|

시장보고서

상품코드

2061422

유전체학 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Genomics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

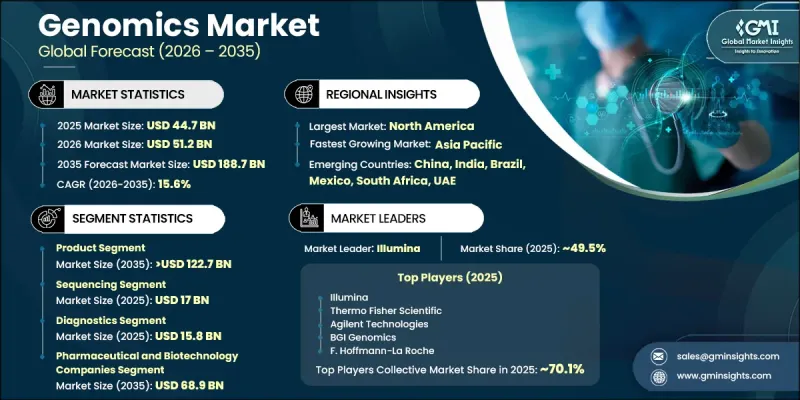

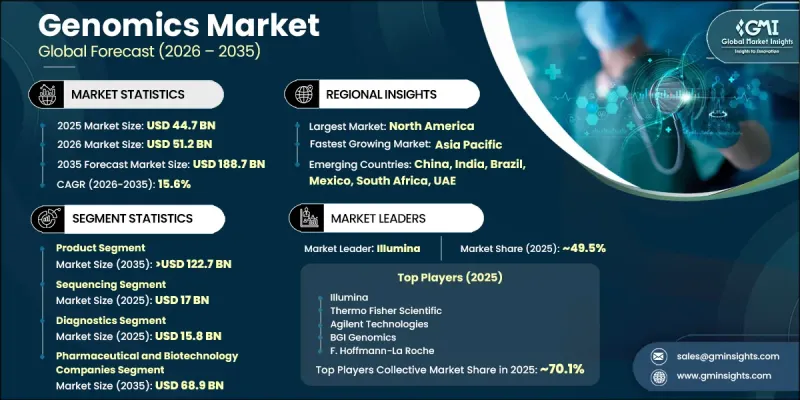

세계의 유전체학 시장은 2025년에 447억 달러로 평가되고 CAGR 15.6%로 성장하며, 2035년까지 1,887억 달러에 달할 것으로 예측됩니다.

유전체학 산업은 만성질환 및 유전성 질환의 유병률 증가와 더불어 정밀 의료 솔루션에 대한 수요가 높아짐에 따라 전 세계에서 인상적인 성장을 달성하고 있습니다. 유전체학는 생물학적 기능, 질병의 진행 과정 및 맞춤형 치료 접근법을 더 깊이 이해하기 위해 유전 물질의 포괄적인 분석에 중점을 두고 있습니다. 시퀀싱 기술, 유전자 분석 플랫폼, 인공지능, 생물정보학 분야의 지속적인 발전은 헬스케어 및 생명과학 분야 전반에 걸쳐 보다 정확하고 효율적인 게놈 응용 프로그램의 개발을 가속화하고 있습니다. 임상 진단, 치료법 개발, 제약 연구, 예방 의료에 유전체학이 통합됨에 따라 업계 상황은 크게 변화하고 있습니다. 또한 질환의 정확한 진단, 치료의 최적화, 표적 치료 분야에서 유전체 기술의 활용 확대가 시장의 추가적인 성장을 지원하고 있습니다. 업계 관계자들은 기술 혁신, 유전체 플랫폼 확충, 생명공학 및 헬스케어 생태계 전반에 걸친 전략적 제휴를 통해 적극적으로 역량 강화를 도모하고 있습니다. 또한 우호적인 규제 지원과 보상 제도의 개선 역시 전 세계 의료 시스템 및 연구 기관에서 유전체 솔루션의 보다 광범위한 도입을 지원하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 447억 달러 |

| 예측 시장 규모 | 1,887억 달러 |

| CAGR | 15.6% |

제품 부문은 2025년에 66.9%의 시장 점유율을 차지하며, 2035년까지 1,227억 달러에 달할 것으로 전망되어, 2026-2035년 연평균 성장률(CAGR) 15.3%를 기록할 것으로 보입니다. 이 부문에는 주로 조사 활동 및 진단 절차 수행에 필수적인 유전체 분석 장비 및 소모품이 포함됩니다. 게놈 장비의 기술적 발전으로 인해 운영 효율, 확장성, 분석 정확도가 크게 향상되어 연구 시설 및 임상 현장에서의 도입이 확대되고 있습니다. 소모품은 게놈 검사 및 실험실 워크플로우 전반에 걸쳐 반복적으로 사용되므로 여전히 이 부문에서 중요한 비중을 차지하고 있습니다. 신뢰성 높은 게놈 분석 및 대규모 연구 역량에 대한 수요가 증가함에 따라 해당 제품 부문의 성장이 더욱 가속화되고 있습니다.

