|

시장보고서

상품코드

2061398

종양학용 AI 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)AI in Oncology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

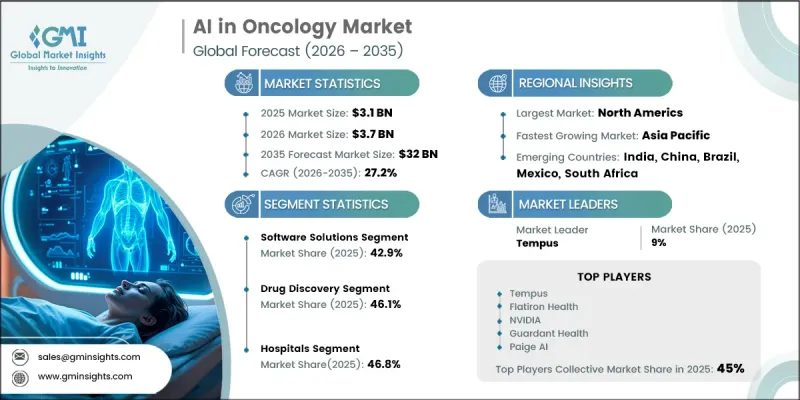

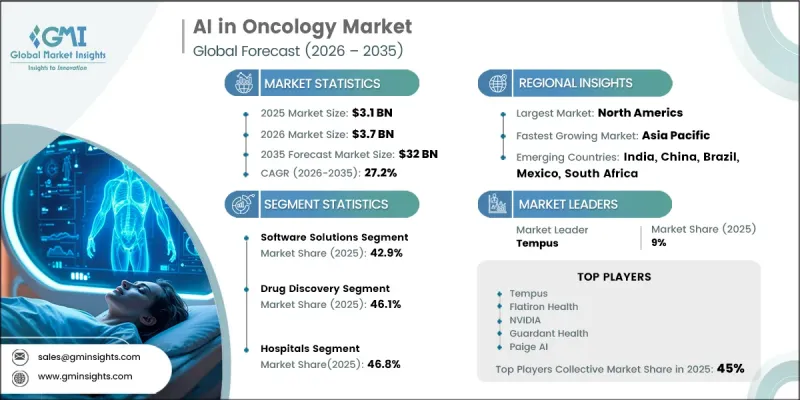

세계의 종양학용 AI 시장은 2025년에 31억 달러로 평가되며, 2035년까지 CAGR 27.2%로 성장하며, 320억 달러에 달할 것으로 추정되고 있습니다.

전 세계 암 부담의 증가, 조기 발견에 대한 수요의 증가, 그리고 정밀의학으로의 전환이 가속화됨에 따라 이 시장은 급속히 확대되고 있습니다. 종양학에서 인공지능이란 암의 검출, 진단, 치료 계획 및 신약 개발 과정을 지원하기 위해 기계 학습, 데이터 분석 및 첨단 계산 모델을 적용하는 것을 의미합니다. 고령화, 생활습관병과 관련된 위험 요인, 환경 노출로 인한 암 사례의 복잡화와 증가는 기존의 진단·치료 시스템에 막대한 부담을 주고 있습니다. AI를 활용한 기술은 진단 정확도 향상, 검사 결과 회신 시간 단축, 임상적 의사결정 강화 등을 통해 이러한 과제 해결에 기여하고 있습니다. 조기 암 검진에 대한 관심이 높아지고 있는 점도 시장 확대에 크게 기여하고 있습니다. 조기 개입은 생존율 향상, 치료비 절감, 그리고 환자 관리 개선으로 직결되기 때문입니다. 또한 디지털 헬스케어 인프라에 대한 투자 확대와 의료 기관에서의 데이터베이스 종양학 솔루션 도입 증가가 전 세계 시장의 성장을 더욱 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 31억 달러 |

