|

시장보고서

상품코드

2061477

PARP 저해제 바이오마커 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)PARP Inhibitor Biomarkers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

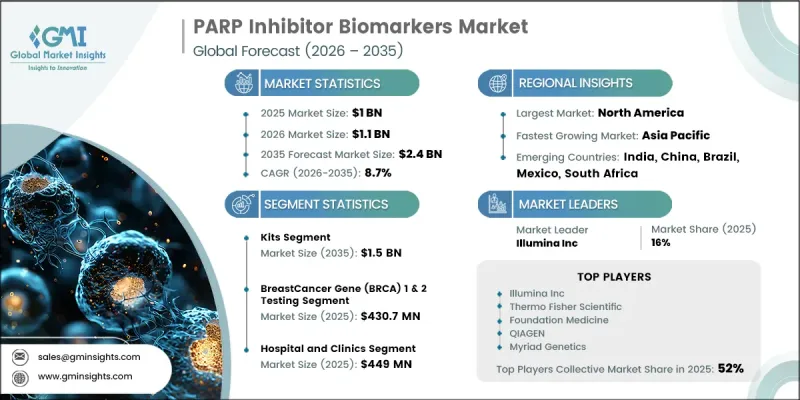

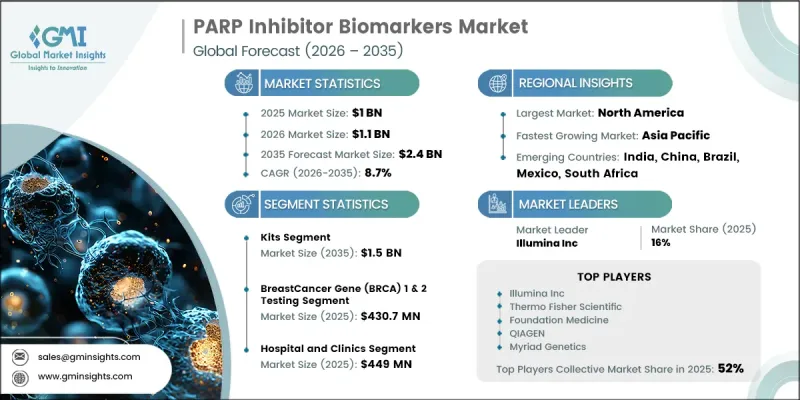

세계의 PARP 저해제 바이오마커 시장은 2025년에 10억 달러로 평가되고 CAGR 8.7%로 성장하며, 2035년까지 24억 달러에 달할 것으로 예측됩니다.

유방암 발병률의 증가, 유전체 연구의 급속한 발전, 그리고 전 세계적인 암 치료 투자 확대에 힘입어 이 시장은 인상적인 성장세를 보이고 있습니다. 의료 종사자들이 치료 효과와 환자 예후를 개선하는 표적 치료에 지속적으로 주력하는 가운데, PARP 억제제 바이오마커는 정밀 의학에서 필수적인 요소로 자리 잡고 있습니다. 또한 의료 종사자들이 더 높은 정확도로 적합한 환자를 선별할 수 있게 해주는 분자 진단 기술의 발전도 이 업계에 혜택을 주고 있습니다. 암의 조기 발견과 맞춤형 의료에 대한 인식이 높아짐에 따라 바이오마커 기반 검사 솔루션에 대한 수요도 더욱 증가하고 있습니다. 또한 제약회사와 진단기기 제조업체들은 임상적 판단을 개선할 수 있는 첨단 검사 기술을 개발하기 위한 연구 활동을 강화하고 있습니다. 헬스케어 인프라 확충, 동반진단의 보급 확대, 그리고 정밀 종양학 솔루션에 대한 수요 증가가 맞물려 시장 발전을 가속화하고 있습니다. 첨단 유전자 검사가 일상적인 임상 워크플로우에 통합되는 것 외에도, 바이오마커 기반 치료법의 수용이 확대되고 있는 점이 앞으로도 PARP 억제제 바이오마커 업계의 장기적인 전망을 계속해서 형성해 나갈 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 10억 달러 |