시퀀싱 부문은 2025년에 170억 달러 규모의 시장을 기록했습니다. 기술 혁신을 통해 처리 속도, 정확도 및 전반적인 비용 효율성이 향상됨에 따라 시퀀싱 기술은 시장 확대에 있으며, 계속해서 핵심적인 역할을 수행하고 있습니다. 첨단 시퀀싱 플랫폼은 정확도 향상과 높은 처리 능력을 바탕으로 대규모 유전자 분석을 가능하게 하여, 연구 및 임상 현장에서의 폭넓은 응용을 지원하고 있습니다. 포괄적인 게놈 평가 및 질환 관련 분석에 시퀀싱 기술의 활용이 증가하고 있는 것은 헬스케어 및 생명공학 산업 전반에서 그 중요성을 높이고 있습니다. 지속적인 기술 발전과 효율적인 게놈 분석에 대한 수요 증가로 인해, 향후 수년간 시퀀싱 부문에서는 강력한 성장이 지속될 것으로 예상됩니다.

2025년, 북미 유전체학 시장은 42.7%의 점유율을 차지했습니다. 이 지역은 첨단인 헬스케어 인프라, 생의학 연구에 대한 강력한 집중, 그리고 임상 및 과학 분야에서의 유전체학 도입 확대를 통해 계속해서 선도적인 위치를 유지하고 있습니다. 헬스케어 분야로의 투자 확대, 생명공학 활동의 확대, 그리고 연구를 지원하는 환경이 해당 지역의 시장 성장에 기여하고 있습니다. 맞춤형 치료 접근법, 질환의 조기 발견, 그리고 첨단 진단 기술에 대한 수요가 증가함에 따라 북미 전역에서 이러한 기술의 도입이 가속화되고 있습니다. 주요 유전체학 혁신 기업의 존재와 시퀀싱, 진단, 생물정보학 분야의 지속적인 기술 개발이 해당 지역 시장 전체의 접근성과 혁신을 한층 더 높이고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 유형별, 2022-2035년

제6장 시장 추산·예측 : 기술별, 2022-2035년

제7장 시장 추산·예측 : 용도별, 2022-2035년

제8장 시장 추산·예측 : 최종 사용별, 2022-2035년

제9장 시장 추산·예측 : 지역별, 2022-2035년

제10장 기업 개요

KSA 26.06.24The Global Genomics Market was valued at USD 44.7 billion in 2025 and is estimated to grow at a CAGR of 15.6% to reach USD 188.7 billion by 2035.

The genomics industry is witnessing substantial growth worldwide due to the increasing prevalence of chronic and inherited disorders, along with rising demand for precision-based healthcare solutions. Genomics focuses on the comprehensive analysis of genetic material to better understand biological functions, disease progression, and individualized therapeutic approaches. Continuous advancements in sequencing technologies, gene analysis platforms, artificial intelligence, and bioinformatics are accelerating the development of more accurate and efficient genomic applications across healthcare and life sciences. The growing integration of genomics into clinical diagnostics, therapeutic development, pharmaceutical research, and preventive healthcare is significantly transforming the industry landscape. In addition, the rising adoption of genomic technologies in disease identification, treatment optimization, and targeted medicine is supporting broader market expansion. Industry participants are actively strengthening their capabilities through technological innovation, expansion of genomic platforms, and strategic collaborations across biotechnology and healthcare ecosystems. Favorable regulatory support and improving reimbursement structures are also encouraging the wider implementation of genomics solutions across healthcare systems and research institutions globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $44.7 Billion |

| Forecast Value | $188.7 Billion |

| CAGR | 15.6% |

The products segment accounted for 66.9% share in 2025 and is projected to reach USD 122.7 billion by 2035, growing at a CAGR of 15.3% 2026-2035. This segment primarily includes genomic instruments and consumable materials that are essential for conducting research activities and diagnostic procedures. Technological advancements in genomic equipment have significantly improved operational efficiency, scalability, and analytical accuracy, enabling greater adoption across research laboratories and clinical environments. Consumables continue to represent a critical portion of the segment due to their recurring use throughout genomic testing and laboratory workflows. Increasing demand for reliable genomic analysis and large-scale research capabilities is further driving growth within the products segment.

