|

시장보고서

상품코드

2061434

식물생장조절제 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Plant Growth Regulators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

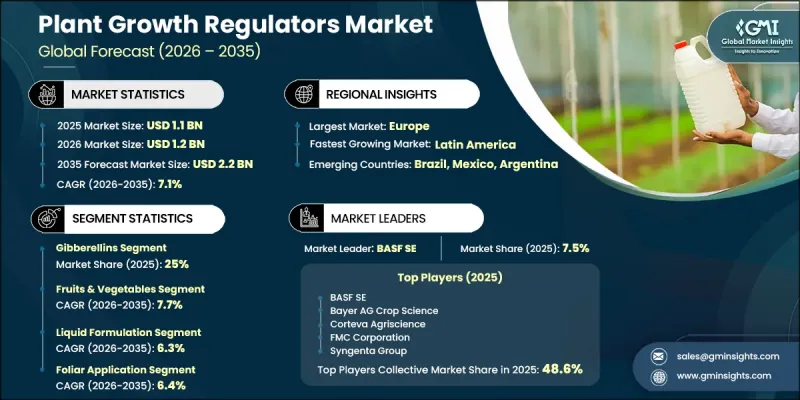

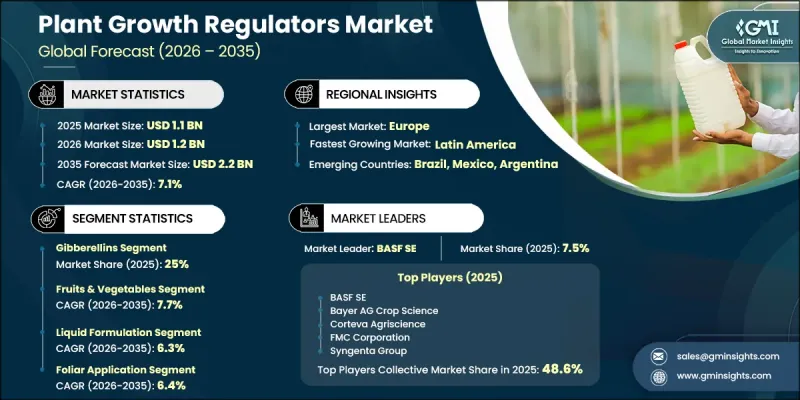

세계의 식물생장조절제 시장은 2025년에 11억 달러로 평가되고 CAGR 7.1%로 성장하며, 2035년까지 22억 달러에 달할 것으로 추정되고 있습니다.

이 시장은 변화하는 환경 조건 속에서 농작물의 품질을 유지하면서 농업 생산성을 향상시켜야 할 필요성이 커짐에 따라 계속해서 성장하고 있습니다. 식물 생장 조절제는 생장 속도, 개화, 과실 발달, 스트레스 반응 메커니즘 등 식물의 생리적 과정을 제어하고 조절하기 위해 현대 농업에서 널리 사용되고 있습니다. 이러한 중요성의 증대는 인구 증가와 경작 가능지의 감소로 인해 발생하는 식량 시스템에 대한 전 세계적 압박과 밀접한 관련이 있습니다. 농가는 수확 효율을 높이고 가뭄, 염해, 기온 변동 등 비생물적 스트레스에 대한 내성을 강화하기 위해 이러한 솔루션에 대한 의존도를 높이고 있습니다. 또한 식물 성장 조절제는 투입 자재의 최적화와 환경 부담 감소를 지원함으로써, 지속가능한 농업 실천으로의 전환도 시장 성장에 크게 기여하고 있습니다. 정밀농업 기술은 효과를 높이는 동시에 낭비를 최소화하는 표적형 시비법을 가능하게 함으로써, 식물 성장 조절제의 도입을 더욱 촉진하고 있습니다. 이러한 제품들은 엽면 살포, 종자 처리, 토양 투여 시스템 등의 기술을 활용하여 곡물, 과일, 채소, 관상용 작물에 널리 적용되고 있습니다. 바이오 기반 제제, 개선된 전달 메커니즘, 친환경 화학 물질에 대한 지속적인 혁신 덕분에 전 세계 상업 농업 시스템에서 식물 성장 조절제의 중요성은 더욱 커지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 금액 | 11억 달러 |

