|

시장보고서

상품코드

2045863

에어 크레인 헬리콥터 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Air Crane Helicopter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

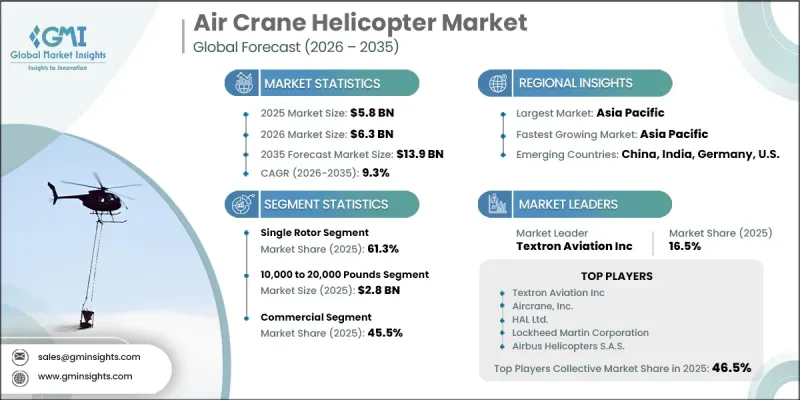

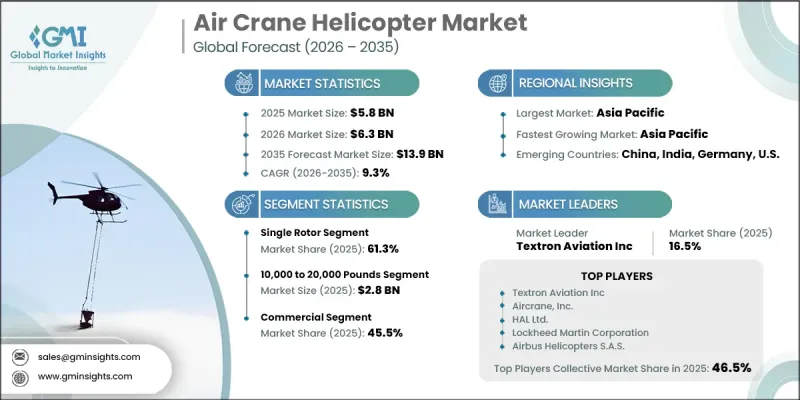

세계의 에어 크레인 헬리콥터 시장은 2025년에 58억 달러로 평가되었고, CAGR 9.3%로 성장할 전망이며, 2035년까지 139억 달러에 이를 것으로 추정되고 있습니다.

에어 크레인 헬리콥터 산업 전반의 성장은 공중 소방 활동에 대한 수요 증가, 대규모 인프라 개발을 위한 중량물 운반용 헬리콥터 도입 확대, 유틸리티 및 에너지 분야에서의 유지보수 활동 확대에 의해 주도되고 있습니다. 또한, 신속한 전개와 높은 적재 능력이 필수적인 긴급 대응 및 재난 복구 활동에서 공중 플랫폼의 사용 확대도 시장에 긍정적인 영향을 미치고 있습니다. 정부와 민간 사업자들은 운영 효율성과 임무 수행 능력을 향상시키기 위해 헬리콥터 기체 현대화에 대한 투자를 점점 더 늘리고 있습니다. 유연한 임대 모델과 서비스 기반 운영 체제는 소유 비용을 절감하고 사업자의 이용 편의성을 향상시켜 도입을 더욱 촉진하고 있습니다. 각 산업계가 열악한 환경에서 대형 장비와 자재를 효율적으로 운송할 수 있는 방법을 모색하는 가운데, 첨단 중량물 운송 항공 솔루션에 대한 수요는 계속 증가하고 있습니다. 적재량 최적화, 비행 안정성, 운항 안전에 초점을 맞춘 기술 발전도 시장 성장을 가속하고 있습니다. 또한, 기후 변화와 관련된 비상사태 증가와 인프라 복구 프로젝트의 확대는 세계 에어 크레인 헬리콥터 시장의 지속적인 성장 기회를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 58억 달러 |

| 예측 시장 규모 | 139억 달러 |

| CAGR | 9.3% |

산불 발생 빈도와 심각성이 계속 증가함에 따라 공중 진화 솔루션에 대한 수요가 증가함에 따라 에어 크레인 헬리콥터 시장은 강력한 모멘텀을 보이고 있습니다. 대형 수송헬기는 대량의 화물을 운반하고, 정확한 공중 소방 지원을 제공하며, 외딴 지역이나 접근이 어려운 지역에서도 효과적으로 운용할 수 있어 선호도가 높아지고 있습니다. 신속한 긴급 대응과 중요 인프라의 조기 복구가 점점 더 중요해짐에 따라 대용량 공중 시스템에 대한 의존도도 더욱 높아지고 있습니다. 비상사태 관리 업무 전반에 걸쳐 효율적인 중량물 운반 장비에 대한 지속적인 수요가 업계의 장기적인 확장을 뒷받침하고 있습니다. 또한, 인프라 정비 활동의 활성화, 유틸리티 활동의 확대, 재난 대응 임무 증가, 그리고 진행 중인 기체 교체 계획이 결합되어 에어 크레인 헬리콥터 산업의 꾸준한 발전에 기여하고 있습니다.

