|

시장보고서

상품코드

2061353

유동성 지혈제 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Flowable Hemostats Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

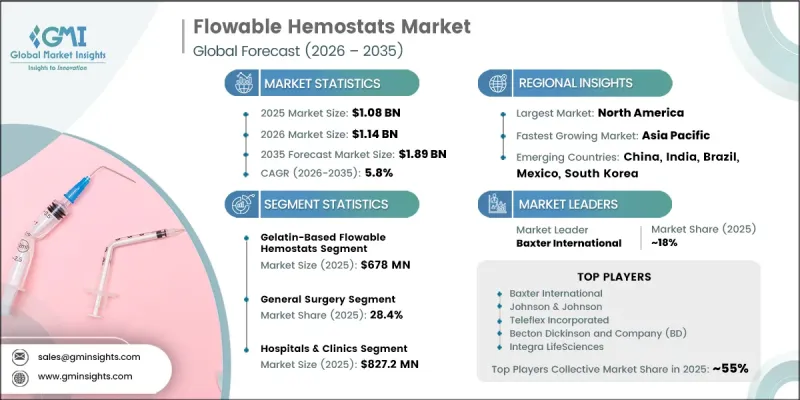

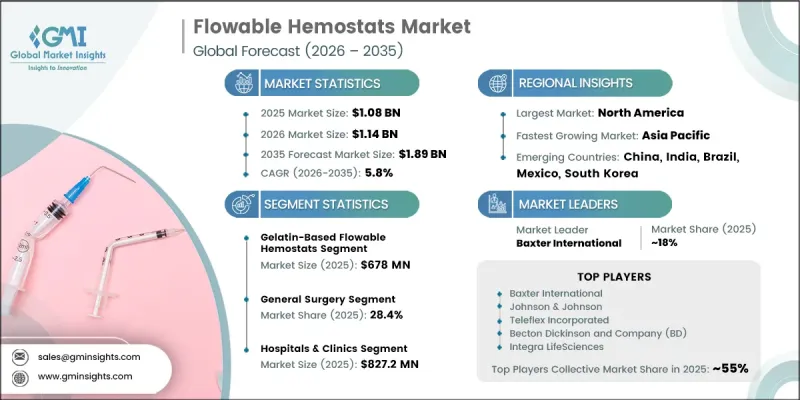

세계의 유동성 지혈제 시장은 2025년에 10억 8,000만 달러로 평가되고 CAGR 5.8%로 성장하며, 2035년까지 18억 9,000만 달러에 달할 것으로 추정되고 있습니다.

전 세계에서 시행되는 외과수술 건수가 증가하는 데다, 수술 중 효과적인 지혈 관리가 필요한 외상 및 만성질환의 유병률이 높아짐에 따라 해당 시장은 인상적인 성장을 달성하고 있습니다. 유동성 지혈제는 기존 방법으로는 충분한 효과를 얻을 수 없는 상황에서 출혈을 제어하기 위해 특별히 고안되었으므로 현대 외과 의료에서 중요한 요소로 자리 잡고 있습니다. 이러한 제품들은 신속한 응고 성능, 사용 편의성, 그리고 복잡한 수술 환경에 대한 적응력 덕분에 여러 외과 전문 분야에서 점점 더 널리 사용되고 있습니다. 저침습 수술에 대한 수요가 증가하는 것도 시장 확대에 더욱 기여하고 있습니다. 외과 의사들은 정확성, 효율성, 그리고 환자 예후 개선을 지원하는 첨단 지혈 솔루션에 대한 필요성이 점점 더 커지고 있기 때문입니다. 또한 의료진은 수술 전후 기간의 혈액 관리와 수술의 안전성을 더욱 중시하게 되었으며, 이는 전 세계 병원 및 전문 의료 시설에서 유동성 지혈 제품의 도입을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 10억 8,000만 달러 |

| 예측액 | 18억 9,000만 달러 |

| CAGR | 5.8% |

또한 전 세계적인 고령화에 따른 수술 건수의 증가와 응급 입원율의 상승도 시장을 지원하고 있습니다. 고급 수술용 지혈 솔루션에 대한 인식이 높아지고, 최소 침습 수술이 보급되면서 업계의 성장을 더욱 지원하고 있습니다. COVID-19 팬데믹으로 인한 혼란이 가라앉은 후, 병원과 의료 시스템에서는 연기되었던 수술과 예정된 수술이 대거 재개되면서 유동성 지혈제에 대한 수요가 크게 증가했습니다. 주요 생명공학 기업 및 의료기기 제조업체들의 제품 개발, 규제 당국의 승인 획득, 그리고 지역 시장 진출을 위한 지속적인 투자 역시 시장 발전에 기여하고 있습니다. 각 제조사는 다양한 의료 전문 분야에 걸쳐 활동하는 외과의사 및 의료진의 변화하는 요구에 부응하기 위해 제품의 성능 향상, 사용 편의성 및 임상적 적합성 향상에 점점 더 주력하고 있습니다.

