|

시장보고서

상품코드

2061454

DNA 합성 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)DNA Synthesis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

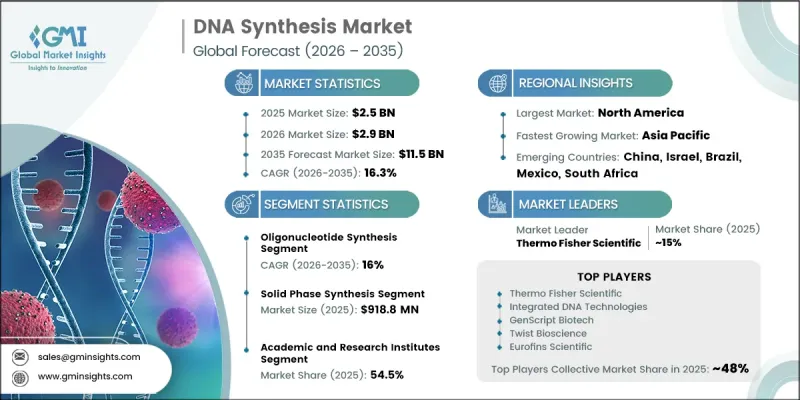

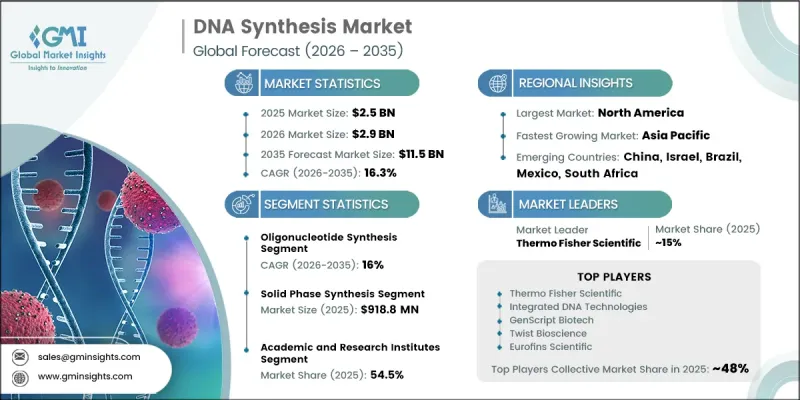

세계의 DNA 합성 시장은 2025년에 25억 달러로 평가되고 CAGR 16.3%로 성장하며, 2035년까지 115억 달러에 달할 것으로 추정되고 있습니다.

분자생물학, 합성생물학, 유전공학, 임상진단 등의 분야에서 합성 DNA에 대한 수요가 증가함에 따라 시장은 강력한 성장세를 보이고 있습니다. 유전성 질환 및 만성질환의 유병률 증가는 신약 개발, 백신 개발, 그리고 맞춤형 의료 분야에서 첨단 연구 필요성을 더욱 강조하고 있습니다. 생명공학에 대한 투자 확대, 고처리량 합성 플랫폼의 도입 확대, 그리고 유전체학 분야의 지속적인 기술 발전이 업계 성장을 더욱 지원하고 있습니다. 또한 첨단 상용 합성 서비스의 이용 가능성과 생명과학 분야에서 DNA 기반 연구 툴의 통합이 진행되고 있는 점이 전 세계적인 보급을 가속화하고 있습니다. 또한 차세대 유전자 솔루션 개발에 주력하는 생명공학 기업, 제약사, 연구 기관 간의 협력이 강화되고 있는 점도 시장에 긍정적인 요인으로 작용하고 있습니다. 정밀 의료와 설계된 생물학적 시스템에 대한 관심이 높아지면서 장기적인 수요가 더욱 촉진되고 있는 한편, 합성 워크플로우의 자동화 및 디지털화를 통해 모든 용도에서 확장성, 속도, 정밀도가 향상되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035 |

| 개시 금액 | 25억 달러 |

| 예측액 | 115억 달러 |

| CAGR | 16.3% |

DNA 합성이란 화학적 또는 효소적 방법을 이용하여 실험실에서 인공적인 DNA 서열을 만드는 것을 말합니다. 이 과정을 통해 유전자 편집, 치료법 개발, 분자 진단, 백신 연구, 합성 생물학 등 폭넓은 분야에서 사용되는 맞춤형 유전 물질을 정밀하게 구축할 수 있게 됩니다. 또한 상업적 목적과 연구 목적 모두에서 설계된 유전자, 생물학적 경로 및 복잡한 생명 시스템의 설계를 지원함으로써, 현대 생명공학 분야에서 기초적인 역할을 수행하고 있습니다. 이 기술은 첨단 생명공학 워크플로우에 점점 더 많이 통합되면서, 생명과학 산업 전반에 걸쳐 보다 신속한 실험과 혁신을 가능하게 하고 있습니다.