| 예측액 | 24억 달러 |

| CAGR | 8.7% |

PARP 억제제 바이오마커란, PARP 억제제 치료의 효과를 잘 볼 수 있는 암 환자를 식별하는 데 도움이 되는 유전적 지표입니다. 이러한 바이오마커는 표적 치료 전략을 지원하고 치료 성과를 향상시키기 위해 정밀 종양학 분야에서 널리 활용되고 있습니다. 전 세계에서 증가하는 유방암의 부담은 첨단 바이오마커 검사 솔루션에 대한 강력한 수요를 지속적으로 창출하고 있습니다. 분자 프로파일링 및 차세대 진단 기술의 활용 확대는 환자 선정 및 치료 계획 수립을 한층 더 개선하는 데 기여하고 있습니다. 또한 맞춤형 암 치료에 대한 관심이 높아지고 있는 것이 헬스케어 시스템 전반에 걸쳐 바이오마커 기반 진단의 도입을 촉진하고 있습니다. 암 치료비 증가와 첨단 치료법의 보급 역시 시장 확대를 지원하고 있습니다. 의료 서비스 제공자들이 치료 효율이 높은 표적 치료법을 점점 더 우선시함에 따라 예측 기간 중 PARP 억제제 바이오마커에 대한 수요는 꾸준히 증가할 것으로 예상됩니다.

키트 부문은 병원, 연구 시설, 진단 검사실 전반에 걸친 견고한 수요에 힘입어 2035년까지 15억 달러에 달할 것으로 전망됩니다. 이 부문은 편의성, 표준화된 워크플로우, 그리고 바이오마커 검사 절차를 간소화하는 능력 덕분에 계속해서 성장세를 보이고 있습니다. 즉시 사용형 검사 키트는 업무의 복잡성을 줄여주는 동시에, 검사 결과 보고까지 걸리는 시간(턴어라운드 타임)과 검사실의 효율을 향상시킵니다. 임상 현장에서의 광범위한 도입은 대규모 선별 검사 및 정밀 종양학 프로그램의 추진에도 기여하고 있습니다. 또한 각 제조사는 정밀도, 신뢰성 및 워크플로우와의 호환성을 향상시키도록 설계된 기술적으로 진보된 키트를 지속적으로 출시하고 있습니다. 자동화되고 사용자 친화적인 솔루션의 이용 가능성이 높아짐에 따라 PARP 억제제 바이오마커 시장에서 키트 부문의 입지가 더욱 공고해지고 있습니다.

유방암 유전자(BRCA) 1 및 2 검사 부문은 2025년에 4억 3,070만 달러의 시장 규모를 기록했습니다. BRCA 검사는 표적형 PARP 억제제 치료의 대상이 되는 환자를 선별하는 데 있으며, 매우 중요한 역할을 하고 있으므로 시장에서 주도적인 위치를 유지하고 있습니다. 이러한 검사는 특히 유방암이나 난소암으로 진단받은 환자를 대상으로, 임상종양학 진료 현장에서 널리 활용되고 있습니다. 유전자 선별 프로그램의 보급이 확대되고, BRCA 검사를 권장하는 임상 지침이 늘어나면서 이 부문의 성장이 가속화되고 있습니다. 또한 유전성 암 위험에 대한 인식이 높아지고 유전 상담 서비스 이용 기회가 확대됨에 따라 더 많은 사람들이 조기 검진을 받고 있습니다. 정밀진단과 조기 치료 개입에 대한 관심이 높아짐에 따라 BRCA 1 및 2 검사 솔루션에 대한 수요는 더욱 증가할 것으로 예상됩니다.

