 2025 and is projected to grow at a CAGR of 5.5% through 2035. Equipment categories such as excavators, loaders, bulldozers, and graders continue to witness strong financing demand due to their widespread application across infrastructure development, urban construction, and mining operations. High equipment acquisition costs and intensive usage cycles are major factors encouraging contractors and construction firms to utilize financing solutions when purchasing or upgrading machinery fleets.

U.S. Construction Equipment Finance Market generated USD 20.9 billion in 2025 and is expected to witness robust growth at a CAGR of 7.1% during 2026-2035. The United States maintains a highly developed equipment financing ecosystem supported by strong collaboration between financial institutions, manufacturers, and industry associations. Increasing infrastructure modernization projects and expanding construction activity are contributing to higher financing volumes across the country. In addition, digital lending platforms are simplifying the approval process for contractors and small and medium-sized enterprises, enabling faster and more convenient access to equipment financing solutions.

Leading companies operating in the Global Construction Equipment Finance Market include Bank of America Equipment Finance, BNP Paribas Leasing Solutions, Caterpillar Financial Services, CNH Industrial Capital, J.P. Morgan Equipment Finance, John Deere Financial, Komatsu Financial, Liebherr Financial Services, Volvo Financial Services, and Wells Fargo Equipment Finance. Companies operating in the construction equipment finance market are implementing several strategic initiatives to strengthen their competitive position and expand market presence. Leading providers are focusing on flexible financing models, customized repayment plans, and hybrid loan structures that align with the evolving cash flow requirements of contractors and construction firms. Investments in digital lending technologies and automated approval systems are helping companies accelerate financing processes and improve customer experience. Strategic collaborations with construction equipment manufacturers and dealerships are also enabling finance providers to expand distribution networks and improve equipment accessibility. In addition, companies are strengthening risk management capabilities through advanced analytics and credit assessment technologies to support more efficient financing operations.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Financing type

- 2.2.3 Equipment

- 2.2.4 Industry vertical

- 2.2.5 Provider

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid infrastructure development & urbanization

- 3.2.1.2 High capital cost of equipment

- 3.2.1.3 Growing preference for cash flow optimization

- 3.2.1.4 Expansion of flexible financing models

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment cost

- 3.2.2.2 Maintenance and operational complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of Equipment-as-a-Service (EaaS)

- 3.2.3.2 Emerging market expansion (Asia-Pacific, Africa)

- 3.2.3.3 Integration of digital & fintech solutions

- 3.2.3.4 Sustainable & green financing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 Federal Reserve System (Fed) / OCC / CFPB

- 3.6.1.2 Office of the Superintendent of Financial Institutions (OSFI)

- 3.6.2 Europe

- 3.6.2.1 European Commission - DG FISMA

- 3.6.2.2 European Banking Authority (EBA)

- 3.6.3 Asia Pacific

- 3.6.3.1 China Banking and Insurance Regulatory Commission (CBIRC) / People's Bank of China (PBOC)

- 3.6.3.2 Reserve Bank of India (RBI)

- 3.6.4 Latin America

- 3.6.4.1 Banco Central do Brasil (BCB)

- 3.6.4.2 Comision Nacional Bancaria y de Valores (CNBV)

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Central Bank (SAMA)

- 3.6.5.2 South African Reserve Bank (SARB) / Financial Sector Conduct Authority (FSCA)

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 Gen AI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Financing Type, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Loans

- 5.3 Leases

- 5.3.1 Finance Leases/Capital Leases

- 5.3.2 Operating Leases

- 5.4 Mortgage

Chapter 6 Market Estimates & Forecast, By Equipment, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Earthmoving & roadbuilding equipment

- 6.2.1 Backhoe

- 6.2.2 Excavator

- 6.2.3 Loader

- 6.2.4 Compaction equipment

- 6.2.5 Others

- 6.3 Material handling and cranes

- 6.3.1 Storage and handling equipment

- 6.3.2 Engineered systems

- 6.3.3 Industrial trucks

- 6.3.4 Bulk material handling equipment

- 6.4 Concrete equipment

- 6.4.1 Concrete pumps

- 6.4.2 Crusher

- 6.4.3 Transit mixers

- 6.4.4 Asphalt pavers

- 6.4.5 Batching plants

Chapter 7 Market Estimates & Forecast, By Industry Vertical, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Mining

- 7.4 Forestry & Logging

- 7.5 Oil & Gas

- 7.6 Government & Public Works

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Provider, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Banks & financial institutions

- 8.3 Captive finance companies

- 8.4 Independent lenders

- 8.5 Fintechs & alternative lenders

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Bank of America Equipment Finance

- 10.1.2 BNP Paribas Leasing Solutions

- 10.1.3 Caterpillar Financial Services

- 10.1.4 CNH Industrial Capital

- 10.1.5 J.P. Morgan Equipment Finance

- 10.1.6 John Deere Financial

- 10.1.7 Komatsu Financial

- 10.1.8 Liebherr Financial Services

- 10.1.9 Volvo Financial Services

- 10.1.10 Wells Fargo Equipment Finance

- 10.2 Regional players

- 10.2.1 ANZ Equipment Finance

- 10.2.2 BBVA Equipment Finance

- 10.2.3 DBS Equipment Leasing

- 10.2.4 JCB Finance

- 10.2.5 Santander Equipment Finance

- 10.2.6 TD Equipment Finance

- 10.3 Emerging players

- 10.3.1 Greensill Equipment Finance

- 10.3.2 Sany Finance

- 10.3.3 Stenn International

- 10.3.4 XCMG Finance