|

시장보고서

상품코드

2061483

자동차용 생성형 AI 시장 기회, 성장 촉진요인, 업계 동향 분석, 예측(2026-2035년)Generative AI in Automotive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

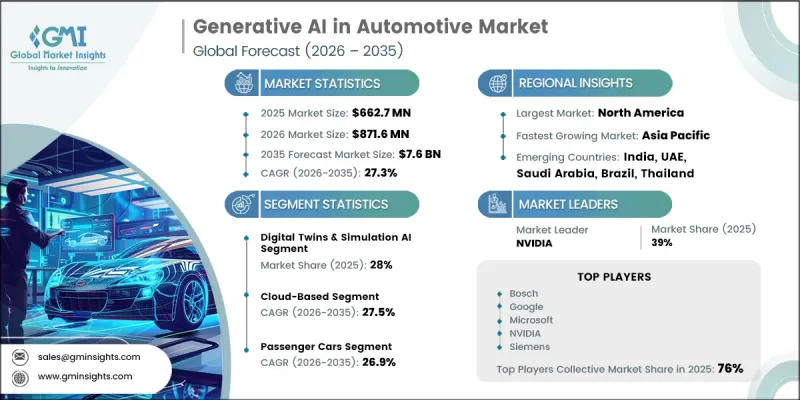

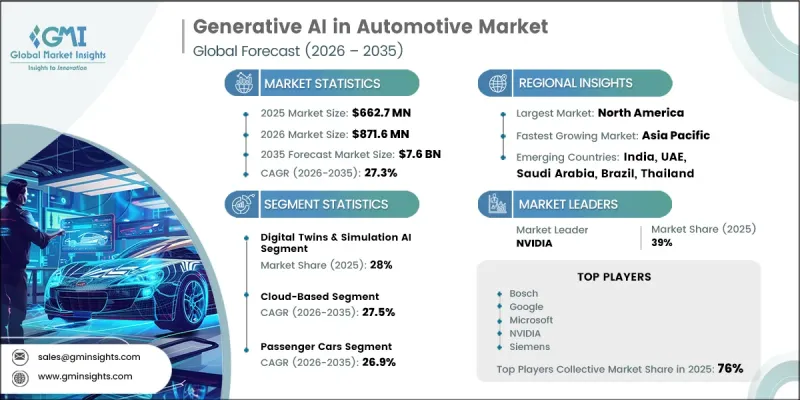

세계의 자동차용 생성형 AI 시장은 2025년에 6억 6,270만 달러로 평가되며, 2035년에는 CAGR 27.3%로 성장하며, 76억 달러에 달할 것으로 예측됩니다.

자동차 업계가 설계, 제조, 진단, 사용자 경험 분야에서 디지털 시스템이 중심적인 역할을 수행하는 ‘소프트웨어 정의 차량(SDV)’ 아키텍처로 점점 더 전환되고 있는 만큼, 해당 시장은 급속히 확대되고 있습니다. 생성형 AI는 소프트웨어 코드 생성, 테스트 워크플로우, 검증 프로세스, 요구사항 정의를 자동화함으로써 큰 진전을 초래하는 동시에, 지속적인 무선 업데이트 기능을 통해 개발 주기를 가속화합니다. 차세대 차량이 점점 더 복잡해짐에 따라 소프트웨어 중심 생태계를 효율적으로 관리하기 위해 AI 기반 솔루션에 대한 의존도가 높아지고 있습니다. 또한 생성형 AI는 드물고 복잡한 주행 시나리오를 재현하는 가상 환경을 생성함으로써 자율주행 모빌리티 개발에 혁신을 가져오고 있으며, 실제 차량 테스트에 대한 의존도를 대폭 줄이고 있습니다. 이를 통해 훈련 효율이 향상되고 모델의 견고성이 강화됩니다. 동시에, 지능형 차량내 경험에 대한 소비자의 기대가 높아짐에 따라 대화형 상호작용, 맞춤형 추천, 스마트 내비게이션, 첨단 인포테인먼트 기능을 구현하는 자연 언어 모델의 도입이 확대되고 있으며, 이러한 요소들이 결합되어 자동차의 콕핏을 디지털 경험의 허브로 탈바꿈시키고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 6억 6,270만 달러 |

| 예측 시장 규모 | 76억 달러 |

| CAGR | 27.3% |

디지털 트윈 및 시뮬레이션 AI 부문은 2025년에 28%의 시장 점유율을 차지하며, 2026-2035년 연평균 성장률(CAGR) 26.6%로 성장할 것으로 전망됩니다. 이 부문은 지속적인 시뮬레이션과 테스트를 가능하게 하기 위해 차량, 생산 시스템 및 주행 환경의 가상 복제본을 만드는 데 중점을 두고 있습니다. 생성형 AI를 활용한 자동차 생태계에서, 이러한 툴들은 자율주행 시스템의 검증, 유지보수 요구사항 예측, 제조 워크플로우 최적화에 폭넓게 활용되고 있습니다. 실기 테스트에 대한 의존도를 낮추면서도 개발 속도와 혁신의 효율성을 높일 수 있는 능력이 도입의 주요 원동력이 되고 있습니다.