| 예측액 | 320억 달러 |

| CAGR | 27.2% |

2025년에는 소프트웨어 솔루션 부문이 42.9%의 점유율을 차지했습니다. 이 부문은 종양학 업무 흐름에서 첨단 분석 플랫폼 및 임상의사결정지원시스템에 대한 의존도가 높아지고 있는 만큼, 계속해서 주도적인 위치를 유지하고 있습니다. 이러한 소프트웨어 솔루션은 방대한 양의 임상 기록, 영상 데이터세트, 유전체 정보를 효율적으로 처리할 수 있게 하여, 정확한 진단, 치료 최적화 및 예후 예측을 지원합니다. 기존의 헬스케어 IT 생태계와 통합이 가능하면서도 확장성과 상호운용성을 겸비하고 있으며, 병원, 연구 기관, 진단 검사실 등에서 널리 도입되고 있습니다. 맞춤형 의료와 근거 기반 치료 계획으로의 전환이 진행되고 있는 점도, AI를 활용한 종양학용 소프트웨어 솔루션에 대한 수요를 더욱 부추기고 있습니다.

신약 개발 부문은 2025년에 46.1%의 점유율을 차지했습니다. 이 부문의 성장은 주로 암 치료제 개발을 가속화하고, 치료법 혁신에 이르기까지의 기간을 단축해야 할 필요성이 커짐에 따라 주도되고 있습니다. AI 기술은 화합물 스크리닝의 효율화, 치료 표적의 규명, 그리고 보다 정밀한 약물 반응 예측에 널리 활용되고 있습니다. 이러한 기능 덕분에 기존의 신약 개발 과정에 소요되는 시간과 비용이 대폭 절감될 뿐만 아니라, 종양학 연구에서 임상적 성공 가능성도 높아집니다.

2025년, 미국의 AI 종양학 시장 규모는 12억 달러로 평가되었습니다. 해당 국가의 시장 성장은 암 발병률의 증가와 첨단 진단 및 선별 검사 솔루션에 대한 수요 증가에 힘입고 있습니다. 조기 발견 및 치료의 정확도를 높이기 위해, AI를 활용한 영상 진단 툴와 예측 분석의 도입이 의료 시스템 전반에서 가속화되고 있습니다. 견고한 디지털 헬스케어 인프라, 높은 기술 보급률, 그리고 확립된 임상 연구 역량이 AI 기술을 종양학 치료 경로에 통합하는 데 더욱 박차를 가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 컴포넌트별, 2022-2035년

제6장 시장 추산·예측 : 암 유형별, 2022-2035년

제7장 시장 추산·예측 : 용도별, 2022-2035년

제8장 시장 추산·예측 : 최종 용도별, 2022-2035년

제9장 시장 추산·예측 : 지역별, 2022-2035년

제10장 기업 개요

KSAThe Global AI In Oncology Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 27.2% to reach USD 32 billion by 2035.

The market is experiencing rapid expansion due to the rising global burden of cancer, increasing demand for early-stage detection, and the accelerating shift toward precision medicine approaches. Artificial intelligence in oncology refers to the application of machine learning, data analytics, and advanced computational models to support cancer detection, diagnosis, treatment planning, and drug development processes. The growing complexity and volume of oncology cases, driven by aging populations, lifestyle-related risks, and environmental exposures, is placing significant pressure on traditional diagnostic and treatment systems. AI-enabled technologies help address these challenges by improving diagnostic accuracy, reducing turnaround times, and enhancing clinical decision-making. Increasing emphasis on early cancer detection is also contributing strongly to market expansion, as early intervention is directly linked to improved survival outcomes, lower treatment costs, and better patient management. In addition, expanding investments in digital healthcare infrastructure and rising adoption of data-driven oncology solutions across healthcare institutions are further accelerating market growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $32 Billion |

| CAGR | 27.2% |

The software solutions segment accounted for 42.9% share in 2025. This segment continues to dominate due to the increasing dependence on advanced analytics platforms and clinical decision-support systems in oncology workflows. These software solutions enable efficient processing of large volumes of clinical records, imaging datasets, and genomic information, supporting accurate diagnosis, treatment optimization, and outcome prediction. Their ability to integrate with existing healthcare IT ecosystems while offering scalability and interoperability is driving widespread adoption across hospitals, research organizations, and diagnostic laboratories. The increasing shift toward personalized medicine and evidence-based treatment planning is further reinforcing demand for AI-driven oncology software solutions.