북미의 PARP 억제제 바이오마커 시장은 2025년에 40.7%의 점유율을 차지했습니다. 이 지역 시장은 유방암 유병률의 증가와 첨단 진단 기술의 도입 확대에 힘입어 강력한 성장을 달성하고 있습니다. 이 지역에서는 매년 수많은 암 진단이 이루어지고 있으며, 바이오마커에 기반한 치료 전략에 대한 수요가 크게 증가하고 있습니다. 암 검진 및 조기 진단 프로그램에 대한 인식이 높아진 것도 의료기관 전체의 검사 건수 증가에 기여하고 있습니다. 또한 BRCA 돌연변이와 관련된 유전성 유방암 사례의 증가로 인해 PARP 억제제 바이오마커 검사의 도입이 가속화되고 있습니다. 탄탄한 의료 인프라, 높은 의료 지출, 그리고 정밀 종양학의 지속적인 발전이 북미 전역에서 시장의 지속적인 성장을 지원할 것으로 예상됩니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품별, 2022-2035년

제6장 시장 추산·예측 : 서비스별, 2022-2035년

제7장 시장 추산·예측 : 기술별, 2022-2035년

제8장 시장 추산·예측 : 용도별, 2022-2035년

제9장 시장 추산·예측 : 최종 사용별, 2022-2035년

제10장 시장 추산·예측 : 지역별, 2022-2035년

제11장 기업 개요

KSA 26.06.24The Global PARP Inhibitor Biomarkers Market was valued at USD 1 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 2.4 billion by 2035.

The market is witnessing notable momentum due to the growing incidence of breast cancer, rapid progress in genomic research, and increasing investments in oncology treatment worldwide. PARP inhibitor biomarkers have become essential in precision medicine as healthcare providers continue focusing on targeted therapies that improve treatment effectiveness and patient outcomes. The industry is also benefiting from advancements in molecular diagnostics, which enable healthcare professionals to identify suitable patients with greater accuracy. Rising awareness regarding early cancer detection and personalized medicine is further supporting demand for biomarker-based testing solutions. In addition, pharmaceutical and diagnostic companies are strengthening research initiatives to develop advanced testing technologies that improve clinical decision-making. Expanding healthcare infrastructure, growing adoption of companion diagnostics, and increasing demand for precision oncology solutions are collectively accelerating market development. The integration of advanced genetic testing into routine clinical workflows, along with increasing acceptance of biomarker-guided therapies, is expected to continue shaping the long-term outlook of the PARP inhibitor biomarkers industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 8.7% |

PARP inhibitor biomarkers are genetic markers that help identify cancer patients who are more likely to benefit from PARP inhibitor therapies. These biomarkers are widely utilized in precision oncology to support targeted treatment strategies and improve therapeutic outcomes. The increasing burden of breast cancer worldwide continues to create strong demand for advanced biomarker testing solutions. Expanding use of molecular profiling and next-generation diagnostic technologies is further contributing to improved patient selection and treatment planning. In addition, the growing emphasis on personalized cancer care is driving the adoption of biomarker-based diagnostics across healthcare systems. Rising spending on cancer therapies and the growing availability of advanced treatment options are also strengthening market expansion. As healthcare providers increasingly prioritize targeted therapies with higher treatment efficiency, the demand for PARP inhibitor biomarkers is expected to rise steadily over the forecast period.

The kits segment is anticipated to reach USD 1.5 billion by 2035, supported by strong demand across hospitals, research facilities, and diagnostic laboratories. The segment continues to gain traction due to its convenience, standardized workflows, and ability to simplify biomarker testing procedures. Ready-to-use testing kits help reduce operational complexity while improving turnaround time and laboratory efficiency. Their broad adoption across clinical environments is also supporting large-scale screening and precision oncology programs. Furthermore, manufacturers are continuously introducing technologically advanced kits designed to deliver improved accuracy, reliability, and workflow compatibility. The increasing availability of automated and user-friendly solutions is further enhancing the position of the kits segment within the PARP inhibitor biomarkers market.

The breast cancer gene (BRCA) 1 & 2 testing segment generated USD 430.7 million in 2025. BRCA testing maintains a leading position in the market because of its critical role in identifying patients eligible for targeted PARP inhibitor therapies. These tests are widely incorporated into clinical oncology practices, particularly for patients diagnosed with breast and ovarian cancers. The growing acceptance of genetic screening programs and favorable clinical recommendations supporting BRCA testing are accelerating segment growth. In addition, rising awareness regarding hereditary cancer risks and increasing access to genetic counseling services are encouraging more individuals to undergo early-stage testing. The increasing focus on precision diagnostics and early treatment intervention is expected to further strengthen demand for BRCA 1 & 2 testing solutions.