탠덤 로터 기계 부문은 2035년까지 연평균 복합 성장률(CAGR) 10%를 나타낼 것으로 예측됩니다. 이 부문의 성장은 중량물 운반 및 재난 대응 임무에서 적재 능력 향상, 리프트 밸런스 개선, 운영 효율성 향상에 대한 수요 증가에 힘입어 성장세를 보이고 있습니다. 탠덤 로터형 헬리콥터의 설계는 무게 배분을 개선하고 복잡한 항공 작업에서 대형화물을 보다 안전하게 운송할 수 있도록 합니다. 이러한 성능상의 이점은 가혹한 운영 환경에서의 도입을 가속화하고, 세계 에어 크레인 헬리콥터 시장에서 이 부문의 성장 잠재력을 강화합니다.

2만 파운드 이상 부문은 2026-2035년 연평균 복합 성장률(CAGR) 10.6%를 나타낼 것으로 예측됩니다. 대형 건설 프로젝트 및 재난 복구 활동에 따른 초중량물 운송 항공 업무에 대한 수요 증가가 이 카테고리의 확장을 주도하고 있습니다. 이 헬리콥터는 적재 능력이 낮은 항공 플랫폼이 감당할 수 없는 대형 기계, 인프라 부품 및 중요 장비를 운송할 수 있습니다. 극도로 까다로운 운영 요건에 대응할 수 있는 능력은 다양한 산업 분야에서 대용량 에어 크레인 헬리콥터의 급속한 보급에 크게 기여하고 있습니다.

북미의 에어 크레인 헬리콥터 시장은 2025년 35.4%의 점유율을 차지했습니다. 이 지역 시장 성장은 심각한 산불 및 기후 변화와 관련된 자연 재해에 대한 노출이 증가함에 따라 촉진되고 있습니다. 화재 시즌이 길어지고 환경 문제가 심각해짐에 따라 지역 전체에서 대형 운반용 공중 소화 시스템에 대한 의존도가 높아지고 있습니다. 또한, 에어 크레인 헬리콥터에 대한 수요는 유틸리티 인프라 업그레이드, 전력망 내결함성 향상 프로그램, 노후화된 인프라 네트워크의 개보수를 위한 지속적인 투자에 의해 뒷받침되고 있습니다. 비상사태 대비와 재난 대응 능력에 대한 관심이 높아짐에 따라 향후 몇 년 동안 북미의 에어 크레인 헬리콥터 산업은 더욱 강화될 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 로터 시스템별(2022-2035년)

제6장 시장 추산 및 예측 : 외부 부하 용량별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.15The Global Air Crane Helicopter Market was valued at USD 5.8 billion in 2025 and is estimated to grow at a CAGR of 9.3% to reach USD 13.9 billion by 2035.

Growth across the air crane helicopter industry is driven by rising demand for aerial firefighting operations, increasing deployment of heavy-lift helicopters for large infrastructure developments, and expanding maintenance activities across utility and energy sectors. The market is also benefiting from growing use of aerial platforms in emergency response and disaster recovery operations where rapid deployment and heavy payload capabilities are essential. Governments and private operators are increasingly investing in modernizing helicopter fleets to improve operational efficiency and mission performance. Flexible leasing models and service-based operational frameworks are further encouraging adoption by reducing ownership costs and improving accessibility for operators. Demand for advanced heavy-lift aviation solutions is continuing to rise as industries seek efficient methods for transporting oversized equipment and materials in challenging environments. Technological advancements focused on payload optimization, flight stability, and operational safety are also strengthening market growth. In addition, increasing climate-related emergencies and infrastructure rehabilitation projects are creating sustained opportunities for the global air crane helicopter market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.8 Billion |

| Forecast Value | $13.9 Billion |

| CAGR | 9.3% |

The air crane helicopter market is witnessing strong momentum due to the increasing requirement for aerial firefighting solutions as wildfire incidents continue to intensify in frequency and severity. Heavy-lift helicopters are gaining preference because of their ability to carry substantial payloads, deliver accurate aerial suppression support, and operate effectively in remote or inaccessible areas. Rising emphasis on rapid emergency response and faster restoration of critical infrastructure is further increasing dependence on high-capacity aerial systems. Continued demand for efficient heavy-lift aircraft across emergency management operations is supporting long-term industry expansion. In addition, growing infrastructure activities, expanding utility operations, increasing disaster response missions, and ongoing fleet modernization initiatives are collectively contributing to the steady development of the air crane helicopter industry.

