|

시장보고서

상품코드

2061297

위성 메가 콘스텔레이션 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2026-2035년)Satellite Mega-Constellation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

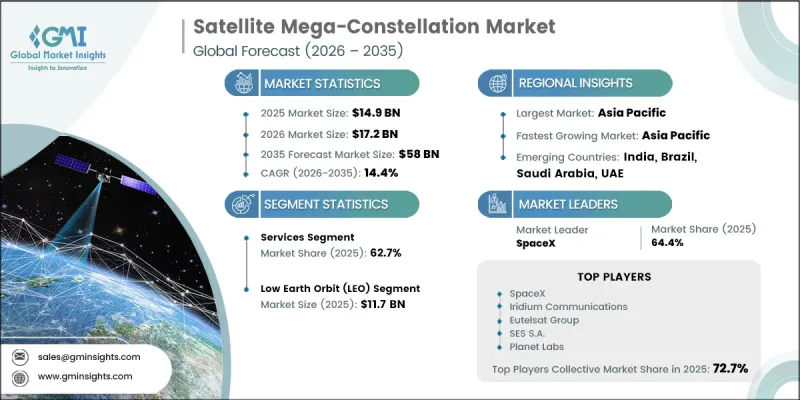

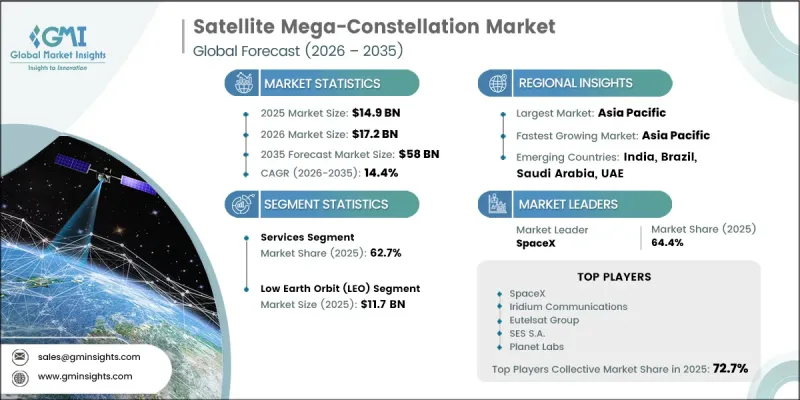

세계의 위성 메가 콘스텔레이션 시장은 2025년에 149억 달러로 평가되었으며, CAGR 14.4%로 성장하여 2035년까지 580억 달러에 달할 것으로 추정됩니다.

위성 메가 콘스텔레이션 산업 전반의 성장은 끊이지 않는 전 세계 광대역 접속 수요의 증가, 우주 인프라에 대한 자본 유입 확대, 그리고 위성 통신 및 데이터 전송 서비스의 확대에 힘입어 견인되고 있습니다. 발사 기술과 위성 제조 공정의 지속적인 개선을 통해 운영 비용이 절감되고, 대규모 위성 군의 배치 주기가 단축되고 있습니다. 또한, 저지연 통신 네트워크에 대한 수요 역시 전 세계 첨단 위성 시스템의 확장을 가속화하고 있습니다. 통신, 운송, 항공, 해운, 디지털 서비스 등 다양한 산업 분야에서 위성을 활용한 연결이 점차 확산되고 있어, 시장은 강력한 성장세를 보이고 있습니다. 지구 관측, 원격 감지, 실시간 분석, IoT(사물인터넷) 연결, 기기와의 직접 통신 등 용도의 확대가 시장 수요를 더욱 부추기고 있습니다. 또한, 2022년 이후 소프트웨어 정의형 위성 아키텍처의 통합을 통해 궤도 상에서의 변경, 적응형 네트워크 관리 및 임무 효율성 향상이 가능해지면서 운영상의 유연성이 획기적으로 개선되었습니다. 이러한 발전은 커버리지 능력, 통신 신뢰성 및 네트워크 성능을 지속적으로 향상시키고 있으며, 전 세계 위성 메가 콘스텔레이션 시장에 유리한 성장 기회를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 149억 달러 |

| 예측액 | 580억 달러 |

| CAGR | 14.4% |

우주 부문은 위성 발사의 급속한 진전과 위성군 확장 이니셔티브에 대한 투자 확대에 힘입어 2035년까지 연평균 성장률(CAGR) 16.2%를 기록할 것으로 예상됩니다. 제조 능력 향상과 발사 효율 개선은 궤도상 자산의 신속한 배치를 뒷받침하며, 위성 메가 콘스텔레이션 업계의 전체 네트워크 인프라 구축을 강화하고 있습니다.