젤라틴 기반 유동성 지혈제 부문은 2025년에 6억 7,800만 달러의 시장 규모를 기록했습니다. 이 범주에는 돼지나 소에서 유래한 제품이 포함되어 있으며, 입증된 임상적 효능과 폭넓은 외과적 적용 가능성 덕분에 계속해서 견고한 시장 수요를 유지하고 있습니다. 젤라틴 기반의 유동성 지혈제는 특히 수술이 어려운 부위나 불규칙한 상처 표면에서도 신속하고 확실한 지혈이 가능하므로 의료 현장에서 널리 선호되고 있습니다. 다양한 외과수술에서 그 적용 가능성과 유효성이 인정받고 있으며, 병원 및 수술 센터에서의 보급이 계속해서 확대되고 있습니다.

병원·진료소 부문은 2025년에 8억 2,720만 달러를 차지할 것으로 예상되며, 2035년까지 연평균 성장률(CAGR) 5.7%로 성장할 것으로 전망됩니다. 병원과 진료소는 일상적인 수술부터 복잡한 수술에 이르기까지 다양한 수술을 다수 시행하고 있으므로 유동성 지혈제의 주요 최종 사용 시설로 자리매김하고 있습니다. 만성질환 발생률의 증가와 전 세계에서 외과적 시술에 대한 수요가 높아지는 추세가 맞물리면서, 의료 기관에서 첨단 지혈 솔루션의 도입이 촉진되고 있습니다. 수술 결과 개선, 출혈량 감소, 환자 회복 촉진에 대한 관심이 높아짐에 따라 병원 및 임상 환경 전반에서 유동성 지혈제에 대한 수요가 크게 증가하고 있습니다.

2025년, 북미의 유동성 지혈제 시장은 40.4%의 점유율을 차지했습니다. 이 지역은 연간 시행되는 수술 건수가 많고, 첨단인 수술 기술을 적극적으로 도입하며, 의료 시스템 전반에 걸친 효과적인 수술 전후 혈액 관리 전략에 대한 관심이 높아짐에 따라 계속해서 선도적인 위치를 유지하고 있습니다. 미국은 첨단인 의료 인프라, 증가하는 수술 건수, 그리고 의료 시설 전반에 걸친 혁신적인 지혈 제품의 활용 확대에 힘입어 지역 성장의 주요 견인차 역할을 계속하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품 유형별, 2022-2035년

제6장 시장 추산·예측 : 용도별, 2022-2035년

제7장 시장 추산·예측 : 최종 사용별, 2022-2035년

제8장 시장 추산·예측 : 지역별, 2022-2035년

제9장 기업 개요

KSA 26.06.23The Global Flowable Hemostats Market was valued at USD 1.08 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 1.89 billion by 2035.

The market is experiencing notable growth due to the rising number of surgical procedures being performed worldwide, along with the increasing prevalence of trauma injuries and chronic health conditions that require effective bleeding management during surgeries. Flowable hemostats have become an important component in modern surgical practices because they are specifically designed to control bleeding in situations where traditional methods may not provide sufficient results. These products are increasingly utilized across multiple surgical specialties due to their fast clotting performance, ease of application, and ability to adapt to complex surgical environments. Growing demand for minimally invasive surgical procedures is further contributing to market expansion, as surgeons increasingly require advanced hemostatic solutions that support precision, efficiency, and improved patient outcomes. In addition, healthcare providers are placing greater emphasis on perioperative blood management and surgical safety, which continues to strengthen adoption of flowable hemostatic products across hospitals and specialty care facilities globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.08 Billion |

| Forecast Value | $1.89 Billion |

| CAGR | 5.8% |

The market is also benefiting from the growing surgical burden associated with aging populations and increasing rates of emergency hospital admissions worldwide. Rising awareness regarding advanced surgical bleeding control solutions and the expanding use of minimally invasive procedures are further supporting industry growth. Following the disruption caused by the COVID-19 pandemic, hospitals and healthcare systems resumed a large volume of delayed and elective surgical procedures, which significantly accelerated demand for flowable hemostats. Continuous investments in product development, regulatory approvals, and geographic expansion initiatives by leading biotechnology and medical device companies are also contributing to market advancement. Manufacturers are increasingly focusing on improving product performance, ease of use, and clinical compatibility to address the evolving needs of surgeons and healthcare providers across diverse medical specialties.