The tandem rotor segment is anticipated to register a CAGR of 10% throughout 2035. Segment growth is being supported by increasing demand for improved payload handling capabilities, enhanced lift balance, and greater operational efficiency during heavy-lift and disaster response missions. Tandem rotor helicopter designs provide improved weight distribution and support safer transportation of oversized cargo during complex aerial operations. These performance advantages are accelerating adoption across demanding operational environments and strengthening the segment's growth potential within the global air crane helicopter market.

The above 20,000 pounds segment is projected to grow at a CAGR of 10.6% during 2026-2035. Increasing demand for ultra-heavy-lift aviation operations associated with large-scale construction projects and disaster recovery activities is driving expansion within this category. These helicopters can transport oversized machinery, infrastructure components, and critical equipment that cannot be managed through lower-capacity aerial platforms. Their ability to support highly demanding operational requirements is contributing significantly to the rapid adoption of high-capacity air crane helicopters across multiple industries.

North America Air Crane Helicopter Market accounted for 35.4% share in 2025. Market growth across the region is being fueled by increasing exposure to severe wildfires and climate-related natural disasters. Extended fire seasons and rising environmental challenges are increasing reliance on heavy-lift aerial firefighting systems throughout the region. Demand for air crane helicopters is also being supported by ongoing investments in utility infrastructure upgrades, grid resilience programs, and rehabilitation of aging infrastructure networks. Growing focus on emergency preparedness and disaster response capabilities is expected to further strengthen the North American air crane helicopter industry over the coming years.

Major companies operating in the Global Air Crane Helicopter Market include Airbus Helicopters S.A.S., HAL Ltd., Aircrane, Inc., Columbia Helicopters, Erickson Incorporated, High Performance Helicopters Corp, KAMAN CORPORATION, Lockheed Martin Corporation, Russian Helicopters, HeliQwest, Textron Aviation Inc, and The Boeing Company. Companies active in the air crane helicopter industry are adopting several strategic initiatives to strengthen their market foothold and improve long-term competitiveness. Leading manufacturers are investing in fleet modernization programs focused on improving payload capacity, operational safety, and fuel efficiency. Many companies are also expanding service-based business models and flexible leasing solutions to attract a broader customer base and reduce operational costs for end users. Strategic collaborations with government agencies, emergency response organizations, and infrastructure contractors are helping businesses secure long-term operational contracts. In addition, manufacturers are prioritizing technological advancements related to flight stability, navigation systems, and heavy-lift performance capabilities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Rotor system trends

- 2.2.2 External load capacity trends

- 2.2.3 Application trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for aerial firefighting operations

- 3.2.1.2 Growth in infrastructure construction and heavy lift requirements

- 3.2.1.3 Expansion of utility maintenance and energy sector activities

- 3.2.1.4 Increased use in disaster relief and emergency response

- 3.2.1.5 Fleet modernization and commercial leasing models

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High operating and maintenance costs of air crane helicopters

- 3.2.2.2 Regulatory and operational constraints in complex airspace environments

- 3.2.3 Market opportunities

- 3.2.3.1 Conversion of legacy heavy-lift operations to specialized aerial solutions

- 3.2.3.2 Growing cross-border contracting and seasonal deployment models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Rotor System, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Single rotor

- 5.3 Tandem rotor

Chapter 6 Market Estimates and Forecast, By External Load Capacity, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Up to 10,000 pounds

- 6.3 10,000 to 20,000 pounds

- 6.4 Above 20,000 pounds

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Industrial & infrastructure work

- 7.3 Aerial firefighting

- 7.4 Logging & forestry operations

- 7.5 Disaster relief & emergency response

- 7.6 Military heavy-lift operations

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government

- 8.4 Military

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Textron Aviation Inc

- 10.1.2 Aircrane, Inc.

- 10.1.3 HAL Ltd.

- 10.1.4 Lockheed Martin Corporation

- 10.1.5 Airbus Helicopters S.A.S.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Columbia Helicopters

- 10.2.1.2 Erickson Incorporated

- 10.2.1.3 KAMAN Corporation

- 10.2.1.4 HeliQwest

- 10.2.2 Asia Pacific

- 10.2.2.1 Russian Helicopters

- 10.2.3 Europe

- 10.2.3.1 The Boeing Company

- 10.2.4 Middle East & Africa

- 10.2.4.1 High Performance

- 10.2.4.2 Helicopters Corp

- 10.2.1 North America