|

시장보고서

상품코드

2045841

죽종절제술 기기 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Atherectomy Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

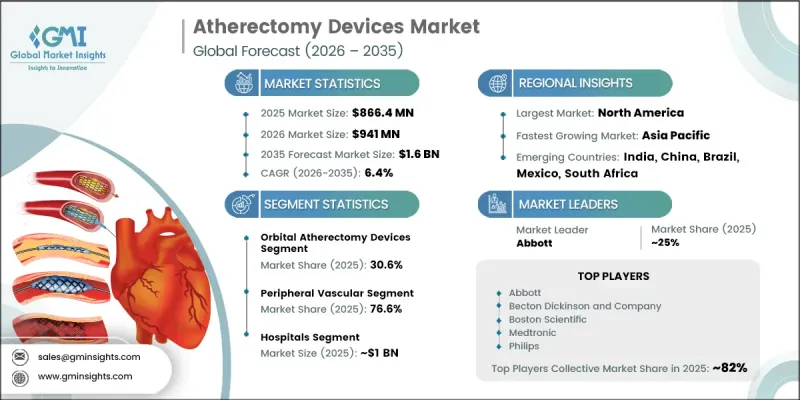

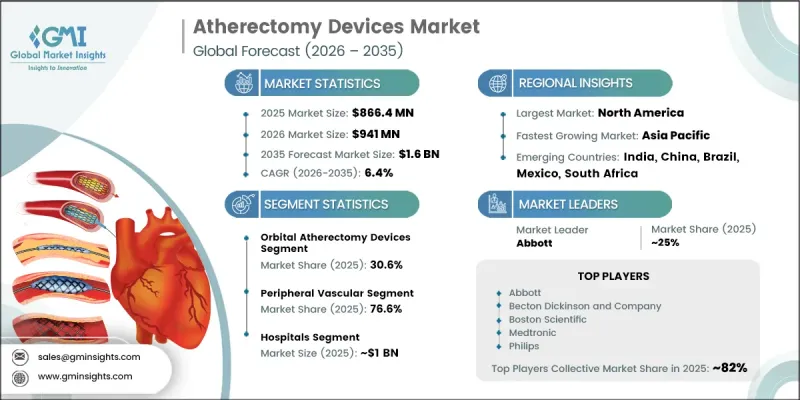

세계의 죽종절제술 기기 시장은 2025년에 8억 6,640만 달러로 평가되었고, CAGR 6.4%로 성장할 전망이며, 2035년까지 16억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 말초동맥질환과 관상동맥질환의 유병률 증가, 전 세계 고령화, 비만과 당뇨병 환자 증가에 힘입어 성장하고 있습니다. 신체 활동 감소와 건강에 해로운 식습관 등 생활습관의 변화도 심혈관 질환의 부담 증가에 기여하고 있으며, 이로 인해 저침습적 혈관 치료 솔루션에 대한 수요가 증가하고 있습니다. 죽종절제술 기기는 침습적 수술의 필요성을 최소화하면서 효과적인 플라크 제거를 가능하게 하는 장치로 널리 받아들여지고 있습니다. 인터벤션 심장학 분야의 지속적인 기술 발전과 의사들의 정밀 혈관 치료에 대한 관심이 높아짐에 따라 제품 채택이 더욱 가속화되고 있습니다. 또한, 의료진은 입원 기간과 회복 기간을 단축하는 환자 중심의 시술에 점점 더 집중하고 있습니다. 첨단 죽상절제술 시스템의 안전성과 성능을 뒷받침하는 임상적 증거 증가와 제품 승인 건수 증가는 세계 죽종절제술 기기 산업에 대한 긍정적인 전망을 더욱 확고히 해주고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 8억 6,640만 달러 |

| 예측 시장 규모 | 16억 달러 |

| CAGR | 6.4% |

죽종절제술 기기는 혈관 질환으로 진단받은 환자의 동맥에 쌓인 플라크를 제거하고 건강한 혈액순환을 회복시키기 위해 고안된 특수 의료기기입니다. 이 시스템은 샌딩, 쉐이빙, 커팅, 레이저를 이용한 플라크 제거 기술 등 여러 가지 첨단 메커니즘을 통해 작동하며, 의사가 개복 수술 없이 막힌 혈관을 치료할 수 있게 해줍니다. 저침습적 심혈관 중재술에 대한 수요가 증가함에 따라 병원 및 전문 의료시설에서 이러한 장치에 대한 수요가 가속화되고 있습니다. 의료 인프라에 대한 투자 확대와 카테터 기술의 혁신도 이러한 장치의 보급을 촉진하고 있습니다. 또한, 의료 시스템에서 혈관 질환의 조기 진단과 적시 치료가 우선시되고 있으며, 이는 죽종절제술 기기 시장에 장기적인 성장 기회를 제공할 것으로 예측됩니다. 시술 효율성 향상, 환자 합병증 감소, 치료 결과 개선으로 인해 죽종절제술 기기 솔루션은 현대 심혈관 의료에서 필수적인 요소로 자리매김하고 있습니다.

