|

시장보고서

상품코드

2061346

가스치환포장 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Modified Atmosphere Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

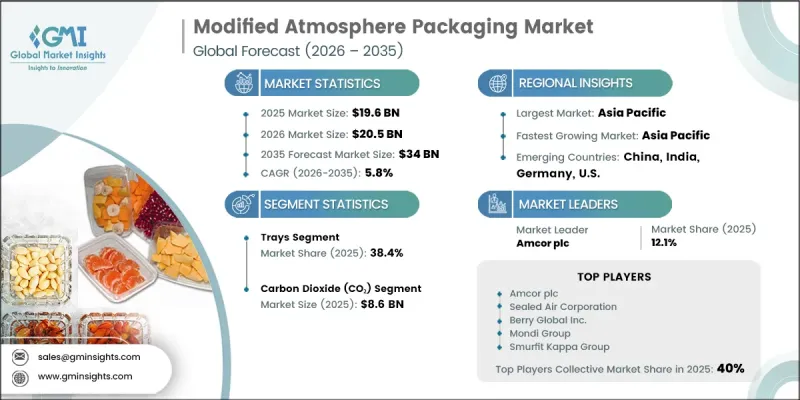

세계의 가스치환포장 시장은 2025년에 196억 달러로 평가되고 CAGR 5.8%로 성장하며, 2035년까지 340억 달러에 달할 것으로 예측됩니다.

가스치환포장 업계는 유통 기한이 길고 신선하며 고품질의 식품에 대한 소비자의 수요가 증가함에 따라 꾸준한 성장을 달성하고 있습니다. 조직화된 식품 소매업의 급속한 확대, 냉장 운송 인프라의 개선, 그리고 공급망 전반에 걸친 식품 폐기물 감축에 대한 관심 증대가 시장 발전에 크게 기여하고 있습니다. 또한 단백질이 풍부한 식품, 인스턴트 식품 및 포장된 편의식품의 소비가 확대됨에 따라 전 세계에서 첨단 포장 기술의 도입이 가속화되고 있습니다. 실링 시스템, 배리어 필름, 가스 치환 기술의 발전으로 인해 포장 효율과 제품의 보존 능력이 더욱 향상되고 있습니다. 제조업체와 식품 가공업체들은 유통 및 보관 과정 전반에 걸쳐 신선도를 유지하고, 영양가를 보존하며, 제품의 안전성을 높이기 위해 가스치환포장 솔루션에 대한 의존도를 높이고 있습니다. 또한 지속가능한 식품 보존 방법에 대한 인식이 높아지고 있으며, 소매 및 가공 환경에서 부패로 인한 손실을 최소화하면서 식품 유통 시스템을 최적화해야 할 필요성이 커지고 있는 점도 업계에 긍정적인 요인으로 작용하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035 |

| 개시 금액 | 196억 달러 |

| 예측액 | 340억 달러 |

| CAGR | 5.8% |

전 세계에서 신선식품 및 신선식품에 대한 선호도가 높아짐에 따라 여러 식품 부문에서 가스치환포장 솔루션에 대한 수요가 계속해서 증가하고 있습니다. 신선 농산물, 육류 제품, 유제품 및 조리 식품에는 운송 및 보관 중에 신선도를 유지하고 유통기한을 연장할 수 있는 첨단 포장 시스템이 요구되고 있습니다. 또한 공급망 전반에 걸친 식품 폐기물 최소화 및 식품 가공 부문의 전반적인 업무 효율 향상을 위한 노력이 활발해지고 있는 점도 시장의 성장세를 지원하고 있습니다. 차단 성능이 향상된 포장재의 지속적인 혁신을 통해, 제조업체는 제품의 품질을 더 오랫동안 유지하면서 더욱 뛰어난 제품 보호 기능을 실현할 수 있게 되었습니다. 또한 식품 보존과 폐기물 감축에 중점을 둔 지원책 덕분에 전 세계 식품 업계 전반에서 가스치환포장 기술의 도입이 촉진되고 있습니다.

2025년에는 트레이 부문이 38.4%의 점유율을 차지했습니다. 트레이는 구조적 내구성과 강력한 밀봉 성능이 필수적인 육류, 수산물, 가금류, 신선식품의 포장 용도로 여전히 널리 사용되고 있습니다. 제어된 대기 조건을 효과적으로 유지하면서도 고속 포장 작업에 대응할 수 있는 이 능력은 식품 가공 및 소매 부문 전반에 걸쳐 계속해서 강력한 수요를 이끌고 있습니다. 트레이가 제공하는 신뢰성과 보호 특성 덕분에, 장기적인 보관 안정성과 높은 수준의 제품 보호가 필요한 제품의 경우 트레이가 선호되는 포장 형태로 자리 잡고 있습니다.

