|

시장보고서

상품코드

2061283

EV용 차세대 전고체 배터리 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)EV Next-Generation Solid-State Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

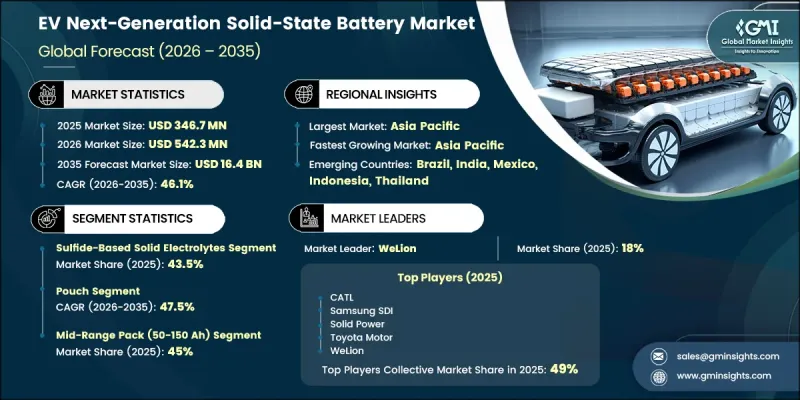

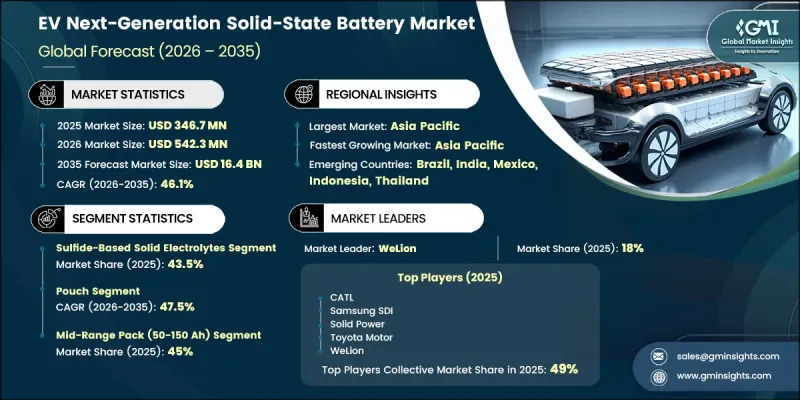

세계의 EV용 차세대 전고체 배터리 시장은 2025년에 3억 4,670만 달러로 평가되며, 2035년까지 CAGR 46.1%로 성장하며, 164억 달러에 달할 것으로 추정되고 있습니다.

자동차 업계가 첨단 전동 모빌리티 솔루션으로의 전환을 가속화하는 가운데, 전기자동차용 차세대 전고체 배터리 산업은 큰 성장세를 보이고 있습니다. 전기자동차에 대한 수요가 증가함에 따라 배터리 제조사와 자동차 제조사들은 효율 향상과 주행 성능 강화를 실현할 수 있는 차세대 배터리 기술에 막대한 투자를 계속하고 있습니다. 전고체 배터리는 더 높은 에너지 밀도를 제공하며, 컴팩트한 배터리 크기를 유지하면서도 전기자동차의 주행 거리를 연장할 수 있으며, 큰 주목을 받고 있습니다. 충전 시간 단축에 대한 소비자의 기대가 높아지는 것도 시장 전반의 급속한 기술 발전에 기여하고 있습니다. 첨단 배터리 구조는 이온 전도성 향상과 출력 증대를 지원하며, 충전 시간 단축과 차량 전반의 편의성 향상에 기여하고 있습니다. 안전성은 전기자동차용 차세대 전고체 배터리 시장의 보급을 지원하는 또 다른 주요 성장 요인입니다. 기존 배터리 기술과 비교했을 때, 전고체 시스템은 열적 안정성이 향상되고 안전 위험이 감소하므로 전기자동차에 적용하는 데 있으며, 점점 더 매력적인 대안이 되고 있습니다. 배터리 혁신, 생산 능력, 그리고 자동차 전기화를 위한 노력에 대한 지속적인 투자를 통해 향후 수년간 전 세계 시장의 성장이 더욱 가속화될 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 3억 4,670만 달러 |

| 예측 시장 규모 | 164억 달러 |

| CAGR | 46.1% |

황화물계 고체 전해질 부문은 2025년에 43.5%의 시장 점유율을 차지하며, 2026-2035년 연평균 성장률(CAGR) 47.2%를 기록할 것으로 전망됩니다. 황화물계 전해질 재료는 액체 전해질의 성능 특성과 매우 유사한 뛰어난 이온 전도성을 지니고 있으며, 계속해서 큰 상업적 관심을 받고 있습니다. 이러한 소재들은 급속 충전 기능을 지원하며 에너지 저장 효율 향상에 기여하므로 차세대 전기자동차 배터리 시스템에 매우 적합합니다. 그러나 이 부문은 여전히 습기에 대한 민감성과 관련된 제조상 과제에 직면해 있으며, 이로 인해 대규모 배터리 제조 공정에서 생산의 복잡성과 전반적인 가공 비용이 증가하고 있습니다.