2025년 기준으로 저궤도(LEO) 부문의 시장 규모는 117억 달러를 기록했습니다. LEO 시스템의 도입이 확대되고 있는 배경에는 저지연 통신, 고속 데이터 전송, 그리고 광범위한 지역 및 전 세계에 걸친 커버리지를 제공할 수 있는 능력이 있습니다. 대규모 위성군 배치 및 실시간 연결 애플리케이션에 대한 적합성이 여러 최종사용자 부문에서 상업적 수요를 지속적으로 견인하고 있습니다.

2025년, 북미의 위성 메가 콘스텔레이션 시장은 41.1%의 점유율을 차지했습니다. 지역 시장의 성장은 확고히 자리 잡은 민간 우주 기업의 존재, 선진적인 항공우주 인프라, 그리고 고도로 발달한 상업 우주 생태계에 의해 뒷받침되고 있습니다. 대규모 위성 네트워크의 지속적인 구축과 발사 활동의 증가는 해당 지역 전체의 기술 발전과 시장 확대에 기여하고 있습니다. 위성 광대역 서비스의 조기 상용화에 더해, 정부 및 기업 부문의 수요 증가가 북미 위성 메가 콘스텔레이션 산업의 전망을 더욱 견고하게 만들고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 구성요소별, 2022-2035년

제6장 시장 추정 및 예측 : 용도별, 2022-2035년

제7장 시장 추정 및 예측 : 궤도 유형별, 2022-2035년

제8장 시장 추정 및 예측 : 콘스텔레이션 규모별, 2022-2035년

제9장 시장 추정 및 예측 : 최종사용자별, 2022-2035년

제10장 시장 추정 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

KSM 26.06.22The Global Satellite Mega-Constellation Market was valued at USD 14.9 billion in 2025 and is estimated to grow at a CAGR of 14.4% to reach USD 58 billion by 2035.

Growth across the satellite mega-constellation industry is fueled by the increasing requirement for uninterrupted global broadband access, rising capital inflow into space-based infrastructure, and the growing deployment of satellite communication and data transmission services. Continuous improvements in launch technologies and satellite production processes are reducing operational costs and enabling faster deployment cycles for large-scale constellations. Demand for low-latency communication networks is also accelerating the expansion of advanced satellite systems worldwide. The market is witnessing strong momentum from the increasing adoption of satellite-enabled connectivity across industries, including telecommunications, transportation, aviation, maritime, and digital services. Expanding applications in Earth monitoring, remote sensing, real-time analytics, Internet of Things connectivity, and direct-to-device communication are further strengthening market demand. In addition, the integration of software-defined satellite architectures since 2022 has transformed operational flexibility by enabling in-orbit modifications, adaptive network management, and enhanced mission efficiency. These developments continue to improve coverage capabilities, communication reliability, and network performance, creating favorable growth opportunities for the global satellite mega-constellation market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.9 Billion |

| Forecast Value | $58 Billion |

| CAGR | 14.4% |

The space segment is expected to record a CAGR of 16.2% throughout 2035, owing to the rapid pace of satellite launches and increasing investments in constellation expansion initiatives. Enhanced manufacturing capabilities and greater launch efficiency are supporting the faster deployment of orbital assets and reinforcing overall network infrastructure development within the satellite mega-constellation industry.

The low Earth orbit (LEO) segment accounted for USD 11.7 billion in 2025. Strong adoption of LEO systems is attributed to their ability to deliver low-latency communication, high-speed data transfer, and extensive regional and global coverage. Their suitability for large constellation deployments and real-time connectivity applications continues to drive commercial demand across multiple end-use sectors.

North America Satellite Mega-Constellation Market captured 41.1% share in 2025. Regional market growth is supported by the presence of established private space enterprises, advanced aerospace infrastructure, and a highly developed commercial space ecosystem. Ongoing deployment of large-scale satellite networks and increasing launch activities are contributing to technological progress and market expansion across the region. Early commercialization of satellite broadband services, combined with rising demand from government and enterprise sectors, is further strengthening the North America satellite mega-constellation industry outlook.