| 예측 금액 | 22억 달러 |

| CAGR | 7.1% |

지베렐린 부문은 2025년에 25%의 시장 점유율을 차지하며, 2035년까지 연평균 성장률(CAGR) 7.4%로 성장할 것으로 전망됩니다. 이 부문은 줄기의 신장, 종자의 발아, 개화, 그리고 작물의 전반적인 생육과 같은 주요 식물 기능을 조절하는 역할을 담당하고 있으므로 여전히 매우 중요한 위치를 차지하고 있습니다. 농가가 다양한 농업 시스템에서 생산성과 작물의 균일성 향상을 추구하는 가운데, 밭작물 및 원예 분야에서의 도입 확대가 안정적인 수요를 지속적으로 지원하고 있습니다. 또한 이 부문은 효율성과 살포 정밀도를 높인 개량된 제제에 대한 지속적인 연구의 혜택을 받고 있습니다.

과일·채소 부문은 2025년에 41%의 시장 점유율을 차지하며, 2026-2035년 연평균 성장률(CAGR) 7.7%로 성장할 것으로 전망됩니다. 이 부문의 수요는 전 세계 신선 농산물 소비량의 증가와 외관 품질, 유통 기한, 병해 저항성에 대한 중요성이 커짐에 따라 견인되고 있습니다. 농가는 과실의 크기를 최적화하고, 착색을 개선하며, 균일한 숙성을 보장하기 위해 식물 성장 조절제를 사용하고 있으며, 이를 통해 까다로운 소매 및 수출 기준을 충족할 수 있게 되었습니다. 지속가능하고 잔류물이 없는 농업 실천에 대한 관심이 높아짐에 따라 첨단이고 환경을 고려한 식물 생장 조절제 솔루션의 활용도 확대되고 있습니다. 또한 원예 생산의 확대와 온실 재배의 확산이 이 부문의 시장 성장을 더욱 가속화하고 있습니다.

북미의 식물 생장 조절제 시장은 첨단인 농업 방식과 정밀농업 기술의 보급에 힘입어 2025년에는 27%의 시장 점유율을 차지했습니다. 이 지역은 생산성, 효율성, 지속가능성을 중시하는 잘 구축된 농업 생태계의 혜택을 누리고 있습니다. 미국과 캐나다의 농가는 수확량의 품질과 안정성을 높이기 위해 작물 관리 전략에 식물 성장 조절제를 점점 더 많이 도입하고 있습니다. 환경 안전성과 제품의 효능을 우선시하는 규제 체계가 바이오 기반 및 친환경 제제의 개발을 지원하고 있습니다. 농업 연구개발에 대한 적극적인 투자와 디지털 농업 툴의 도입 확대가 맞물리면서, 해당 지역의 상업 농업 사업 전반에 걸쳐 식물 생장 조절제의 혁신과 활용이 더욱 가속화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 유효 성분 유형별, 2022-2035년

제6장 시장 추산·예측 : 작물 적용별, 2022-2035년

제7장 시장 추산·예측 : 제제 유형별, 2022-2035년

제8장 시장 추산·예측 : 시용 방법별, 2022-2035년

제9장 시장 추산·예측 : 최종사용자 산업별, 2022-2035년

제10장 시장 추산·예측 : 지역별, 2022-2035년

제11장 기업 개요

KSA 26.06.24The Global Plant Growth Regulators Market was valued at USD 1.1 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 2.2 billion by 2035.

The market is experiencing expansion driven by the increasing need to improve agricultural productivity while maintaining crop quality under changing environmental conditions. Plant growth regulators are widely used in modern agriculture to control and modify plant physiological processes such as growth rate, flowering, fruit development, and stress response mechanisms. Their growing importance is closely tied to the global pressure on food systems caused by rising population levels and shrinking arable land availability. Farmers are increasingly relying on these solutions to enhance yield efficiency and improve resilience against abiotic stresses such as drought, salinity, and temperature fluctuations. The shift toward sustainable farming practices is also contributing significantly to market growth, as plant growth regulators support optimized input use and reduced environmental impact. Precision agriculture technologies are further strengthening adoption by enabling targeted application methods that improve effectiveness while minimizing waste. These products are widely applied across cereals, fruits, vegetables, and ornamental crops using techniques such as foliar application, seed treatment, and soil-based delivery systems. Continuous innovation in bio-based formulations, improved delivery mechanisms, and environmentally friendly chemistries is further expanding the relevance of plant growth regulators in commercial farming systems worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.1 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 7.1% |

The gibberellins segment accounted for a share of 25% in 2025 and is projected to grow at a CAGR of 7.4% through 2035. This segment remains highly important due to its role in regulating key plant functions such as stem elongation, seed germination, flowering, and overall crop development. Increased adoption in both field crops and horticultural applications continues to support steady demand, as growers aim to improve productivity and crop uniformity across different agricultural systems. The segment is also benefiting from ongoing research into improved formulations that enhance efficiency and application accuracy.

