|

시장보고서

상품코드

2061304

고전압 스위치 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2026-2035년)High Voltage Switches Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

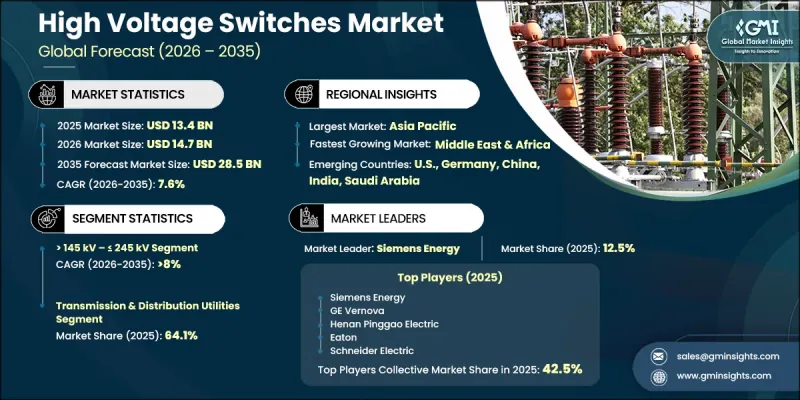

세계의 고전압 스위치 시장은 2025년에 134억 달러로 평가되었으며, CAGR 7.6%로 성장하여 2035년까지 285억 달러에 달할 것으로 추정됩니다.

이 시장의 성장은 송배전 인프라에 대한 급속한 투자, 재생에너지 통합의 가속화, 그리고 전 세계적으로 노후화된 전력망의 현대화 진전에 힘입어 이끌리고 있습니다. 산업 시설, 데이터센터, 교통 인프라, 도시 개발 프로젝트에서 전력 수요가 증가함에 따라, 전력 회사와 정부는 고전압 송전망의 확장은 물론, 송전망의 신뢰성, 운영상의 안전성, 그리고 무정전 전력 공급을 보장할 수 있는 첨단 스위칭 솔루션의 도입을 추진하고 있습니다. 고전압 스위치는 안정적인 전력 흐름을 유지하고, 고장 부위를 격리할 수 있게 하며, 현대의 변전소 및 송전 회랑 전체에서 이루어지는 유지보수 활동을 뒷받침하는 데 있어 그 중요성이 날로 커지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 134억 달러 |

| 예측액 | 285억 달러 |

| CAGR | 7.6% |

태양광발전소, 풍력발전소, 대규모 수력발전 시설 등 재생에너지 프로젝트의 도입이 확대됨에 따라, 첨단 고전압 개폐 장치에 대한 수요가 더욱 크게 증가하고 있습니다. 재생에너지 발전은 전력 계통에 변동을 초래하기 때문에 전력 회사는 변동하는 부하에 대응하고, 전압의 안정성을 유지하며, 원활한 계통연계를 지원할 수 있는 신뢰성이 높은 개폐 장치를 도입해야 합니다. 선진국 및 신흥 경제국의 정부는 에너지 안보 강화와 송전 효율 향상을 도모하기 위해 장거리 송전 회랑, 계통연계 프로젝트 및 스마트 그리드 기술에 막대한 투자를 하고 있습니다. 이러한 투자를 통해 유틸리티 규모의 인프라 프로젝트에서 고전압 차단 스위치 및 회로 전환 장치의 도입이 크게 가속화되고 있습니다. 또한, 안전 규제 및 환경 기준, 전력 계통의 내장애성에 관한 요건이 강화됨에 따라, 전력 회사들은 노후화된 전력 인프라를 디지털화되어 유지보수 부담이 적은 스위칭 시스템으로 교체하도록 권장받고 있습니다.

145 kV 초과-245 kV 이하 부문은 2025년에 30%의 점유율을 차지했으며, 송전망에 대한 투자 확대, 진행 중인 산업 전기화, 그리고 대규모 송전망 현대화 이니셔티브에 힘입어 2035년까지 연평균 성장률(CAGR) 8%로 성장할 것으로 전망됩니다. 이러한 시스템은 송전·배전 네트워크뿐만 아니라 산업용 및 상업용 분야에서도 널리 활용되고 있으며, 신뢰성 높은 전력 흐름을 뒷받침하고, 송전망의 안정성을 높이며, 효율적인 고장 보호 및 운영 성능을 확보하기 위해 활용되고 있습니다.