Key companies operating in the Global Satellite Mega-Constellation Market include SpaceX, Eutelsat Group, Amazon, Telesat, Iridium Communications, China Aerospace Science & Technology Corporation, Shanghai Spacecom Satellite Technology, SES S.A., Sateliot, AST SpaceMobile, Lynk Global, Planet Labs, Spire Global, Satellogic, and E-Space. Leading participants in the satellite mega-constellation market are focusing on strategic partnerships, advanced satellite manufacturing, and aggressive constellation deployment programs to strengthen their market position. Companies are increasing investments in reusable launch technologies, software-defined satellite systems, and next-generation communication platforms to improve operational efficiency and reduce deployment costs. Many industry players are also expanding their global coverage capabilities through collaborations with telecom providers, government agencies, and technology firms. Continuous investment in research and development is enabling the introduction of low-latency connectivity solutions, enhanced Earth observation services, and direct-to-device communication technologies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Application trends

- 2.2.3 Orbit Type trends

- 2.2.4 Constellation Size trends

- 2.2.5 End- User trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for global broadband connectivity

- 3.2.1.2 Rising defense and military investments in space based communication networks

- 3.2.1.3 Advancements in reusable launch vehicles and satellite manufacturing technologies

- 3.2.1.4 Growing demand for real time earth observation and data analytics

- 3.2.1.5 Increasing deployment of IoT and direct-to-device satellite connectivity services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital requirements and long return cycles

- 3.2.2.2 Space debris and regulatory challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of in-orbit data processing and edge computing capabilities

- 3.2.3.2 Emergence of satellite-as-a-service business models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Discrete satellite mega-constellation devices

- 5.3 Space segment

- 5.3.1 Satellite buses

- 5.3.2 Payloads

- 5.3.3 Propulsion systems

- 5.3.4 Others

- 5.4 Ground segment

- 5.4.1 Stations and facilities

- 5.4.2 Network operations centers

- 5.4.3 User terminals & ground equipment

- 5.4.4 Others

- 5.5 Launch & deployment services

- 5.5.1 Dedicated launch services

- 5.5.2 Rideshare launch services

- 5.5.3 On-orbit deployment & commissioning

- 5.6 Services

- 5.6.1 Maintenance & lifecycle management

- 5.6.2 Network control & orchestration platforms

- 5.6.3 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Broadband connectivity

- 6.2.1 Residential internet services

- 6.2.2 Enterprise & corporate connectivity

- 6.2.3 Others

- 6.3 Earth observation & remote sensing

- 6.3.1 Environmental monitoring

- 6.3.2 Agricultural intelligence

- 6.3.3 Maritime & vessel tracking

- 6.3.4 Climate & weather analysis

- 6.3.5 Others

- 6.4 Defense & surveillance

- 6.4.1 Military communications

- 6.4.2 Intelligence, surveillance & reconnaissance (ISR)

- 6.4.3 Others

- 6.5 Navigation & positioning

- 6.6 Media & broadcasting

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Orbit Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Low earth orbit (LEO)

- 7.3 Medium earth orbit (MEO)

- 7.4 Geostationary earth orbit (GEO)

Chapter 8 Market Estimates and Forecast, By Constellation Size, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Small (100-500 satellites)

- 8.3 Medium (501-1,000 satellites)

- 8.4 Large (1,001-3,000 satellites)

- 8.5 Very Large (Above 3,000 satellites)

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Commercial operators

- 9.2.1 Telecommunications service providers

- 9.2.2 Satellite network operators

- 9.2.3 Internet service providers

- 9.2.4 Others

- 9.3 Government & defense

- 9.3.1 Military & defense agencies

- 9.3.2 National security organizations

- 9.3.3 Others

- 9.4 Research & space organizations

- 9.4.1 Space agencies

- 9.4.2 Academic & research institutions

- 9.4.3 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 SpaceX

- 11.1.2 Iridium Communications

- 11.1.3 Eutelsat Group

- 11.1.4 SES S.A.

- 11.1.5 Planet Labs

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Amazon

- 11.2.1.2 Telesat

- 11.2.1.3 AST SpaceMobile

- 11.2.1.4 Lynk Global

- 11.2.1.5 Spire Global

- 11.2.2 Asia Pacific

- 11.2.2.1 China Aerospace Science & Technology Corporation

- 11.2.2.2 Shanghai Spacecom Satellite Technology

- 11.2.3 Europe

- 11.2.3.1 Sateliot

- 11.2.3.2 E-Space

- 11.2.4 Middle East & Africa

- 11.2.4.1 Satellogic

- 11.2.1 North America