|

시장보고서

상품코드

2061401

자기열개질 블루 수소 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Autothermal Reforming Blue Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

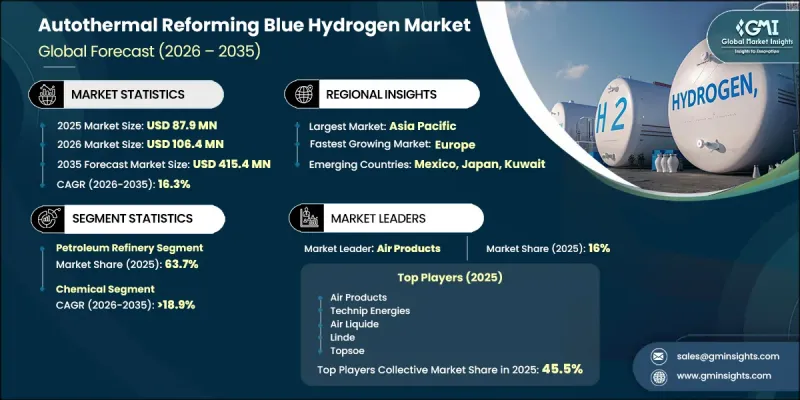

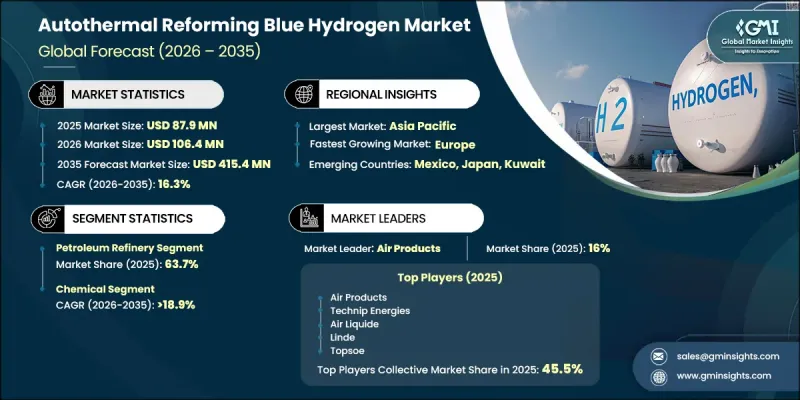

세계의 자기열개질 블루 수소 시장은 2025년에 8,790만 달러로 평가되며, 2035년까지 CAGR 16.3%로 성장하며, 4억 1,540만 달러에 달할 것으로 추정되고 있습니다.

탄소 포집 효율이 높은 저탄소 수소 제조 기술에 대한 관심이 높아지면서, 전 세계에서 자가열 개질(ATR) 공정의 도입이 크게 촉진되고 있습니다. 산업계에서는 엄격한 환경 규제, 정부의 기후 정책 및 전 세계적인 탄소 감축 목표를 준수하기 위해 보다 친환경적인 수소 생산 방식으로의 전환이 진행되고 있습니다. 에너지 집약적 부문 전반에 걸쳐 비용 대비 효과가 높은 대규모 수소 생산에 대한 수요가 증가함에 따라 시장 확대가 가속화되고 있습니다. ATR 기반의 블루 수소 시스템을 기존 산업 인프라에 통합함으로써 운영상의 유연성이 향상될 뿐만 아니라, 도입 비용이 절감되고 전환 과정 중의 혼란도 최소화되고 있습니다. ATR 기술은 탄소 포집 기능을 갖춘 기존 수소 생산 시설의 개조를 가능하게 하고, 프로젝트의 경제성을 높이며, 도입 기간을 단축하므로 기업의 도입이 점점 더 확대되고 있습니다. ATR 시스템이 천연가스, 바이오가스 및 더 무거운 가스를 포함한 여러 원료를 처리할 수 있는 능력은 다양한 산업 분야에서 그 매력을 한층 더 높여주고 있습니다. 또한 산업의 탈탄소화와 청정 에너지로의 전환 전략에 대한 관심이 높아짐에 따라 전 세계 자가열개질(ATR) 블루 수소 시장에는 강력한 장기 성장 기회가 창출될 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 8,790만 달러 |