The gelatin-based flowable hemostats segment generated USD 678 million in 2025. This category includes products derived from porcine and bovine sources and continues to maintain strong market demand because of its proven clinical effectiveness and broad surgical applicability. Gelatin-based flowable hemostats are widely preferred in healthcare settings due to their ability to provide fast and dependable bleeding control, especially in challenging surgical areas and irregular wound surfaces. Their adaptability and effectiveness across various surgical procedures continue to support widespread adoption in hospitals and surgical centers.

The hospitals and clinics segment accounted for USD 827.2 million in 2025 and is projected to grow at a CAGR of 5.7% throughout 2035. Hospitals and clinics remain the primary end-use settings for flowable hemostats because these facilities perform a high volume of both routine and complex surgical procedures. The increasing incidence of chronic diseases, combined with rising global demand for surgical interventions, is driving the adoption of advanced hemostatic solutions within healthcare institutions. Growing emphasis on improving surgical outcomes, reducing blood loss, and enhancing patient recovery is also contributing to strong demand for flowable hemostats across hospitals and clinical environments.

North America Flowable Hemostats Market held a 40.4% in 2025. The region continues to maintain a leading position due to the high number of surgical procedures performed annually, strong adoption of advanced surgical technologies, and increasing focus on effective perioperative blood management strategies across healthcare systems. The United States remains a major contributor to regional growth, supported by advanced healthcare infrastructure, growing surgical volumes, and increasing utilization of innovative hemostatic products across medical facilities.

Major companies operating in the Global Flowable Hemostats Market include Baxter International, Ethicon (Johnson & Johnson), Teleflex Incorporated, Integra LifeSciences Holdings Corporation, Pfizer, Becton Dickinson and Company (BD), Medcura, Aegis Lifesciences, Ferrosan Medical Devices, Dalim Tissen, and 3-D Matrix. Companies in the flowable hemostats market are focusing on product innovation, strategic partnerships, and geographic expansion to strengthen their competitive position. Leading manufacturers are investing heavily in research and development to introduce advanced hemostatic products with improved clotting efficiency, enhanced biocompatibility, and broader surgical applications. Many players are expanding their global footprint through collaborations with hospitals, healthcare providers, and distribution networks to improve product accessibility across emerging and developed markets. Regulatory approvals and clinical validation studies remain key priorities for companies aiming to strengthen physician confidence and increase product adoption. Businesses are also emphasizing minimally invasive surgical applications and customized hemostatic solutions to meet evolving healthcare requirements. In addition, mergers, acquisitions, and investments in manufacturing capabilities are helping companies improve supply chain efficiency and reinforce their long-term market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing number of surgical procedures globally

- 3.2.1.2 Increasing incidence of accidents and trauma cases

- 3.2.1.3 Rising technological advancements in hemostasis products

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of products

- 3.2.2.2 Availability of alternatives

- 3.2.2.3 Stringent storage & handling requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into price-sensitive emerging markets with local manufacturing

- 3.2.3.2 Development of room-temperature stable synthetic alternatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by Primary Research)

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Investment & funding analysis

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy, by product type

- 3.10 Future market trends (Driven by primary research)

- 3.11 Impact of AI & Generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Gelatin-based flowable hemostats

- 5.2.1 Porcine gelatin

- 5.2.2 Bovine gelatin

- 5.3 Collagen-based flowable hemostats

- 5.4 Synthetic polymer-based flowable hemostats

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Cardiovascular surgery

- 6.4 Orthopedic and trauma surgery

- 6.5 Gynecological surgery

- 6.6 Neurosurgery

- 6.7 Plastic and reconstructive surgery

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals & clinics

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Aegis Lifesciences

- 9.2 Baxter International

- 9.3 Becton Dickinson and Company (BD)

- 9.4 Dalim Tissen

- 9.5 Ethicon (Johnson & Johnson)

- 9.6 Ferrosan Medical Devices

- 9.7 Integra LifeSciences Holdings Corporation

- 9.8 Medcura

- 9.9 Pfizer

- 9.10 Teleflex Incorporated

- 9.11 3-D Matrix