최종사용자별로는 2025년에 송배전 사업자 부문이 64.1%의 점유율을 차지했습니다. 이 부문의 경쟁력은 주로 송전망 확장, 노후화된 인프라의 교체, 그리고 도시 지역 및 산업 부문의 전력 소비량 증가에 따른 대규모 투자에서 비롯됩니다. 전력 사업자들은 신뢰성 향상, 전력 손실 저감, 그리고 재생에너지원을 국가 송전망에 통합하기 위해 기존 변전소 및 송전망의 현대화를 적극적으로 추진하고 있습니다. 스마트 그리드 기술, 첨단 감시 시스템 및 자동화 변전소의 도입 확대는 고성능 스위칭 장비에 대한 수요를 더욱 부추기고 있습니다. 고전압 스위치는 전력망 내에서의 안전한 격리, 고장 차단 및 운영상의 유연성을 실현하는 데 있어 매우 중요한 역할을 수행하고 있으며, 현대 송전 인프라에 없어서는 안 될 구성요소로 자리 잡고 있습니다. 증가하는 산업 부하, 데이터센터 확장 및 전기화 이니셔티브를 뒷받침할 수 있는 탄력적인 전력망에 대한 관심이 높아짐에 따라, 예측 기간 동안 송배전 사업자들의 견조한 수요가 지속될 것으로 예상됩니다.

아시아태평양의 고전압 개폐 장치 시장은 2025년까지 연평균 성장률(CAGR) 9%로 성장할 것으로 예상됩니다. 이 지역의 주도적 지위는 중국, 인도, 일본, 한국, 호주 등 여러 국가에서 이루어지고 있는 급속한 산업화, 대규모 도시화, 전력 수요 증가, 그리고 송전 인프라에 대한 지속적인 투자에 힘입어 유지되고 있습니다. 이 지역의 각국 정부는 에너지 안보 강화와 송전 효율 향상을 도모하기 위해 재생에너지 통합, 초고전압 송전 회랑, 그리고 기존 송전망의 현대화에 막대한 투자를 하고 있습니다. 중국은 송전 인프라의 적극적인 확충, 재생에너지의 광범위한 도입, 그리고 고전압 전기 장비의 견고한 국내 제조 생태계를 바탕으로 계속해서 지역 내 수요를 주도하고 있습니다. 인도 역시 산업 발전, 전기화 프로그램, 철도 확장 프로젝트, 그리고 스마트 그리드 인프라에 대한 투자의 뒷받침을 받아 상당한 성장을 이루고 있습니다. 아시아태평양 전체에서 데이터센터, 상업 인프라 및 산업 단지의 도입이 확대됨에 따라, 신뢰성이 높은 고전압 개폐 솔루션에 대한 수요가 더욱 가속화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 제품별, 2022-2035년

제6장 시장 규모 및 예측 : 등급별, 2022-2035년

제7장 시장 규모 및 예측 : 최종사용자별, 2022-2035년

제8장 시장 규모 및 예측 : 채널별, 2022-2035년

제9장 시장 규모 및 예측 : 전송 방식별, 2022-2035년

제10장 시장 규모 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

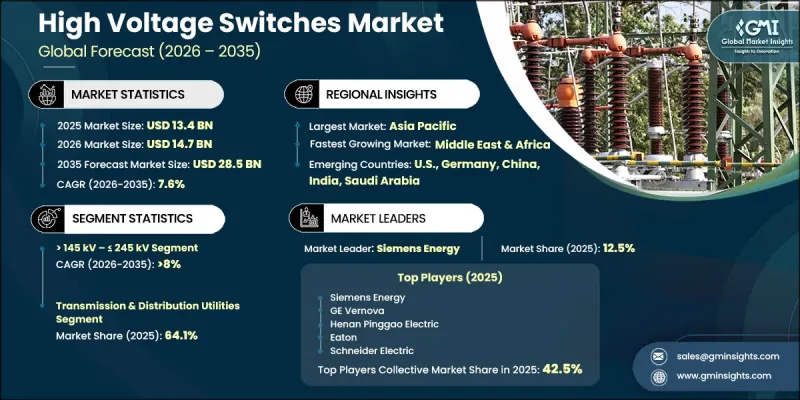

KSM 26.06.22The Global High Voltage Switches Market was valued at USD 13.4 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 28.5 billion by 2035.