이산화탄소(CO2) 부문은 포장 식품 분야에서 미생물 증식을 억제하고 신선도를 유지하는 뛰어난 효과에 힘입어, 2025년에는 86억 달러의 시장 규모를 기록했습니다. 이산화탄소는 식품의 안전성을 유지하고 유통기한을 연장하는 데 필수적인, 육류, 수산물, 가금류 및 조리식품을 위한 가스치환포장 시스템에 널리 사용되고 있습니다. 대규모 포장 식품 사업에서 이 물질이 광범위하게 사용됨에 따라 전 세계 가스치환포장 업계에서 이산화탄소의 우위성이 계속해서 유지되고 있습니다.

2025년, 북미의 가스치환포장 시장은 28%의 점유율을 차지했습니다. 해당 지역에서는 고도로 발달한 콜드체인 인프라에 힘입어, 포장된 신선식품, 간편식, 냉장식품에 대한 수요가 계속해서 견고한 양상을 보이고 있습니다. 북미 전역의 식품 가공업체와 소매업체들은 장거리 운송 및 보관 중 제품 품질 향상, 부패 방지, 신선도 유지를 위해 가스치환포장 기술에 대한 의존도를 높이고 있습니다. 또한 첨단인 식품 안전 시스템, 냉장 물류, 혁신적인 포장 기술에 대한 투자 확대도 해당 지역 전체의 시장 확대에 크게 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품 유형별, 2022-2035년

제6장 시장 추산·예측 : 포장재료별, 2022-2035년

제7장 시장 추산·예측 : 가스 유형별, 2022-2035년

제8장 시장 추산·예측 : 최종 용도별, 2022-2035년

제9장 시장 추산·예측 : 지역별, 2022-2035년

제10장 기업 개요

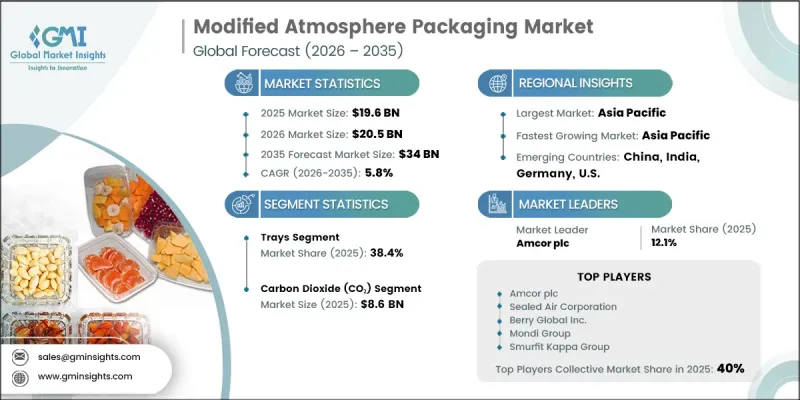

KSA 26.06.23The Global Modified Atmosphere Packaging Market was valued at USD 19.6 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 34 billion by 2035.

The modified atmosphere packaging industry is witnessing steady growth due to increasing consumer demand for fresh and high-quality food products with extended shelf life. Rapid expansion of organized food retail, improvements in refrigerated transportation infrastructure, and rising focus on reducing food waste across supply chains are significantly contributing to market development. In addition, growing consumption of protein-rich food products, ready-to-eat meals, and packaged convenience foods is accelerating the adoption of advanced packaging solutions globally. Technological advancements in sealing systems, barrier films, and gas-flushing technologies are further improving packaging efficiency and product preservation capabilities. Manufacturers and food processors are increasingly relying on modified atmosphere packaging solutions to maintain freshness, preserve nutritional quality, and improve product safety throughout distribution and storage processes. The industry is also benefiting from increasing awareness regarding sustainable food preservation practices and the need to optimize food distribution systems while minimizing spoilage losses across retail and processing environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $19.6 Billion |

| Forecast Value | $34 Billion |

| CAGR | 5.8% |

The rising global preference for fresh and perishable food products continues to strengthen demand for modified atmosphere packaging solutions across multiple food categories. Fresh produce, meat products, dairy items, and packaged meals require advanced packaging systems capable of preserving freshness and extending shelf life during transportation and storage. The market is also gaining momentum due to increasing efforts aimed at minimizing food waste across supply chains and improving overall operational efficiency within the food processing sector. Continuous innovation in packaging materials with enhanced barrier performance is enabling manufacturers to deliver better product protection while maintaining product quality for longer periods. Furthermore, supportive initiatives focused on food preservation and waste reduction are encouraging broader implementation of modified atmosphere packaging technologies across the global food industry.

The trays segment accounted for 38.4% share in 2025. Trays remain widely adopted for packaging applications involving meat, seafood, poultry, and fresh produce, where structural durability and strong sealing performance are critical. Their ability to maintain controlled atmospheric conditions effectively while supporting high-speed packaging operations continues to drive strong demand across food processing and retail sectors. The reliability and protective characteristics offered by trays make them a preferred packaging format for products requiring extended shelf stability and enhanced product protection.