클라우드 기반 도입 부문은 2025년에 48.2%의 점유율을 차지하며, 2035년까지 연평균 성장률(CAGR) 27.5%로 성장할 것으로 전망됩니다. 클라우드 인프라를 통해 자동차 제조업체는 대규모 언어 모델, 합성 데이터 엔진, 디지털 트윈 시스템 등 생성형 AI 모델의 훈련 및 배포에 필요한 확장 가능한 컴퓨팅 리소스를 활용할 수 있게 됩니다. 이러한 도입 방식은 시스템의 실시간 업데이트, 엔지니어링 팀 간의 글로벌 협업, 그리고 유연한 비용 구조를 지원합니다. 이는 소프트웨어 정의 자동차 생태계 내에서 자율주행 시뮬레이션 및 차량용 AI 애플리케이션에 널리 활용되고 있습니다.

미국 자동차 업계의 생성형 AI 시장은 2025년에 1억 9,880만 달러에 달하며, 2026-2035년 연평균 성장률(CAGR) 26.1%로 성장할 것으로 전망됩니다. 이 국가는 첨단인 자율주행 개발 프로그램과 자동차 제조사와 기술 기업 간의 강력한 협력을 바탕으로, AI 주도형 모빌리티 분야의 혁신을 이끄는 주요 거점으로 자리매김하고 있습니다. 고성능 컴퓨팅과 AI 플랫폼의 통합을 통해 차세대 모빌리티 솔루션의 시뮬레이션, 훈련 및 도입이 가속화되고 있습니다. 또한 자율주행 시스템을 규제하는 체계 역시 AI 기반 검증 및 테스트 기술의 활용을 촉진하고 있으며, 시장 확대를 더욱 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 기술별, 2022-2035년

제6장 시장 추산·예측 : 용도별, 2022-2035년

제7장 시장 추산·예측 : 차량별, 2022-2035년

제8장 시장 추산·예측 : 배포 모드별, 2022-2035년

제9장 시장 추산·예측 : 최종 사용별, 2022-2035년

제10장 시장 추산·예측 : 지역별, 2022-2035년

제11장 기업 개요

KSAThe Global Generative AI In Automotive Market was valued at USD 662.7 million in 2025 and is estimated to grow at a CAGR of 27.3% to reach USD 7.6 billion in 2035.

The market is experiencing rapid expansion as the automotive industry increasingly shifts toward software-defined vehicle architectures, where digital systems play a central role in design, manufacturing, diagnostics, and user experience. Generative AI enables major advancements by automating software code generation, testing workflows, validation processes, and requirements engineering while also accelerating development cycles through continuous over-the-air update capabilities. The growing complexity of next-generation vehicles is increasing reliance on AI-driven solutions to manage software-intensive ecosystems efficiently. In addition, generative AI is transforming autonomous mobility development by producing synthetic environments that replicate rare and complex driving scenarios, significantly reducing dependency on physical testing. This improves training efficiency and enhances model robustness. At the same time, rising consumer expectations for intelligent in-vehicle experiences are driving adoption of natural language models that enable conversational interaction, personalized recommendations, smart navigation, and advanced infotainment features, collectively reshaping the automotive cockpit into a digital experience hub.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $662.7 Million |

| Forecast Value | $7.6 Billion |

| CAGR | 27.3% |

The digital twins & simulation AI segment held a 28% share in 2025 and is projected to grow at a CAGR of 26.6% from 2026 to 2035. This segment focuses on creating virtual replicas of vehicles, production systems, and driving environments to enable continuous simulation and testing. In the generative AI automotive ecosystem, these tools are widely used for validating autonomous driving systems, forecasting maintenance requirements, and optimizing manufacturing workflows. Their ability to reduce reliance on physical testing while enhancing development speed and innovation efficiency is driving strong adoption.

The cloud-based deployment segment held a 48.2% share in 2025 and is expected to grow at a CAGR of 27.5% through 2035. Cloud infrastructure enables automotive companies to access scalable computing resources for training and deploying generative AI models, including large language models, synthetic data engines, and digital twin systems. This deployment approach supports real-time system updates, global collaboration across engineering teams, and flexible cost structures. It is widely used for autonomous driving simulations and in-vehicle AI applications within software-defined automotive ecosystems.