The sequencing segment generated USD 17 billion in 2025. Sequencing technologies continue to play a central role in market expansion as innovations improve processing speed, precision, and overall cost efficiency. Advanced sequencing platforms enable large-scale genetic analysis with enhanced accuracy and high-throughput capabilities, supporting wider application across research and clinical settings. The increasing use of sequencing technologies for comprehensive genomic evaluation and disease-related analysis is strengthening their importance across the healthcare and biotechnology industries. Ongoing technological progress and rising demand for efficient genomic interpretation are expected to sustain strong growth within the sequencing segment over the coming years.

North America Genomics Market held a 42.7% share in 2025. The region continues to maintain a leading position due to its advanced healthcare infrastructure, strong focus on biomedical research, and increasing implementation of genomics across clinical and scientific applications. Growing investments in precision healthcare initiatives, expanding biotechnology activities, and supportive research environments are contributing to regional market growth. Rising demand for personalized treatment approaches, early-stage disease identification, and advanced diagnostic technologies is also accelerating adoption throughout North America. The presence of major genomics innovators and continuous technological developments in sequencing, diagnostics, and bioinformatics are further enhancing accessibility and innovation across the regional market.

Key companies operating in the Global Genomics Market include Agilent Technologies, BGI Genomics, Bio-Rad Laboratories, Color Genomics, Danaher, Eppendorf, Eurofins Scientific, F. Hoffmann-La Roche, Illumina, Myriad Genetics, NVIDIA, Oxford Nanopore Technologies, Pacific Biosciences of California, QIAGEN, Quest Diagnostics, and Thermo Fisher Scientific. Companies operating in the Global Genomics Industry are adopting multiple strategic initiatives to strengthen their market position and expand their global presence. Leading players are heavily investing in research and development activities to introduce advanced sequencing systems, improved analytical software, and more efficient genomic testing solutions. Strategic partnerships with biotechnology firms, pharmaceutical companies, healthcare providers, and research organizations are helping companies accelerate innovation and broaden application areas. Market participants are also expanding their product portfolios through acquisitions and collaborations to enhance technological capabilities and improve service offerings. In addition, businesses are increasingly integrating artificial intelligence and data analytics into genomic platforms to improve data interpretation and operational efficiency. Several companies are focusing on geographic expansion, laboratory network development, and automation technologies to improve accessibility, streamline workflows, and strengthen long-term customer relationships across the global genomics market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of genetic and chronic diseases

- 3.2.1.2 Advancements in DNA sequencing and gene editing technologies

- 3.2.1.3 Increasing adoption of precision medicine

- 3.2.1.4 Government initiatives and funding for genomics research

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Ethical and privacy concerns around genetic data

- 3.2.2.2 High cost and affordability issues

- 3.2.3 Market opportunities

- 3.2.3.1 Development of affordable and rapid sequencing technologies

- 3.2.3.2 Integration of AI and machine learning for enhanced genomic data analysis

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technology

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.6 Regulatory landscape (Driven by primary research)

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East and Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Impact of AI and generative AI on the market

- 3.10 Future market trends (Driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Products

- 5.2.1 Instruments

- 5.2.2 Consumables and reagents

- 5.3 Services

- 5.3.1 NGS-based services

- 5.3.2 Core genomics services

- 5.3.3 Biomarker translation services

- 5.3.4 Computational services

- 5.3.5 Other services

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 PCR (polymerase chain reaction)

- 6.3 Sequencing

- 6.4 Microarray

- 6.5 Nucleic acid extraction and purification

- 6.6 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Diagnostics

- 7.3 Drug discovery and development

- 7.4 Precision medicine

- 7.5 Agriculture and animal research

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Research centers and academic and government institutes

- 8.4 Pharmaceutical and biotechnology companies

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Agilent Technologies

- 10.2 BGI Genomics

- 10.3 Bio-Rad Laboratories

- 10.4 Color Genomics

- 10.5 Danaher

- 10.6 Eppendorf

- 10.7 Eurofins Scientific

- 10.8 F. Hoffmann-La Roche

- 10.9 Illumina

- 10.10 Myriad Genetics

- 10.11 NVIDIA

- 10.12 Oxford Nanopore Technologies

- 10.13 Pacific Biosciences of California

- 10.14 QIAGEN

- 10.15 Quest Diagnostics

- 10.16 Thermo Fisher Scientific