The market growth is driven by rapid investments in transmission and distribution infrastructure, accelerating renewable energy integration, and increasing modernization of aging power grids worldwide. Rising electricity demand from industrial facilities, data centers, transportation infrastructure, and urban development projects is encouraging utilities and governments to expand high-voltage transmission networks and deploy advanced switching solutions capable of ensuring grid reliability, operational safety, and uninterrupted power supply. High voltage switches are becoming increasingly critical for maintaining stable power flow, enabling fault isolation, and supporting maintenance activities across modern substations and transmission corridors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.4 Billion |

| Forecast Value | $28.5 Billion |

| CAGR | 7.6% |

The increasing adoption of renewable energy projects, including solar farms, wind parks, and large-scale hydroelectric facilities, is further creating substantial demand for advanced high-voltage switching equipment. Renewable energy generation introduces variability into power systems, requiring utilities to deploy highly reliable switching devices capable of handling fluctuating loads, maintaining voltage stability, and supporting seamless grid synchronization. Governments across developed and emerging economies are investing heavily in long-distance transmission corridors, grid interconnection projects, and smart grid technologies to strengthen energy security and improve transmission efficiency. These investments are significantly accelerating the deployment of high-voltage disconnect switches and circuit switchers across utility-scale infrastructure projects. In addition, stricter safety regulations, environmental standards, and grid resilience requirements are encouraging utilities to replace aging electrical infrastructure with digitally enabled and low-maintenance switching systems.

The >145 kV to <= 245 kV segment accounted for 30% share in 2025 and is anticipated to register growth at an 8% CAGR through 2035, driven by rising investments in power transmission networks, ongoing industrial electrification, and large-scale grid modernization initiatives. These systems are extensively utilized across power transmission and distribution networks, as well as in industrial and commercial applications, to support reliable electricity flow, enhance grid stability, and ensure efficient fault protection and operational performance.

By end user, the transmission & distribution utilities segment held 64.1% share in 2025. The dominance of this segment is primarily attributed to large-scale investments in grid expansion, replacement of aging infrastructure, and rising electricity consumption across urban and industrial sectors. Utilities are aggressively modernizing existing substations and transmission networks to improve reliability, reduce power losses, and support the integration of renewable energy sources into national grids. Increasing deployment of smart grid technologies, advanced monitoring systems, and automated substations is further boosting demand for high-performance switching equipment. High voltage switches play a crucial role in enabling safe isolation, fault interruption, and operational flexibility within utility networks, making them indispensable components of modern transmission infrastructure. The growing focus on resilient power networks capable of supporting rising industrial loads, data center expansion, and electrification initiatives is expected to sustain robust demand from transmission and distribution utilities over the forecast period.

Asia Pacific High Voltage Switches Market is expected to grow at a CAGR of 9% in 2025. The region's leadership is supported by rapid industrialization, large-scale urbanization, rising electricity demand, and continuous investments in transmission infrastructure across countries including China, India, Japan, South Korea, and Australia. Governments across the region are investing heavily in renewable energy integration, ultra-high-voltage transmission corridors, and modernization of existing grid networks to strengthen energy security and improve transmission efficiency. China continues to lead regional demand due to its aggressive expansion of transmission infrastructure, extensive renewable deployment, and robust domestic manufacturing ecosystem for high-voltage electrical equipment. India is also witnessing substantial growth driven by increasing industrial development, electrification programs, railway expansion projects, and investments in smart grid infrastructure. The rising deployment of data centers, commercial infrastructure, and industrial parks across Asia Pacific is further accelerating demand for reliable high-voltage switching solutions.

Key players operating in the Global High Voltage Switches Market include Siemens Energy, GE Vernova, Schneider Electric, Hitachi Energy, Mitsubishi Electric Corporation, Eaton, CG Power and Industrial Solutions, Henan Pinggao Electric Co., China XD Group, Siemens Energy, S&C Electric Company, and Southern States LLC. Companies operating in the high voltage switches market are increasingly adopting strategies focused on technological innovation, manufacturing expansion, strategic collaborations, and digital grid integration to strengthen their market foothold. Leading manufacturers are investing heavily in the development of intelligent and IoT-enabled switching solutions integrated with predictive maintenance, remote monitoring, and automation capabilities to improve grid reliability and operational efficiency. Companies are also expanding production facilities and strengthening regional supply chains to meet rising demand from utility modernization and renewable energy projects. Partnerships with utilities, EPC contractors, and grid infrastructure developers are helping manufacturers secure long-term transmission and substation projects across emerging markets. In addition, firms are focusing on environmentally sustainable solutions, including SF6-free technologies, compact modular designs, and digital substations to comply with tightening environmental regulations and evolving grid modernization requirements. Strategic acquisitions, localization initiatives, and investments in R&D are further enabling market participants to strengthen their competitive positioning and expand their global customer base.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Rating trends

