|

시장보고서

상품코드

2061350

인공 추간판 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2026-2035년)Artificial Disc Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

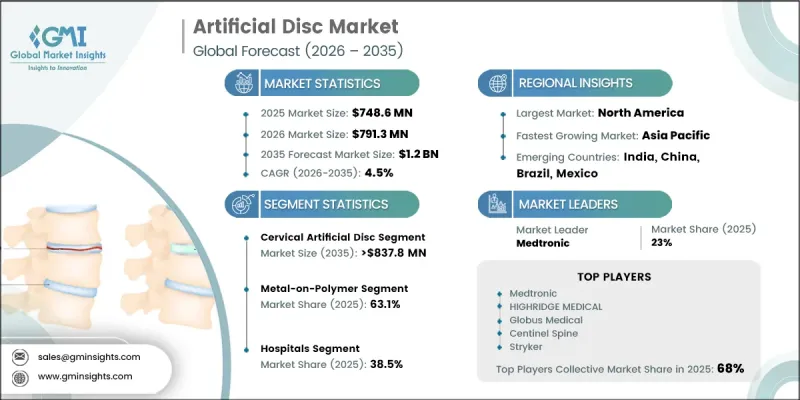

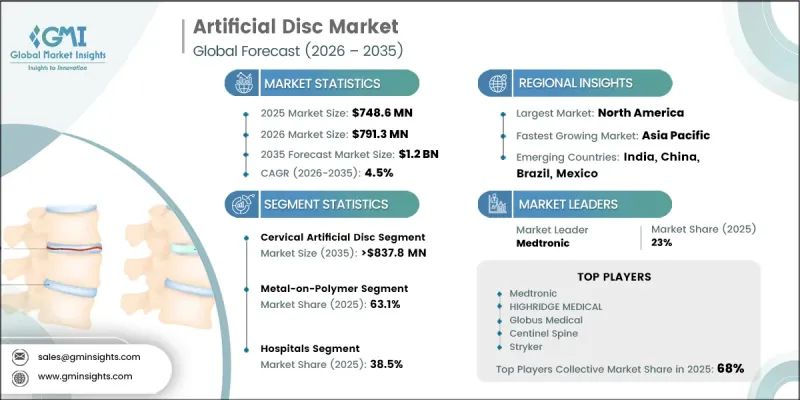

세계의 인공 추간판 시장은 2025년에 7억 4,860만 달러로 평가되었으며, CAGR 4.5%로 성장하여 2035년까지 12억 달러에 달할 것으로 추정됩니다.

시장 성장은 퇴행성 추간판 질환의 유병률 증가, 척추 임플란트 재료 및 기기 공학의 지속적인 발전, 그리고 최소침습 척추 수술에 대한 선호도 증가에 힘입어 이루어지고 있습니다. 또한, 선진적인 의료 제도 하에서 보험 적용 범위가 확대됨에 따라, 환자들이 인공 추간판 치환술을 더 쉽게 이용할 수 있게 되었습니다. 고령화, 장시간 앉아 있는 생활 습관, 비만율의 증가로 인해 척추 질환의 부담이 커지면서, 장기적인 관절 가동성을 유지하는 치료법에 대한 수요가 크게 증가하고 있습니다. 외과적 시술이 필요한 환자층의 확대는 의료 기관 전반에 걸쳐 첨단 척추 임플란트의 도입 확대를 촉진하고 있습니다. 또한, 생체 재료 및 기기 설계의 지속적인 개선을 통해 내구성, 내마모성, 생체적합성이 향상되었을 뿐만 아니라, 척추의 자연스러운 움직임을 재현하는 능력도 높아져, 그 결과 임상 성과와 외과의사의 신뢰도가 강화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 7억 4,860만 달러 |

| 예측액 | 12억 달러 |

| CAGR | 4.5% |

경추 인공 추간판 부문은 2025년에 69.5%의 시장 점유율을 차지했으며, 2035년까지 8억 3,780만 달러에 달할 것으로 전망되며, 2035년까지 연평균 성장률(CAGR) 4.7%를 기록할 것으로 추정됩니다. 이 부문은 목 부위의 퇴행성 질환 치료에 있어, 가동성을 유지하면서 인접한 척추 부문에 가해지는 부담을 줄여준다는 효과 덕분에 계속해서 주도적인 위치를 유지하고 있습니다. 양호한 임상 결과와 비교적 복잡하지 않은 수술 절차가 높이 평가되어, 외과의사들로부터 폭넓은 지지를 받고 있습니다. 현대인의 생활 습관과 관련된 경추 퇴행성 질환의 사례가 증가함에 따라, 이에 대한 수요도 더욱 늘어나고 있습니다. 주요 의료 시장에서 확고한 임상적 유효성이 입증되고 규제 당국의 승인을 받은 점도 도입률 향상에 기여하고 있습니다.

2025년 기준으로 MOP(Metal-on-polymer) 부문은 63.1%의 시장 점유율을 차지했습니다. 이 제품 카테고리는 금속 구조와 폴리머 코어를 결합함으로써 강도와 유연성을 모두 확보할 수 있기 때문에 널리 사용되고 있습니다. 이 설계는 마찰을 줄이고 기계적 성능을 향상시키면서, 척추의 자연스러운 움직임을 재현하는 데 도움이 됩니다. 폴리머 성분은 충격 흡수성과 전반적인 생체역학적 적합성을 높여, 환자의 예후 개선에 기여하고 있습니다. 또한, 다른 설계에 비해 합병증 발생률이 낮은 점도 높은 임상적 수용성과 다양한 수술 환경에서의 폭넓은 사용을 뒷받침하고 있습니다.