| 예측액 | 4억 1,540만 달러 |

| CAGR | 16.3% |

정유소용 애플리케이션 부문은 2025년에 63.7%의 시장 점유율을 차지하며, 2035년까지 연평균 성장률(CAGR) 14.2%로 성장할 것으로 전망됩니다. 수소를 많이 사용하는 공정에서 발생하는 배출량을 줄여야 한다는 정유소에 대한 압박이 커짐에 따라 저탄소 수소 제조 기술의 도입이 촉진되고 있습니다. ATR(암모니아 개질) 기반의 블루 수소 시스템은 대규모 수소 공급 능력을 갖추고 있으면서도 탄소 포집 솔루션을 효율적으로 통합할 수 있다는 점에서 주목을 받고 있습니다. 정유소 운영사들은 진화하는 환경 기준을 준수하면서 신뢰성이 높고 비용 효율적인 가동을 확보하기 위해, 기존의 그레이 수소 설비를 ATR 기반 시스템으로 교체하는 움직임을 강화하고 있습니다. 지속적인 연료 처리 및 지속가능성 향상에 대한 수요가 이 부문의 성장을 더욱 촉진하고 있습니다.

미국의 자가열개질(ATR) 블루 수소 시장은 2025년에 85.6%의 점유율을 차지하며, 2035년까지 6,400만 달러 규모의 시장에 도달할 것으로 전망됩니다. 철강, 화학, 시멘트 등 산업 전반에 걸쳐 탈탄소화 노력이 확대됨에 따라 해당 국가에서는 저배출 수소 생산 기술에 대한 수요가 크게 증가하고 있습니다. 청정 연료 도입 촉진을 목적으로 한 연방 정부의 지원 프로그램, 탄소 감축 인센티브, 그리고 우호적인 규제 정책이 시장 성장에 긍정적인 영향을 미치고 있습니다. 탄소 포집·활용·저장(CCUS) 프로젝트를 장려하는 금융 메커니즘은 ATR(자동 열분해) 기반의 블루 수소 인프라에 대한 투자를 가속화하고 있습니다. 또한 수소 개발 프로젝트에 대한 민관 자금 지원이 증가함에 따라 미국내 첨단 수소 제조 기술의 상용화와 규모 확대가 촉진되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모·예측 : 용도별, 2022-2035년

제6장 시장 규모·예측 : 지역별, 2022-2035년

제7장 기업 개요

KSA 26.06.24The Global Autothermal Reforming Blue Hydrogen Market was valued at USD 87.9 million in 2025 and is estimated to grow at a CAGR of 16.3% to reach USD 415.4 million by 2035.

Rising focus on low-carbon hydrogen production technologies with high carbon capture efficiency is significantly supporting the adoption of autothermal reforming (ATR) processes worldwide. Industries are increasingly shifting toward cleaner hydrogen production methods to comply with stringent environmental regulations, government climate policies, and global carbon reduction targets. Growing demand for cost-effective large-scale hydrogen generation across energy-intensive sectors is also accelerating market expansion. The integration of ATR-based blue hydrogen systems into existing industrial infrastructure is improving operational flexibility while lowering deployment costs and minimizing disruptions during transition processes. Companies are increasingly adopting ATR technology because it enables retrofitting of conventional hydrogen production facilities with carbon capture capabilities, improving project economics and reducing implementation timelines. The ability of ATR systems to process multiple feedstocks, including natural gas, biogas, and heavier gases, is further increasing their attractiveness across different industrial applications. In addition, the growing emphasis on industrial decarbonization and clean energy transition strategies is expected to create strong long-term growth opportunities for the autothermal reforming blue hydrogen market globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $87.9 Million |

| Forecast Value | $415.4 Million |

| CAGR | 16.3% |

The petroleum refinery application segment accounted for 63.7% share in 2025 and is anticipated to grow at a CAGR of 14.2% through 2035. Rising pressure on refineries to lower emissions associated with hydrogen-intensive processes is encouraging the adoption of low-carbon hydrogen production technologies. ATR-based blue hydrogen systems are gaining traction due to their ability to deliver large-scale hydrogen output while integrating carbon capture solutions efficiently. Refinery operators are increasingly replacing conventional grey hydrogen facilities with ATR-based systems to comply with evolving environmental standards while ensuring reliable and cost-efficient operations. The need for continuous fuel processing and improved sustainability performance is further supporting segment growth.