- 2.1.4 End user trends

- 2.1.5 Channel trends

- 2.1.6 Transmission type trends

- 2.1.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of high voltage switches

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Growth in untapped markets & applications

- 3.10 Technical comparison of IEC v/s IEEE standards

- 3.11 Investment analysis & future prospects

- 3.12 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.12.1 By region (Driven by Primary Research)

- 3.12.2 By product (Driven by Primary Research)

- 3.12.3 By rating (Driven by Primary Research)

- 3.12.4 By end user (Driven by Primary Research)

- 3.13 Trade data analysis (Driven by Primary Research)

- 3.13.1 Import/export value trends (Driven by Primary Research)

- 3.13.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.14.1 AI-Driven production optimization (Driven by Primary Research)

- 3.14.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Disconnect switches

- 5.2.1 By Design

- 5.2.1.1 Vertical break

- 5.2.1.2 Center break

- 5.2.1.3 Double-end

- 5.2.1.4 Single-side

- 5.2.1.5 Ground

- 5.2.1.6 Hookstick-operated

- 5.2.1.7 Phase-over-phase

- 5.2.1.8 Unitized

- 5.2.1.9 Others

- 5.2.1 By Design

- 5.3 Circuit switchers

- 5.3.1 By Design

- 5.3.1.1 Capacitor

- 5.3.1.2 Reactor

- 5.3.1.3 Vertical

- 5.3.1.4 Horizontal circuit

- 5.3.1.5 Horizontal line

- 5.3.1.6 Load & line

- 5.3.1.7 Others

- 5.3.1 By Design

Chapter 6 Market Size and Forecast, By Rating, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 > 72.5 kV - ≤ 145 kV

- 6.3 > 145 kV - ≤ 245 kV

- 6.4 > 245 kV - ≤ 420 kV

- 6.5 > 420 kV

Chapter 7 Market Size and Forecast, By End User, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Transmission & distribution utilities

- 7.3 Industrial

- 7.4 Data centers

- 7.5 Commercial & infrastructure

- 7.6 Renewable energy

- 7.7 Others

Chapter 8 Market Size and Forecast, By Channel, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 EPC / turnkey procurement

- 8.4 System integrator

- 8.5 Indirect/ aftermarket

Chapter 9 Market Size and Forecast, By Transmission Type, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 HVAC

- 9.3 HVDC

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Russia

- 10.3.5 Italy

- 10.3.6 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Australia

- 10.4.3 India

- 10.4.4 Japan

- 10.4.5 South Korea

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Qatar

- 10.5.4 Oman

- 10.5.5 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

Chapter 11 Company Profiles

- 11.1 Bharat Heavy Electricals Limited

- 11.2 China XD Electric Co.

- 11.3 CNC Electric

- 11.4 CG Power and Industrial Solutions

- 11.5 CHINT Group

- 11.6 Cleaveland/Price Inc.

- 11.7 COELME

- 11.8 EMSPEC

- 11.9 Eaton

- 11.10 Elsewedy Electric

- 11.11 Eximprod

- 11.12 Fuji Electric FA Components & Systems Co.

- 11.13 GE Vernova

- 11.14 Goto Electrical Co.

- 11.15 Haivo Electrical Co.

- 11.16 Hapam

- 11.17 Henan Pinggao Electric Co.

- 11.18 Hitachi Energy

- 11.19 Hubbell

- 11.20 Insulect

- 11.21 Liyond Electric Co.

- 11.22 MindCore Technologies

- 11.23 Mitsubishi Electric Corporation

- 11.24 Ormazabal

- 11.25 Patton & Cooke Co.

- 11.26 Pinggao India

- 11.27 Schneider Electric

- 11.28 Siemens Energy

- 11.29 Socomec

- 11.30 Southern States LLC

- 11.31 S&C Electric Company

- 11.32 Toshiba Energy Systems & Solutions Corporation