올리고뉴클레오티드 합성 부문은 2026-2035년 연평균 성장률(CAGR) 16%를 기록하며 성장할 것으로 전망됩니다. 이러한 우위는 주로 PCR, qPCR, 유전자 염기서열 분석, 클로닝 및 유전자 편집 응용 분야에서 높은 활용도에 힘입은 것입니다. 이러한 짧은 DNA 단편은 임상 및 연구 환경 모두에서 필수적인 실험실 소모품으로 널리 사용되고 있으며, 안정적이고 지속적인 수요를 창출하고 있습니다. 업계 관계자들의 지속적인 제품 혁신과 전략적 제휴가 이 부문의 성장을 더욱 지원하고 있습니다.

2025년 기준으로, 학술·연구 기관 부문은 54.5%의 점유율을 차지했습니다. 이러한 선도적 지위는 게놈 연구, 분자 클로닝, 기능 생물학 연구, 경로 공학, 그리고 보다 광범위한 생명과학 연구 분야에서 합성 DNA가 폭넓게 활용됨에 따라 주도되고 있습니다. 대학, 정부 연구소, 연구 센터에 대한 공공 및 민간 기관의 지속적인 자금 지원 덕분에, 모든 과학 분야에서 올리고뉴클레오티드 및 유전자 합성 서비스에 대한 강력한 수요가 지속적으로 유지되고 있습니다.

북미의 DNA 합성 시장은 2025년에 38.7%의 점유율을 차지했습니다. 이 지역의 경쟁력은 생명공학 및 유전체 연구에 대한 막대한 투자뿐만 아니라, 주요 DNA 합성 기업의 입지와 고도로 발달된 연구 인프라에 의해 지원되고 있습니다. 강력한 정부 지원에 더해, 업계 관계자 및 연구 기관과의 협력이 추가적인 성장을 이끌고 있습니다. 이 지역은 제약 기업, 합성생물학 개발 기업, 수탁 연구 기관 및 학술기관을 포함한 성숙한 생명공학 생태계의 혜택을 누리고 있으며, 이들 기관은 신약 개발 및 첨단 연구 용도로 고처리량 DNA 합성 기술을 적극적으로 활용하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 서비스별, 2022-2035년

제6장 시장 추산·예측 : 방법별, 2022-2035년

제7장 DNA 합성 시장의 규모와 예측 : 용도별, 2022-2035년

제8장 DNA 합성 시장의 규모와 예측 : 최종 용도별, 2022-2035년

제9장 DNA 합성 시장의 규모와 예측 : 지역별, 2022-2035년

제10장 기업 개요

KSAThe Global DNA Synthesis Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 16.3% to reach USD 11.5 billion by 2035.

The market is experiencing strong momentum due to rising demand for synthetic DNA across molecular biology, synthetic biology, genetic engineering, and clinical diagnostics applications. Increasing prevalence of genetic and chronic diseases is further strengthening the need for advanced research in drug discovery, vaccine development, and personalized medicine. Expanding biotechnology investments, growing adoption of high-throughput synthesis platforms, and continuous technological improvements in genomics are further supporting industry expansion. In addition, the availability of advanced commercial synthesis services and rising integration of DNA-based research tools in life sciences are accelerating global adoption. The market is also benefiting from increasing collaboration between biotechnology firms, pharmaceutical companies, and research institutions focused on developing next-generation genetic solutions. Growing emphasis on precision medicine and engineered biological systems is further reinforcing long-term demand, while automation and digitalization in synthesis workflows are improving scalability, speed, and accuracy across applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 16.3% |

DNA synthesis is defined as the laboratory-based creation of artificial DNA sequences using chemical or enzymatic techniques. This process enables the precise construction of customized genetic material used in a wide range of applications such as gene editing, therapeutic development, molecular diagnostics, vaccine research, and synthetic biology. It plays a foundational role in modern biotechnology by supporting the design of engineered genes, biological pathways, and complex living systems for both commercial and research purposes. The technology is increasingly integrated into advanced biological engineering workflows, enabling faster experimentation and innovation across life sciences industries.

The oligonucleotide synthesis segment is projected to grow at a CAGR of 16% during 2026-2035. Its dominance is mainly supported by strong utilization in PCR, qPCR, gene sequencing, cloning, and gene-editing applications. These short DNA fragments are widely used as essential laboratory consumables in both clinical and research environments, creating steady and recurring demand. Ongoing product innovations and strategic partnerships among industry participants are further strengthening segment growth.