파우치형 부문은 2025년에 46.7%의 시장 점유율을 차지하며, 2035년까지 연평균 성장률(CAGR) 47.5%로 성장할 것으로 전망됩니다. 파우치형 배터리는 경량 구조와 유연한 패키지 설계 덕분에 에너지 효율을 높이고 전기자동차에 배터리를 최적화하여 통합할 수 있게 해주기 때문에 널리 선호되고 있습니다. 이 배터리들은 높은 에너지 밀도를 제공하며, 소형이고 효율적인 배터리 솔루션을 추구하는 자동차 제조사들에게 보다 정교한 맞춤 설계를 가능하게 합니다. 이러한 장점에도 불구하고 파우치형 배터리는 팽창 문제와 구조적 내구성의 한계로 인해 여전히 취약한 점이 있으며, 시장에서 사업을 운영하는 제조사들에게 설계 및 성능 측면에서의 과제로 남아 있습니다.

미국의 전기자동차용 차세대 전고체 배터리 시장은 2025년에 5,900만 달러에 달하며, 2026-2035년 연평균 성장률(CAGR) 45.9%로 성장할 것으로 전망됩니다. 벤처 캐피털, 기술 개발 기업, 자동차 제조업체의 투자가 증가함에 따라 미국은 첨단 배터리 기술의 주요 혁신 허브로 계속해서 부상하고 있습니다. 배터리 연구개발 및 상용화 활동에 대한 재정 지원 확대는 제품 개발 일정을 앞당기고, 국내 제조 역량을 강화하고 있습니다. 또한 기업이 장기적인 배터리 공급망을 확보하고 전기자동차 생산 목표를 가속화하려는 가운데, 배터리 개발 기업과 자동차 제조사 간의 전략적 제휴도 점점 더 보편화되고 있습니다. 또한 자동차 제조사들은 급속히 발전하는 전고체 배터리 업계에서 경쟁력을 강화하기 위해 사내 연구 프로그램 및 공동 개발 계약에 대한 투자를 확대하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 전해질별, 2022-2035년

제6장 시장 추산·예측 : 배터리 형태별, 2022-2035년

제7장 시장 추산·예측 : 용량 범위별, 2022-2035년

제8장 시장 추산·예측 : 차량별, 2022-2035년

제9장 시장 추산·예측 : 지역별, 2022-2035년

제10장 기업 개요

KSA 26.06.23The Global EV Next-Generation Solid-State Battery Market was valued at USD 346.7 million in 2025 and is estimated to grow at a CAGR of 46.1% to reach USD 16.4 billion by 2035.

The EV next-generation solid-state battery industry is gaining significant traction as the automotive sector accelerates its transition toward advanced electric mobility solutions. Rising demand for electric vehicles continues to encourage battery manufacturers and automotive companies to invest heavily in next-generation battery technologies capable of delivering improved efficiency and enhanced driving performance. Solid-state batteries are attracting strong attention because they offer higher energy density, enabling electric vehicles to achieve extended driving ranges while maintaining compact battery sizes. Increasing consumer expectations for shorter charging times are also contributing to rapid technological progress across the market. Advanced battery architectures support improved ion conductivity and greater power output, helping reduce charging durations and improve overall vehicle convenience. Safety remains another major growth factor supporting adoption within the EV next-generation solid-state battery market. Compared to conventional battery technologies, solid-state systems provide enhanced thermal stability and lower safety risks, making them increasingly attractive for electric vehicle applications. Ongoing investments in battery innovation, manufacturing capabilities, and automotive electrification initiatives are expected to further strengthen market expansion globally over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $346.7 Million |

| Forecast Value | $16.4 Billion |

| CAGR | 46.1% |

The sulfide-based solid electrolytes segment held a 43.5% share in 2025 and is anticipated to register a CAGR of 47.2% from 2026 to 2035. Sulfide-based electrolyte materials continue to gain strong commercial interest due to their superior ionic conductivity, which closely matches the performance characteristics of liquid electrolytes. These materials support faster charging capabilities and contribute to higher energy storage efficiency, making them highly suitable for next-generation electric vehicle battery systems. However, the segment continues to face manufacturing challenges associated with moisture sensitivity, which increases production complexity and overall processing costs within large-scale battery manufacturing operations.

The pouch segment accounted for 46.7% share in 2025 and is forecast to grow at a CAGR of 47.5% through 2035. Pouch cell batteries are widely preferred due to their lightweight structure and flexible packaging design, which support improved energy efficiency and optimized battery integration within electric vehicles. These batteries offer high energy density and allow greater customization for vehicle manufacturers seeking compact and efficient battery solutions. Despite these advantages, pouch cells remain vulnerable to swelling issues and limited structural durability, which continue to present engineering and performance challenges for manufacturers operating in the market.