궤도 동맥류 제거 장치 부문은 2025년에 30.6%의 점유율을 차지했고, 2035년까지 4억 9,580만 달러에 달할 것으로 예상되며, 예측 기간 동안 연평균 6.3%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 이 카테고리의 강력한 성장은 특히 복잡한 석회화 병변에서 제어되고 균일한 플라크 제거를 달성할 수 있는 궤도식 죽상동맥 절제술 시스템의 능력에 기인합니다. 이 장치들은 주변 동맥 구조를 보존하면서 경화된 플라크를 조심스럽게 깎아내는 첨단 회전 크라운 기술을 채택하여 관상동맥과 말초혈관 수술 모두에서 높은 효과를 발휘합니다. 임상의들 사이에서 정확성을 중시하는 플라크 제거 기술에 대한 선호도가 높아지고 있는 것도 이 부문의 성장을 더욱 촉진하고 있습니다. 기기의 유연성, 탐색 정확도, 시술 안전성에 대한 기술적 진보도 의료시설 전반에 걸쳐 도입을 촉진하고 있습니다.

말초혈관 부문은 2025년 76.6%의 점유율을 차지했으며, 죽상동맥경화증 치료 기기 시장에서 선두를 유지했습니다. 전 세계적으로 말초동맥질환(PAD)의 부담이 증가함에 따라 효과적인 혈관 형성 및 플라크 관리 기술에 대한 수요가 지속적으로 증가하고 있습니다. 흡연, 당뇨병, 비만, 노화에 따른 혈관 합병증 증가율은 PAD의 유병률 증가에 기여하고 있으며, 이에 따라 시장 확대를 뒷받침하고 있습니다. 죽종절제술 기기는 혈류를 개선하고 동맥폐쇄의 심각성을 줄일 수 있어 말초혈관 치료에서 점점 더 중요성이 커지고 있습니다. 또한, 이러한 장치는 회복 기간이 짧고 환자의 예후를 개선할 수 있는 최소 침습적 치료 옵션을 제공하기 때문에 의사들의 지지를 받고 있습니다.

2025년, 북미의 죽종절제술 기기 시장은 58.8%의 점유율을 차지했습니다. 이 지역, 특히 말초동맥질환과 관상동맥질환 환자 수가 여전히 많은 미국에서는 첨단 심혈관 치료 기술에 대한 수요가 꾸준히 증가하고 있습니다. 비만, 당뇨병, 좌식 생활습관 증가는 혈관 중재술이 필요한 환자 수 증가에 기여하고 있습니다. 이 지역은 고도로 발달된 의료 인프라, 풍부한 보험 상환 제도, 혁신적인 의료 기술의 빠른 도입의 혜택을 누리고 있습니다. 북미 전역의 의료 서비스 제공업체들은 치료 효율성과 환자 회복 결과를 개선하기 위해 최소침습적 시술의 사용을 점점 더 많이 늘리고 있습니다. 또한, 심혈관 연구에 대한 투자 확대, 첨단 중재적 치료에 대한 접근성 확대, 혈관 질환 관리에 대한 인식이 높아지면서 이 지역 시장의 성장을 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 산업 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품별(2022-2035년)

제6장 시장 추정 및 예측 : 용도별(2022-2035년)

제7장 시장 추정 및 예측 : 최종 용도별(2022-2035년)

제8장 시장 추정 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

AJY 26.06.15The Global Atherectomy Devices Market was valued at USD 866.4 million in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 1.6 billion by 2035.

Market expansion is fueled by the increasing incidence of peripheral artery disease and coronary artery disease, along with the rising global elderly population and growing cases of obesity and diabetes. Changing lifestyles, including reduced physical activity and unhealthy dietary patterns, are also contributing to the increasing burden of cardiovascular disorders, thereby strengthening demand for minimally invasive vascular treatment solutions. Atherectomy devices are gaining wider acceptance because they support effective plaque removal while minimizing the need for invasive surgical procedures. Continuous technological advancements in interventional cardiology, combined with increasing physician preference for precision-based vascular treatments, are further supporting product adoption. In addition, healthcare providers are increasingly focusing on patient-centered procedures that reduce hospital stays and recovery time. Rising clinical evidence validating the safety and performance of advanced atherectomy systems, along with a growing number of product approvals, continues to reinforce the positive outlook for the global atherectomy devices industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $866.4 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 6.4% |

Atherectomy devices are specialized medical instruments designed to eliminate plaque accumulation from arteries and restore healthy blood circulation in patients diagnosed with vascular disorders. These systems operate through several advanced mechanisms, including sanding, shaving, cutting, and laser-based plaque removal technologies, allowing physicians to address blocked vessels without open surgery. Growing preference for minimally invasive cardiovascular interventions is accelerating demand for these devices across hospitals and specialty care facilities. Increasing investments in healthcare infrastructure and innovation in catheter-based technologies are also encouraging broader adoption. Furthermore, healthcare systems are prioritizing early diagnosis and timely treatment of vascular diseases, which is expected to create long-term growth opportunities for the atherectomy devices market. Enhanced procedural efficiency, reduced patient complications, and improved treatment outcomes continue to position atherectomy solutions as a critical component of modern cardiovascular care.