The academic and research institutes segment accounted for a share of 54.5% in 2025. This leadership is driven by extensive use of synthetic DNA in genomics research, molecular cloning, functional biology studies, pathway engineering, and broader life science investigations. Consistent funding support from public and private organizations for universities, government laboratories, and research centers continues to sustain strong demand for oligonucleotide and gene synthesis services across scientific disciplines.

North America DNA Synthesis Market held a 38.7% share in 2025. The region's dominance is supported by significant investments in biotechnology and genomics research, along with the presence of leading DNA synthesis companies and highly advanced research infrastructure. Strong government support, along with collaborations between industry participants and research organizations, is further driving growth. The region benefits from a mature biotechnology ecosystem that includes pharmaceutical companies, synthetic biology developers, contract research organizations, and academic institutions actively utilizing high-throughput DNA synthesis technologies for drug discovery and advanced research applications.

Prominent players operating in the Global DNA synthesis industry include GenScript Biotech, Thermo Fisher Scientific, Eurofins Scientific, Integrated DNA Technologies, Twist Bioscience, BIOMATIK, Bioneer, Eton Bioscience, IBA Lifesciences, Kaneka Eurogentec, LGC Biosearch Technologies, OriGene Technologies, ProMab Biotechnologies, ProteoGenix, Quintara Biosciences, Shenzhen Shuxin Biotechnology, Synbio Technologies, and LGC Biosearch Technologies. Companies operating in the DNA synthesis market are increasingly focusing on technological innovation, automation, and scalability to strengthen their market position. A key strategy includes expanding high-throughput synthesis capabilities to meet rising demand from research and pharmaceutical applications. Market players are heavily investing in next-generation synthesis platforms that improve speed, accuracy, and cost efficiency. Strategic collaborations with biotechnology firms, academic institutes, and pharmaceutical companies are also enhancing product development and application reach. Many companies are strengthening their global distribution networks and expanding service portfolios to include customized DNA design and rapid delivery solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis

- 2.1.1 Regional trends

- 2.1.2 Service trends

- 2.1.3 Method trends

- 2.1.4 Application trends

- 2.1.5 End Use trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of diseases globally

- 3.2.1.2 Rapid technology advancements in the field of synthetic biology

- 3.2.1.3 Rising investments towards research and development(R&D) activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent government regulations and guidelines

- 3.2.2.2 High cost, potential biosafety,biosecurity and ethical issues

- 3.2.3 Market opportunities

- 3.2.3.1 Advancement of enzymatic and cell-free DNA synthesis technologies

- 3.2.3.2 Expansion of DNA data storage commercialization opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Automation and high-throughput DNA synthesis platforms

- 3.5.1.2 Advancements in enzymatic DNA synthesis

- 3.5.2 Emerging technologies

- 3.5.2.1 Integration with cell-free and cell-based manufacturing systems

- 3.5.2.2 Cloud-based DNA synthesis platforms and digital labs

- 3.5.1 Current technological trends

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Impact of AI and Generative AI on the market (Driven by Primary Research)

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Service, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Oligonucleotide synthesis

- 5.2.1 Standard oligonucleotide synthesis

- 5.2.2 Custom oligonucleotide synthesis

- 5.3 Gene Synthesis

- 5.3.1 Custom gene synthesis

- 5.3.2 Gene library synthesis

Chapter 6 Market Estimates and Forecast, By Method, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Solid phase synthesis

- 6.3 PCR-based enzyme synthesis

- 6.4 CHIP-based DNA synthesis

Chapter 7 DNA Synthesis Market Size and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Research and development

- 7.3 Diagnostics

- 7.4 Therapeutics

Chapter 8 DNA Synthesis Market Size and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Academic and research institutes

- 8.3 Contract research organizations

- 8.4 Biopharmaceutical companies

Chapter 9 DNA Synthesis Market Size and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East & Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 BIOMATIK

- 10.2 Bioneer

- 10.3 Eton Bioscience

- 10.4 Eurofins Scientific

- 10.5 GenScript Biotech

- 10.6 IBA Lifesciences

- 10.7 Integrated DNA Technologies

- 10.8 Kaneka Eurogentec

- 10.9 LGC Biosearch Technologies

- 10.10 OriGene Technologies

- 10.11 ProMab Biotechnologies

- 10.12 ProteoGenix

- 10.13 Quintara Biosciences

- 10.14 Shenzhen Shuxin Biotechnology

- 10.15 Synbio Technologies

- 10.16 Thermo Fisher Scientific

- 10.17 Twist Bioscience