U.S. Autothermal Reforming Blue Hydrogen Market accounted for 85.6% share in 2025 and is projected to generate USD 64 million by 2035. Growing decarbonization initiatives across industries such as steel, chemicals, and cement are creating significant demand for low-emission hydrogen production technologies in the country. Federal support programs, carbon reduction incentives, and favorable regulatory policies aimed at promoting clean fuel adoption are positively influencing market growth. Financial mechanisms encouraging carbon capture, utilization, and storage projects are accelerating investments in ATR-based blue hydrogen infrastructure. In addition, increasing public and private sector funding for hydrogen development projects is supporting the commercialization and scale-up of advanced hydrogen production technologies across the U.S.

Leading companies operating in the Global Autothermal Reforming Blue Hydrogen Market include Air Liquide, Air Products, Casale, CF Industries, Clariant AG, Equinor, ExxonMobil, Ineos, INPEX, Johnson Matthey, KBR, Linde, Petronas, SABIC, Saudi Aramco, Shell, Sinopec, Technip Energies, Topsoe, and TotalEnergies. Companies active in the autothermal reforming blue hydrogen market are implementing several growth strategies to strengthen their market presence and expand operational capabilities. Major participants are investing heavily in carbon capture technologies, process optimization, and large-scale hydrogen production facilities to improve efficiency and reduce operational costs. Strategic collaborations with industrial manufacturers, energy providers, and infrastructure developers are helping companies accelerate project deployment and secure long-term supply agreements. Businesses are also focusing on expanding global production networks and increasing investments in hydrogen transportation and storage infrastructure to support large-scale commercialization. In addition, companies are prioritizing technology innovation to improve feedstock flexibility, enhance carbon capture rates, and meet evolving environmental standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Application trends

- 2.4 Region trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.2.1 North America

- 3.2.2 Europe

- 3.2.3 Asia Pacific

- 3.2.4 Middle East & Africa

- 3.2.5 Latin America

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of ATR blue hydrogen

- 3.8 Price trend analysis (Driven by Primary Research)

- 3.8.1 By application USD/Ton (Driven by Primary Research)

- 3.8.2 Pricing strategy by player type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 Predictive maintenance & fault detection

- 3.9.2 Grid optimization & load forecasting

- 3.9.3 Digital twin simulation & testing

- 3.9.4 Risks, limitations & regulatory considerations

- 3.10 Emerging opportunities & trends

- 3.10.1 Digitalization & IoT integration

- 3.10.2 Emerging market penetration

- 3.11 Overall investment scenario and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MT)

- 5.1 Key trends

- 5.2 Petroleum refinery

- 5.3 Chemical

- 5.4 Steel & metals

- 5.5 Power generation

- 5.6 Transportation

- 5.7 Others

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MT)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 France

- 6.3.3 UK

- 6.3.4 Italy

- 6.3.5 Netherlands

- 6.3.6 Russia

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 Oman

- 6.5.3 UAE

- 6.5.4 Kuwait

- 6.5.5 Qatar

- 6.5.6 South Africa

- 6.6 Latin America

Chapter 7 Company Profiles

- 7.1 Air Liquide

- 7.2 Air Products

- 7.3 Casale

- 7.4 CF Industries

- 7.5 Clariant AG

- 7.6 Equinor

- 7.7 ExxonMobil

- 7.8 Ineos

- 7.9 INPEX

- 7.10 Johnson Matthey

- 7.11 KBR

- 7.12 Linde

- 7.13 Petronas

- 7.14 SABIC

- 7.15 Saudi Aramco

- 7.16 Shell

- 7.17 Sinopec

- 7.18 Technip Energies

- 7.19 Topsoe

- 7.20 TotalEnergies