The orbital atherectomy devices segment accounted for a share of 30.6% in 2025 and is anticipated to reach USD 495.8 million by 2035, expanding at a CAGR of 6.3% over the forecast period. Strong growth within this category is largely linked to the ability of orbital atherectomy systems to deliver controlled and uniform plaque modification, particularly in complex calcified lesions. These devices utilize advanced rotating crown technology that carefully sands hardened plaque while preserving the surrounding arterial structure, making them highly effective in both coronary and peripheral vascular procedures. Increasing preference among clinicians for precision-driven plaque removal techniques is further supporting segment growth. Technological improvements in device flexibility, navigation accuracy, and procedural safety are also encouraging adoption across healthcare facilities.

The peripheral vascular segment captured a share of 76.6% in 2025, maintaining its leading position within the atherectomy devices market. The growing global burden of peripheral artery disease continues to create significant demand for effective vessel preparation and plaque management technologies. Increasing rates of smoking, diabetes, obesity, and aging-related vascular complications are contributing to the rising prevalence of PAD, thereby supporting market expansion. Atherectomy procedures are becoming increasingly important in peripheral vascular treatments due to their ability to improve blood flow and reduce the severity of arterial blockages. Physicians are also favoring these devices because they offer minimally invasive treatment options with shorter recovery periods and improved patient outcomes.

North America Atherectomy Devices Market held a share of 58.8% in 2025. The region continues to experience strong demand for advanced cardiovascular treatment technologies, particularly in the United States, where cases of peripheral artery disease and coronary artery disease remain high. The increasing prevalence of obesity, diabetes, and sedentary lifestyles has contributed to the growing patient population requiring vascular interventions. The region benefits from a highly developed healthcare infrastructure, strong reimbursement systems, and rapid adoption of innovative medical technologies. Healthcare providers across North America are increasingly utilizing minimally invasive procedures to improve treatment efficiency and patient recovery outcomes. In addition, growing investments in cardiovascular research, expanding access to advanced interventional care, and rising awareness regarding vascular disease management continue to reinforce regional market growth.

Key companies operating in the Global Atherectomy Devices Market include Abbott, Medtronic, Boston Scientific, Philips, Becton Dickinson and Company, AVINGER, MicroPort, Nipro, Angiodynamics, Ra Medical Systems, Rex Medical, and Cardio Flow. These companies are actively focusing on product innovation, strategic partnerships, and expansion of their cardiovascular treatment portfolios to strengthen their market presence and improve competitive positioning within the global atherectomy devices industry. Companies operating in the atherectomy devices market are increasingly adopting strategic initiatives focused on innovation, geographic expansion, and portfolio diversification to strengthen their competitive position. Major industry participants are investing heavily in research and development activities to introduce technologically advanced devices with improved precision, safety, and procedural efficiency. Partnerships with hospitals, cardiovascular centers, and healthcare providers are helping companies expand product accessibility and improve physician adoption rates. Many manufacturers are also focusing on regulatory approvals and clinical trials to validate product performance and accelerate commercialization opportunities. In addition, businesses are expanding their distribution networks across emerging economies to capture growing demand for minimally invasive vascular treatments.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in preference for minimally invasive procedures

- 3.2.1.2 Growing target patient population

- 3.2.1.3 Technological advancements in atherectomy devices

- 3.2.1.4 Rising prevalence of peripheral arterial diseases (PAD)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and associated procedures

- 3.2.2.2 Steep learning curve and operator dependency

- 3.2.3 Market opportunities

- 3.2.3.1 Geographic expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by primary research)

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.11 Value chain analysis

- 3.12 Customer insights (Driven by primary research)

- 3.13 Start-up scenarios

- 3.14 Investment & funding analysis (Driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Products, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Orbital atherectomy devices

- 5.3 Laser atherectomy devices

- 5.4 Directional atherectomy devices

- 5.5 Rotational atherectomy devices

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Peripheral vascular applications

- 6.3 Coronary applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 angiodynamics

- 9.3 AVINGER

- 9.4 Becton Dickinson and Company

- 9.5 Boston Scientific

- 9.6 Cardio Flow

- 9.7 Medtronic

- 9.8 MicroPort

- 9.9 Nipro

- 9.10 Philips

- 9.11 Ra Medical Systems

- 9.12 Rex Medical