The fruits and vegetables segment held a share of 41% in 2025 and is anticipated to grow at a CAGR of 7.7% during 2026 to 2035. Demand within this segment is being driven by the rising global consumption of fresh produce and the increasing emphasis on visual quality, shelf life, and disease resistance. Farmers are adopting plant growth regulators to optimize fruit size, improve coloration, and ensure uniform ripening, which helps meet strict retail and export standards. The growing focus on sustainable and residue-free farming practices is also supporting the use of advanced and environmentally compatible plant growth regulator solutions. Additionally, expanding horticultural production and greenhouse cultivation practices are further strengthening market growth in this category.

North America Plant Growth Regulators Market accounted for 27% share in 2025 supported by advanced agricultural practices and high adoption of precision farming technologies. The region benefits from a well-developed agricultural ecosystem that emphasizes productivity, efficiency, and sustainability. Farmers across the United States and Canada are increasingly integrating plant growth regulators into crop management strategies to improve yield quality and consistency. Regulatory frameworks that prioritize environmental safety and product efficacy are encouraging the development of bio-based and eco-friendly formulations. Strong investment in agricultural research, combined with the rising adoption of digital farming tools, is further accelerating innovation and usage of plant growth regulators across commercial farming operations in the region.

Key companies operating in the Global Plant Growth Regulators Industry include BASF SE, Bayer AG Crop Science, Corteva Agriscience, Syngenta Group, FMC Corporation, Nufarm Limited, Sumitomo Chemical Co. Ltd., Sipcam Oxon S.p.A., Tata Chemicals Ltd., Valent BioSciences LLC, Fine Americas, Inc., Crop Care Australasia Pty Ltd., Nippon Soda Co. Ltd., UPL Limited, and Xinyi Industrial Co. Ltd. Companies operating in the plant growth regulators market are focusing on product innovation, biological formulation development, and strategic expansion to strengthen their competitive position. A major priority is the development of bio-based and environmentally friendly solutions that align with sustainable agriculture practices and evolving regulatory standards. Market players are investing heavily in research and development to improve product efficiency, crop specificity, and application precision. Strategic partnerships with agricultural research institutions and distribution networks are also being used to expand geographic reach and improve product accessibility. Companies are increasingly leveraging precision agriculture technologies, including data-driven application systems, to enhance performance outcomes and farmer adoption rates.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Active ingredients type

- 2.2.3 Crop application

- 2.2.4 Formulation type

- 2.2.5 Application method

- 2.2.6 End User Industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Active Ingredient Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Auxins

- 5.2.1 Indole-3-Acetic Acid (IAA)

- 5.2.2 Indole-3-Butyric Acid (IBA)

- 5.2.3 Naphthaleneacetic Acid (NAA)

- 5.2.4 2,4-Dichlorophenoxyacetic Acid (2,4-D)

- 5.2.5 Other Auxins

- 5.3 Cytokinins

- 5.3.1 Kinetin

- 5.3.2 Zeatin

- 5.3.3 6-Benzylaminopurine (6-BA / Benzyl Adenine)

- 5.3.4 Other cytokinins

- 5.4 Gibberellins

- 5.4.1 Gibberellic acid (GA3)

- 5.4.2 GA4+7 complex

- 5.4.3 Other gibberellins (GA1, GA5, GA6)

- 5.5 Ethylene & ethylene modulators

- 5.5.1 Ethylene donors (Ethephon/Ethrel)

- 5.5.2 Ethylene inhibitors (AVG, 1-MCP)

- 5.6 Abscisic acid (ABA)

- 5.6.1 Natural abscisic acid

- 5.6.2 Synthetic abscisic acid (S-ABA)

- 5.7 Growth retardants (anti-gibberellins)