The carbon dioxide (CO2) segment generated USD 8.6 billion in 2025, driven by its strong effectiveness in slowing microbial growth and preserving freshness across packaged food applications. Carbon dioxide is extensively utilized in modified atmosphere packaging systems for meat, seafood, poultry, and prepared meal products where maintaining food safety and extending shelf life are essential. Its widespread usage across large-scale packaged food operations continues to support its dominance within the global modified atmosphere packaging industry.

North America Modified Atmosphere Packaging Market held 28% share in 2025. The region continues to experience strong demand for packaged fresh foods, convenience meals, and refrigerated food products supported by a highly developed cold chain infrastructure. Food processors and retailers across North America increasingly rely on modified atmosphere packaging technologies to improve product quality, reduce spoilage, and maintain freshness during long-distance transportation and storage. Rising investment in advanced food safety systems, refrigerated logistics, and innovative packaging technologies is also contributing significantly to market expansion across the region.

Major companies operating in the Global Modified Atmosphere Packaging Market include Sealed Air Corporation, Berry Global Inc., Amcor Plc, Mondi Group, Winpak Ltd., Coveris Holdings S.A., Graphic Packaging International, MULTIVAC Group, Smurfit Kappa Group, Crown Holdings Inc., ProAmpac, StePac Inc., Dow Chemical Company, Charter NEX Films Inc., AEP Industries Inc., Klockner Pentaplast (kp), Air Products and Chemicals Inc., Linde AG, and Praxair Inc. Companies operating in the modified atmosphere packaging market are focusing on product innovation, sustainable packaging development, and strategic partnerships to strengthen their market presence and competitive positioning. Manufacturers are investing heavily in advanced barrier films, recyclable packaging materials, and improved sealing technologies to enhance product preservation while meeting evolving sustainability requirements. Businesses are also expanding production capabilities and strengthening distribution networks to address rising global demand for packaged fresh foods and convenience products. Strategic collaborations with food processors, retailers, and logistics providers are enabling companies to deliver customized packaging solutions tailored to specific food applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Packaging material trends

- 2.2.3 Gas type trends

- 2.2.4 End- use application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for fresh and minimally processed food

- 3.2.1.2 Expansion of global cold-chain logistics

- 3.2.1.3 Increasing focus on reducing food waste in supply chains

- 3.2.1.4 Growth of high-protein and convenience food categories

- 3.2.1.5 Advancements in packaging materials and sealing technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced MAP materials and equipment

- 3.2.2.2 Operational complexity and strict compliance requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Emergence of smart and IoT-enabled MAP solutions

- 3.2.3.2 Expansion into pharmaceutical and medical sterile-packaging applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Trays

- 5.3 Films

- 5.4 Bags and pouches

- 5.5 Lidding films

- 5.6 Containers

- 5.7 Flexible wraps

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Packaging Material, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Polyethylene (PE)

- 6.3 Polyethylene terephthalate (PET)

- 6.4 Ethylene vinyl alcohol (EVOH)

- 6.5 Polypropylene (PP)

- 6.6 Multi-layer barrier films

- 6.7 Biodegradable materials

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Gas Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Carbon dioxide (CO2)

- 7.3 Oxygen (O2)

- 7.4 Nitrogen (N2)

- 7.5 Mixed gases

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End- Use Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food

- 8.2.1 Meat, poultry & seafood

- 8.2.2 Fruits & vegetables

- 8.2.3 Dairy products

- 8.2.4 Bakery & confectionery

- 8.2.5 Ready meals

- 8.2.6 Others

- 8.3 Pharmaceutical & healthcare

- 8.3.1 Pharmaceuticals

- 8.3.2 Medical devices

- 8.4 Industrial

- 8.4.1 Electronics

- 8.4.2 Specialty chemicals

- 8.4.3 Others

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor plc

- 10.1.2 Sealed Air Corporation

- 10.1.3 Berry Global Inc.

- 10.1.4 Mondi Group

- 10.1.5 Smurfit Kappa Group

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Winpak Ltd.

- 10.2.1.2 Crown Holdings Inc.

- 10.2.1.3 Air Products and Chemicals Inc.

- 10.2.1.4 ProAmpac

- 10.2.1.5 AEP Industries Inc.

- 10.2.1.6 Charter NEX Films Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 StePac Inc.

- 10.2.2.2 Dow Chemical Company

- 10.2.3 Europe

- 10.2.3.1 Klockner Pentaplast (kp)

- 10.2.3.2 MULTIVAC Group

- 10.2.3.3 Coveris Holdings S.A.

- 10.2.3.4 Linde AG

- 10.2.3.5 Graphic Packaging International

- 10.2.4 Middle East & Africa

- 10.2.4.1 Praxair Inc.

- 10.2.1 North America