United States Generative AI In Automotive Market reached USD 198.8 million in 2025 and is projected to grow at a CAGR of 26.1% from 2026 to 2035. The country remains a key hub for innovation in AI-driven mobility, supported by advanced autonomous driving development programs and strong collaboration between automotive and technology companies. The integration of high-performance computing and AI platforms is accelerating simulation, training, and deployment of next-generation mobility solutions. Regulatory frameworks governing autonomous driving systems are also encouraging the use of AI-based validation and testing technologies, further supporting market expansion.

Major companies operating in the Global Generative AI In Automotive Industry include Autodesk, Amazon Web Services, Baidu, Bosch, Google, Microsoft, NVIDIA, PTC, Qualcomm, and Siemens. Companies operating in the generative AI in automotive market are focusing on strengthening their position through heavy investment in AI model development tailored for automotive-grade applications such as autonomous driving, predictive maintenance, and in-vehicle experience systems. They are expanding cloud-native AI platforms to provide scalable computing infrastructure for training and deploying large-scale generative models. Strategic collaborations with automakers, semiconductor firms, and mobility service providers are being prioritized to accelerate ecosystem integration. Firms are also investing in digital twin technologies and simulation environments to improve testing efficiency and reduce development cycles. Another key strategy includes integrating generative AI with edge computing systems to enable real-time vehicle intelligence and decision-making. Companies are further focusing on enhancing data security, model accuracy, and regulatory compliance to support safe deployment in autonomous systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Deployment mode

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Software-defined vehicle adoption growth

- 3.2.1.2 Autonomous driving data demand

- 3.2.1.3 OEM cost optimization pressure

- 3.2.1.4 In-Vehicle AI assistant expansion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Vehicle data privacy concerns

- 3.2.2.2 High AI infrastructure costs

- 3.2.3 Market opportunities

- 3.2.3.1 Generative vehicle design adoption

- 3.2.3.2 Commercial fleet AI expansion

- 3.2.3.3 Emerging market deployment potential

- 3.2.3.4 Cross-industry automotive AI solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Cost breakdown analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 National Institute of Standards and Technology

- 3.6.1.2 Innovation, Science and Economic Development Canada

- 3.6.2 Europe

- 3.6.2.1 European Commission

- 3.6.2.2 European Telecommunications Standards Institute

- 3.6.3 Asia Pacific

- 3.6.3.1 Ministry of Industry and Information Technology

- 3.6.3.2 Ministry of Economy, Trade and Industry

- 3.6.4 Latin America

- 3.6.4.1 Ministry of Science, Technology and Innovation

- 3.6.4.2 National Institute of Statistics and Geography

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Data and Artificial Intelligence Authority

- 3.6.5.2 Department of Communications and Digital Technologies

- 3.6.1 North America

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 Gen AI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.12.1 Base Case - key macro & industry variables driving CAGR

- 3.12.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Million)

- 5.1 Key trends

- 5.2 Large Language Models (LLMs) & NLP

- 5.3 Generative Design & Computer Vision

- 5.4 Synthetic Data Generation

- 5.5 Digital Twins & Simulation AI

- 5.6 AI Agents & Copilots

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Million)

- 6.1 Key trends

- 6.2 Vehicle Design & Engineering

- 6.3 Autonomous Driving & ADAS Development

- 6.4 Manufacturing & Quality Control

- 6.5 Software Development & Testing

- 6.6 In-Vehicle Experience & Customer Interaction

- 6.7 Supply Chain & Procurement

- 6.8 Predictive Maintenance & Diagnostics

Chapter 7 Market Estimates and Forecast, By Vehicle, 2022 - 2035 ($ Million)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedan

- 7.2.2 SUV

- 7.2.3 Hatchback

- 7.3 Commercial Vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates and Forecast, By Deployment Mode, 2022 - 2035 ($ Million)

- 8.1 Key trends

- 8.2 Cloud-Based

- 8.3 On-Premises

- 8.4 Hybrid

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Million)

- 9.1 Key trends

- 9.2 Automotive OEMs

- 9.3 Tier-1 & Tier-2 Suppliers

- 9.4 Automotive Software & Technology Providers

- 9.5 Fleet Operators & Aftermarket Service Providers

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Norway

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Thailand

- 10.4.7 Indonesia

- 10.4.8 Singapore

- 10.4.9 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Autodesk

- 11.1.2 Bosch

- 11.1.3 Google

- 11.1.4 Microsoft

- 11.1.5 Mobileye

- 11.1.6 NVIDIA

- 11.1.7 PTC

- 11.1.8 Qualcomm

- 11.1.9 Siemens

- 11.1.10 Tesla

- 11.2 Regional players

- 11.2.1 Baidu

- 11.2.2 BYD

- 11.2.3 Huawei

- 11.2.4 KPIT Technologies

- 11.2.5 Pony.ai

- 11.2.6 Xpeng

- 11.3 Emerging players

- 11.3.1 Aurora Innovation

- 11.3.2 Waabi

- 11.3.3 Wayve