North America PARP Inhibitor Biomarkers Market accounted for 40.7% share in 2025. The regional market is experiencing strong growth due to the rising prevalence of breast cancer and increasing adoption of advanced diagnostic technologies. The region records a substantial number of cancer diagnoses each year, creating significant demand for biomarker-driven treatment strategies. Greater awareness regarding cancer screening and early diagnosis programs is also contributing to higher testing volumes across healthcare institutions. Furthermore, the increasing occurrence of hereditary breast cancer cases linked to BRCA mutations is accelerating the adoption of PARP inhibitor biomarker testing. Strong healthcare infrastructure, high healthcare expenditure, and continued advancements in precision oncology are expected to support sustained market expansion across North America.

Prominent companies operating in the Global PARP Inhibitor Biomarkers Market include Agilent Technologies, Thermo Fisher Scientific, Foundation Medicine, Myriad Genetics, Illumina Inc., QIAGEN, Guardant Health, Invitae, Ambry Genetics, EntroGen, Amoy Diagnostics, BPS Bioscience, and Pillar Biosciences. Companies operating in the PARP inhibitor biomarkers market are implementing several strategic initiatives to strengthen their competitive positioning and expand market presence. Leading players are heavily investing in research and development activities to introduce advanced genomic testing technologies with improved sensitivity and accuracy. Strategic collaborations between pharmaceutical companies, diagnostic developers, and healthcare institutions are helping accelerate biomarker discovery and commercialization. Many organizations are also focusing on regulatory approvals and product launches to broaden their diagnostic portfolios and enhance clinical adoption. Expansion into emerging healthcare markets, increased investment in precision oncology infrastructure, and partnerships for companion diagnostic development are further supporting business growth.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Service trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.2.6 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of breast cancer

- 3.2.1.2 Advancements in genomic technologies

- 3.2.1.3 Rising expenditure for cancer treatment

- 3.2.1.4 Growing adoption of personalized medicine and precision therapy

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of PARP inhibitor biomarker test kits and assays

- 3.2.2.2 Limited awareness and understanding of PARP inhibitor biomarkers

- 3.2.3 Market opportunities

- 3.2.3.1 Liquid biopsy & ctDNA-based testing expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.1.1 Expansion of companion diagnostics integration

- 3.5.1.2 Improved multiplex biomarker panels

- 3.5.2 Emerging technologies

- 3.5.2.1 Rise of liquid biopsy and ctDNA testing

- 3.5.2.2 Integration of AI and bioinformatics in genomics

- 3.5.1 Current technological trends

- 3.6 Future market trends (Driven by primary research)

- 3.7 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.8 Pricing trend analysis (Driven by primary research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Kits

- 5.3 Assays

Chapter 6 Market Estimates and Forecast, By Service, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Breast cancer gene (BRCA) 1 & 2 testing

- 6.3 Homologous recombination deficiency (HRD) testing

- 6.4 Homologous recombination repair (HRR) testing

- 6.5 Other services

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Next-generation sequencing

- 7.3 Polymerase Chain Reaction

- 7.4 Immunohistochemistry

- 7.5 In situ hybridization

- 7.6 other technologies

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Breast cancer

- 8.3 Ovarian cancer

- 8.4 Pancreatic cancer

- 8.5 Prostate cancer

- 8.6 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and fertility clinics

- 9.3 Home care

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Agilent Technologies

- 11.2 Ambry Genetics

- 11.3 Amoy Diagnostics

- 11.4 BPS Bioscience

- 11.5 EntroGen

- 11.6 Foundation Medicine

- 11.7 Guardant Health

- 11.8 Illumina Inc.

- 11.9 Invitae

- 11.10 Myriad Genetics

- 11.11 Pillar Biosciences

- 11.12 QIAGEN

- 11.13 Thermo Fisher Scientific