- 5.7.1 Chlormequat chloride

- 5.7.2 Mepiquat chloride

- 5.7.3 Paclobutrazol

- 5.7.4 Trinexapac-ethyl

- 5.7.5 Prohexadione calcium

- 5.7.6 Daminozide

- 5.7.7 Other growth retardants

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Crop Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.1.1 Fruits & vegetables

- 6.1.1.1 Fruit crops

- 6.1.1.2 Citrus

- 6.1.1.3 Grapes

- 6.1.1.4 Pome fruits

- 6.1.1.5 Stone fruits

- 6.1.1.6 Berries

- 6.1.1.7 Tropical fruits

- 6.1.1.8 Other fruits

- 6.1.2 Vegetable crops

- 6.1.2.1 Fruiting vegetables

- 6.1.2.2 Leafy vegetables

- 6.1.2.3 Root vegetables

- 6.1.2.4 Cucurbits

- 6.1.2.5 Other vegetables

- 6.1.1 Fruits & vegetables

- 6.2 Cereals & grains

- 6.2.1 Wheat

- 6.2.2 Rice

- 6.2.3 Maize/corn (field corn only)

- 6.2.4 Barley

- 6.2.5 Oats

- 6.2.6 Sorghum

- 6.2.7 Other cereals (rye, millet, triticale)

- 6.3 Oilseeds & pulses

- 6.3.1 Oilseeds

- 6.3.1.1 Soybeans

- 6.3.1.2 Canola/rapeseed

- 6.3.1.3 Sunflower

- 6.3.1.4 Cotton (cottonseed oil)

- 6.3.1.5 Other oilseeds

- 6.3.2 Pulses

- 6.3.2.1 Lentils

- 6.3.2.2 Chickpeas

- 6.3.2.3 Dry beans

- 6.3.2.4 Peas

- 6.3.2.5 Other pulses (faba beans, pigeon peas)

- 6.3.1 Oilseeds

- 6.4 Turf & ornamentals

- 6.4.1 Turf/turfgrass management

- 6.4.1.1 Golf courses

- 6.4.1.2 Sports fields & athletic facilities

- 6.4.1.3 Residential lawns

- 6.4.1.4 Commercial landscapes

- 6.4.2 Ornamental plants

- 6.4.2.1 Cut flowers

- 6.4.2.2 Potted plants

- 6.4.2.3 Bedding plants

- 6.4.2.4 Nursery stock

- 6.4.2.5 Landscape plants

- 6.4.1 Turf/turfgrass management

Chapter 7 Market Estimates and Forecast, By Formulation Type, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Liquid Formulations

- 7.2.1 Soluble Concentrates (SL)

- 7.2.2 Emulsifiable Concentrates (EC)

- 7.2.3 Suspension Concentrates (SC)

- 7.2.4 Aqueous Solutions (Ready-to-Use)

- 7.3 Solid Formulations

- 7.3.1 Wettable Powders (WP)

- 7.3.2 Water-Dispersible Granules (WDG/WG)

- 7.3.3 Soluble Granules (SG)

- 7.3.4 Dry Flowable (DF)

- 7.4 Specialized Formulations

- 7.4.1 Microencapsulated Formulations

- 7.4.2 Slow-Release/Controlled-Release Formulations

- 7.4.3 Aerosol/Spray Formulations

- 7.4.4 Other Specialty Forms (Gels, Pastes, Tablets)

Chapter 8 Market Estimates and Forecast, By Application Method, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Foliar application

- 8.3 Soil application

- 8.4 Seed treatment

- 8.5 Direct plant application

Chapter 9 Market Estimates and Forecast, By End User Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Commercial agriculture

- 9.3 Specialty & high-value crop producers

- 9.4 Turf & landscape professionals

- 9.5 Institutional & government

- 9.6 Retail / consumer

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 BASF SE

- 11.2 Bayer AG Crop Science

- 11.3 Corteva Agriscience

- 11.4 Crop Care Australasia Pty Ltd.

- 11.5 Fine Americas, Inc.

- 11.6 FMC Corporation

- 11.7 Nippon Soda Co. Ltd.

- 11.8 Nufarm Limited

- 11.9 Sipcam Oxon S.p.A.

- 11.10 Sumitomo Chemical Co. Ltd.

- 11.11 Syngenta Group

- 11.12 Tata Chemicals Ltd.

- 11.13 UPL Limited

- 11.14 Valent BioSciences LLC

- 11.15 Xinyi Industrial Co. Ltd.