The drug discovery segment held a 46.1% share in 2025. Growth in this segment is primarily driven by the rising need to accelerate cancer drug development and improve therapeutic innovation timelines. AI technologies are being widely utilized to streamline compound screening, identify therapeutic targets, and predict drug responses with higher precision. These capabilities significantly reduce the time and cost associated with traditional drug development processes while improving the probability of clinical success in oncology research.

U.S. AI in Oncology Market was valued at USD 1.2 billion in 2025. Market growth in the country is supported by the rising incidence of cancer and the increasing demand for advanced diagnostic and screening solutions. The adoption of AI-powered imaging tools and predictive analytics is accelerating across healthcare systems to improve early detection and treatment accuracy. Strong digital healthcare infrastructure, high technology penetration, and established clinical research capabilities are further supporting the integration of AI technologies into oncology care pathways.

Key companies operating in the AI in Oncology Market include Aidoc, Freenome, Flatiron Health, GE HealthCare, Guardant Health, Ibex Medical Analytics, Lunit, Merative, NVIDIA, Paige AI, PathAI, Qure.ai, Siemens Healthineers, SOPHiA GENETICS, and Tempus. Companies operating in the AI in oncology market are adopting a range of strategic initiatives to strengthen their market position and expand clinical adoption. Leading players are heavily investing in advanced machine learning models, multimodal data integration, and next-generation diagnostic algorithms to improve cancer detection accuracy and treatment personalization. Strategic collaborations with hospitals, research institutions, and pharmaceutical companies are enabling broader clinical validation and faster commercialization of AI-based oncology solutions. Organizations are also focusing on expanding cloud-based platforms and interoperable software systems to ensure seamless integration into existing healthcare infrastructures. In addition, companies are strengthening their presence through regulatory approvals, clinical trials, and real-world evidence generation to enhance trust and adoption among healthcare providers.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy and data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy and data integrity commitment

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Cancer type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.2.5 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for early detection and classification of cancer

- 3.2.1.2 Increasing prevalence of cancer

- 3.2.1.3 Growing adoption of precision medicine

- 3.2.1.4 Surging advancements in healthcare infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High procurement and implementation cost

- 3.2.2.2 High impact of regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into rare cancers and pediatric oncology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.1.1 AI-powered medical imaging & diagnostics

- 3.5.1.2 Genomics & precision oncology analytics

- 3.5.2 Emerging technologies

- 3.5.2.1 Multimodal ai (integrated data platforms)

- 3.5.2.2 Real-world evidence & predictive oncology

- 3.5.1 Current technological trends

- 3.6 Future market trends (Driven by primary research)

- 3.7 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.8 Pricing trend analysis (Driven by primary research)

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Software solutions

- 5.3 Hardware

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Cancer Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Breast cancer

- 6.3 Lung cancer

- 6.4 Prostate cancer

- 6.5 Colorectal cancer

- 6.6 Brain tumor

- 6.7 Other cancer types

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Cancer detection and diagnosis

- 7.3 Treatment planning and optimization

- 7.4 Drug discovery

- 7.5 Drug development and clinical trials

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostics centers

- 8.4 Specialty clinics

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aidoc

- 10.2 Freenome

- 10.3 Flatiron Health

- 10.4 GE HealthCare

- 10.5 Guardant Health

- 10.6 Ibex Medical Analytics

- 10.7 Lunit

- 10.8 Merative

- 10.9 NVIDIA

- 10.10 Paige AI

- 10.11 PathAI

- 10.12 Qure.ai

- 10.13 Siemens Healthineers

- 10.14 SOPHiA GENETICS

- 10.15 Tempus