2025년, 북미 인공 추간판 시장은 59.5%의 점유율을 차지했습니다. 이 지역은 혁신적인 척추 수술이 널리 보급되어 있는, 고도로 발달하고 성숙한 의료 환경을 특징으로 합니다. 퇴행성 추간판 질환을 앓고 있는 환자 수가 많고, 또한 관절 가동 범위를 보존하는 치료법에 대한 인식이 높아지고 있는 점이 계속해서 수요를 견인하고 있습니다. 주요 의료기기 제조업체들의 존재와 연구 개발에 대한 지속적인 투자가 끊임없는 제품 혁신을 더욱 뒷받침하고 있습니다. 또한, 유리한 상환 제도와 첨단 척추 수술 기술에 대한 조기 규제 승인이 지역 전체의 시장 침투를 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 종류별(2022-2035년)

제6장 시장 추정 및 예측 : 재료별(2022-2035년)

제7장 시장 추정 및 예측 : 용도별(2022-2035년)

제8장 시장 추정 및 예측 : 최종 용도별(2022-2035년)

제9장 시장 추정 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KSM 26.06.22The Global Artificial Disc Market was valued at USD 748.6 million in 2025 and is estimated to grow at a CAGR of 4.5% to reach USD 1.2 billion by 2035.

Market growth is driven by the rising prevalence of degenerative disc diseases, continuous advancements in spinal implant materials and device engineering, and increasing preference for minimally invasive spine procedures. Expanding reimbursement coverage in developed healthcare systems is also supporting wider patient access to artificial disc replacement therapies. The growing burden of spinal disorders, fueled by aging populations, sedentary behavior, and increasing obesity rates, is significantly increasing demand for long-term motion-preserving treatment options. The expanding patient base requiring surgical intervention is encouraging greater adoption of advanced spinal implants across healthcare facilities. In addition, ongoing improvements in biomaterials and device design are enhancing durability, wear resistance, and biocompatibility, while also improving replication of natural spinal movement, thereby strengthening clinical outcomes and surgeon confidence.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $748.6 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 4.5% |

The cervical artificial disc segment held a 69.5% share in 2025 and is estimated to reach USD 837.8 million by 2035, growing at a CAGR of 4.7% during 2035. This segment continues to lead due to its effectiveness in treating degenerative conditions in the neck region while maintaining motion and reducing stress on adjacent spinal segments. It is widely preferred by surgeons because of its favorable clinical results and comparatively less complex surgical procedures. Rising cases of cervical spine degeneration linked to modern lifestyle patterns are further supporting demand. Strong clinical validation and regulatory approvals in major healthcare markets have also contributed to increasing adoption rates.

The metal-on-polymer segment held a 63.1% share in 2025. This product category is widely used due to its ability to combine strength and flexibility through a metallic structure paired with a polymer core. This design helps replicate natural spinal motion while reducing friction and improving mechanical performance. The polymer component enhances shock absorption and overall biomechanical compatibility, which contributes to improved patient outcomes. Its lower complication profile compared to alternative designs has also supported strong clinical acceptance and widespread usage across surgical settings.

North America Artificial Disc Market held a 59.5% share in 2025. The region represents a highly advanced and mature healthcare environment with strong adoption of innovative spinal procedures. A large patient population affected by degenerative disc conditions, along with increasing awareness of motion-preserving treatment alternatives, continues to drive demand. The presence of leading medical device manufacturers and sustained investment in research and development further support ongoing product innovation. In addition, favorable reimbursement frameworks and early regulatory approvals for advanced spinal technologies are accelerating market penetration across the region.

Key companies operating in the Global Artificial Disc Industry include Globus Medical, Medtronic, Stryker, Orthofix, Spineart, Centinel Spine, Spineway Group, AxioMed, HIGHRIDGE MEDICAL, Neuro France Implants, and SIGNUS Medizintechnik. Companies in the artificial disc market are focusing on continuous product innovation through the development of next-generation motion-preserving spinal implants with improved durability and biocompatibility. Many players are investing heavily in research and clinical trials to strengthen product efficacy and expand surgical indications. Strategic collaborations with hospitals, orthopedic specialists, and research institutions help accelerate product adoption and clinical validation. Firms are also expanding their geographic presence in emerging healthcare markets to tap into rising surgical demand. Advances in biomaterials, including improved polymer and metal combinations, are being prioritized to enhance implant performance. In addition, companies are strengthening surgeon training programs to improve procedural outcomes and adoption rates.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Material trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of degenerative disc diseases

- 3.2.1.2 Rising preference for minimally invasive spine surgeries

- 3.2.1.3 Technological advancements in artificial disc materials and designs

- 3.2.1.4 Expansion of reimbursement coverage in developed regions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of artificial disc replacement procedures

- 3.2.2.2 Stringent regulatory approvals for medical devices

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing research and development in biomaterials and implants

- 3.2.3.2 Development of next-generation motion-preserving devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by primary research)

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing trend analysis (Driven by primary research)

- 3.10 Impact of AI & generative AI on the market

- 3.11 Investment & funding analysis

- 3.12 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Cervical artificial disc

- 5.3 Lumbar artificial disc

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Metal-on-metal

- 6.3 Metal-on-polymer

- 6.4 Other material types

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Spinal trauma

- 7.3 Degenerative spine disease

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinic

- 8.4 Ambulatory surgical centers

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AxioMed

- 10.2 Centinel Spine

- 10.3 Globus Medical

- 10.4 HIGHRIDGE MEDICAL

- 10.5 Medtronic

- 10.6 Neuro France Implants

- 10.7 Orthofix

- 10.8 SIGNUS Medizintechnik

- 10.9 Spineart

- 10.10 Spineway Group

- 10.11 Stryker