U.S. EV Next-Generation Solid-State Battery Market reached USD 59 million in 2025 and is expected to grow at a CAGR of 45.9% between 2026 and 2035. The United States continues to emerge as a major innovation hub for advanced battery technologies due to increasing investments from venture capital firms, technology developers, and automotive manufacturers. Growing financial support for battery research and commercialization activities is accelerating product development timelines and strengthening domestic manufacturing capabilities. Strategic collaborations between battery developers and automakers are also becoming increasingly common as companies seek to secure long-term battery supply chains and accelerate electric vehicle production goals. In addition, automotive manufacturers are expanding investments in internal research programs and collaborative development agreements to strengthen their competitive position within the rapidly evolving solid-state battery industry.

Key companies operating in the EV Next-Generation Solid-State Battery Market include BYD, CATL, LG Energy Solution, Nissan, Panasonic Energy, ProLogium Technology, QuantumScape, Samsung SDI, SK On, Solid Power, Toyota Motor, and WeLion. Companies participating in the EV next-generation solid-state battery market are adopting multiple strategic initiatives to strengthen their market presence and technological leadership. Major industry participants are increasing investments in research and development activities focused on improving energy density, battery safety, charging speed, and manufacturing scalability. Strategic partnerships between automotive manufacturers and battery developers are becoming increasingly important for securing long-term supply agreements and accelerating commercialization efforts. Many companies are also expanding pilot production facilities and investing in advanced manufacturing infrastructure to support large-scale deployment of solid-state battery technologies. In addition, businesses are pursuing intellectual property development and patent expansion to strengthen competitive advantages within the evolving market landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Electrolyte

- 2.2.3 Battery form

- 2.2.4 Capacity range

- 2.2.5 Vehicle

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 EV range extension demand

- 3.2.1.2 Fast-charging requirement

- 3.2.1.3 Automotive safety improvement push

- 3.2.1.4 Government EV electrification mandates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing cost

- 3.2.2.2 Scalability challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Premium EV segment expansion

- 3.2.3.2 Commercial fleet electrification

- 3.2.3.3 Strategic OEM-battery partnerships

- 3.2.3.4 Energy density breakthrough innovations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 U.S. Department of Energy (DOE)

- 3.6.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.6.2 Europe

- 3.6.2.1 European Commission Directorate-General for Mobility and Transport (DG MOVE)

- 3.6.2.2 European Chemicals Agency (ECHA)

- 3.6.3 Asia Pacific

- 3.6.3.1 Ministry of Industry and Information Technology (MIIT)

- 3.6.3.2 Ministry of Heavy Industries (MHI)

- 3.6.4 Latin America

- 3.6.4.1 Ministry of Development, Industry, Trade and Services (MDIC)

- 3.6.4.2 Secretariat of Economy (SE)

- 3.6.5 Middle East & Africa

- 3.6.5.1 Ministry of Industry and Advanced Technology (MoIAT)

- 3.6.5.2 Ministry of Industry and Mineral Resources

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Trade Data Analysis (Driven by Primary Research)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Installed Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 Gen AI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Electrolyte, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Oxide-based solid electrolytes

- 5.3 Polymer-based solid electrolytes

- 5.4 Sulfide-based solid electrolytes

- 5.5 Composite/hybrid electrolytes

Chapter 6 Market Estimates & Forecast, By Battery Form, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Pouch

- 6.3 Prismatic

- 6.4 Cylindrical

Chapter 7 Market Estimates & Forecast, By Capacity Range, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Small Pack (Below 50 Ah)

- 7.3 Mid-Range Pack (50-150 Ah)

- 7.4 Large Pack (Above 150 Ah)

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Sedan

- 8.2.2 SUV

- 8.2.3 Hatchback

- 8.3 Commercial Vehicles

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Thailand

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 BMW

- 10.1.2 BYD

- 10.1.3 CATL (Contemporary Amperex Technology)

- 10.1.4 LG Energy Solution

- 10.1.5 Panasonic Energy

- 10.1.6 Samsung SDI

- 10.1.7 Toyota Motor

- 10.1.8 Volkswagen

- 10.2 Regional players

- 10.2.1 Automotive Cells Company (ACC)

- 10.2.2 General Motors (GM)

- 10.2.3 Hyundai Motor

- 10.2.4 Nissan Motor

- 10.2.5 SK Innovation / SK On

- 10.2.6 Stellantis

- 10.2.7 SVOLT Energy Technology

- 10.3 Emerging players

- 10.3.1 Factorial Energy

- 10.3.2 ProLogium Technology

- 10.3.3 QuantumScape

- 10.3.4 Solid Power

- 10.3.5 WeLion