|

시장보고서

상품코드

2061484

태양광발전 모듈 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Solar PV Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

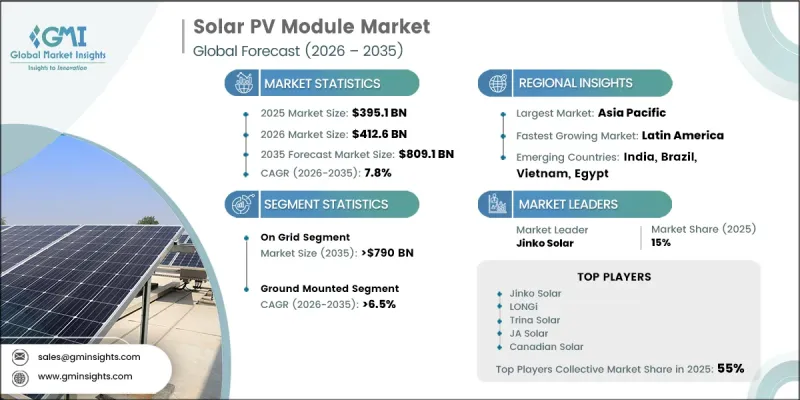

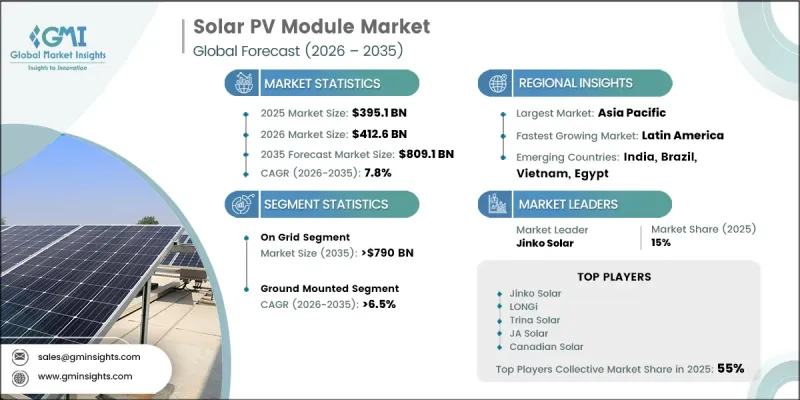

세계의 태양광발전 모듈 시장은 2025년에 3,951억 달러로 평가되고 CAGR 7.8%로 성장하며, 2035년까지 8,091억 달러에 달할 것으로 추정되고 있습니다.

태양광발전 모듈은 주로 실리콘 등의 반도체 재료에 내장된 태양전지를 이용하여, 햇빛을 직접 전기로 변환하도록 설계되어 있습니다. 이러한 모듈은 태양 복사를 포착하여 직류 전기로 변환하는 방식으로 작동하며, 상호 연결된 어레이를 통해 더 대규모의 시스템으로 확장함으로써 다양한 에너지 수요를 충족시킬 수 있습니다. 이 시장은 제조 효율 향상, 기술 혁신, 그리고 설치 방식의 최적화를 통해 이루어지는 기술 비용의 감소에 큰 영향을 받고 있습니다. 계통 연계형 태양광발전 프로젝트에 대한 인센티브, 정책 체계 및 재정 지원 프로그램을 통한 정부의 지원 확대는 투자 매력을 한층 더 높이고 있습니다. 기후 변화에 대한 전 세계의 인식이 높아지고, 온실가스 배출 감축의 시급성에 대한 이해도 깊어짐에 따라 재생에너지로의 전환이 가속화되고 있습니다. 또한 기업, 정부, 일반 가정이 지속가능성 전략에 태양광발전 솔루션을 도입하는 움직임이 확대되고 있으며, 이는 수요를 더욱 끌어올려 장기적인 시장 성장을 지원하고 있습니다. 보다 청정한 에너지 시스템으로의 지속적인 전환과 이를 지원하는 규제 환경 덕분에, 전 세계 태양광발전 도입이 강력한 성장세를 유지할 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 3,951억 달러 |

| 예측액 | 8,091억 달러 |

| CAGR | 7.8% |

계통 연계형 부문은 에너지 출력과 시스템 성능을 향상시키는 단결정 및 양면 수광 기술의 발전을 포함한 태양광 모듈 효율의 지속적인 개선에 힘입어, 2035년까지 7,900억 달러에 달할 것으로 전망됩니다. 보조금, 세제 혜택, 리베이트 프로그램 등 지원 정책 체계를 통해 많은 지역에서 계통 연계형 태양광발전 시스템의 보급이 촉진되고 있습니다. 주요 경제권에서 체계적인 인센티브 제도를 확충함에 따라 계통 연계형 태양광발전 인프라 도입이 더욱 가속화되고 있습니다.

지상 설치형 태양광발전 부문은 2035년까지 연평균 성장률(CAGR) 6.5%로 성장할 것으로 예상됩니다. 설치 면적당 발전량 증가를 가능하게 하는 단결정 및 양면 패널을 포함한 고효율 태양광발전 기술의 발전이 도입 확대를 지원하고 있습니다. 박막 태양광발전 기술의 개선 또한 그 경량 구조와 유연성 덕분에 대규모 설치에 적합하므로 도입 확대에 기여하고 있습니다.

미국의 태양광 모듈 시장은 2035년까지 570억 달러에 달할 것으로 전망됩니다. 2025년 현재 북미는 세계 시장 점유율의 9.4%를 차지하고 있으며, 이는 수입 의존에서 국내 생산 능력 확대로의 구조적 전환을 반영하고 있습니다. 정책 지원 조치에 힘입어 생산 능력 확대가 크게 가속화되면서, 지역 태양광발전 제조 생태계가 강화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모·예측 : 기술별, 2022-2035년

제6장 시장 규모·예측 : 제품별, 2022-2035년

제7장 시장 규모·예측 : 접속성별, 2021-2034년

제8장 시장 규모·예측 : 설치 방식별, 2022-2035년

제9장 시장 규모·예측 : 최종 사용별, 2022-2035년

제10장 시장 규모·예측 : 지역별, 2022-2035년

제11장 기업 개요

KSA 26.06.24The Global Solar PV Module Market was valued at USD 395.1 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 809.1 billion by 2035.

Solar PV modules are designed to convert sunlight directly into electricity using photovoltaic cells embedded within semiconductor-based materials, primarily silicon. These modules function by capturing solar radiation and converting it into direct current electricity, which can then be scaled into larger systems through interconnected arrays to meet diverse energy requirements. The market is strongly influenced by falling technology costs driven by manufacturing efficiency improvements, technological innovation, and optimized installation methods. Expanding government support through incentives, policy frameworks, and financial assistance programs for grid-connected solar projects is further strengthening investment attractiveness. Increasing global awareness of climate change and the urgent need to reduce greenhouse gas emissions is also accelerating the shift toward renewable energy adoption. In addition, corporations, governments, and households are increasingly integrating solar solutions into their sustainability strategies, further boosting demand and supporting long-term market expansion. The continuous transition toward cleaner energy systems and supportive regulatory environments is expected to sustain strong growth momentum across global solar PV deployments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $395.1 Billion |

| Forecast Value | $809.1 Billion |

| CAGR | 7.8% |

The on-grid segment is projected to reach USD 790 billion by 2035, driven by continuous improvements in solar module efficiency, including advancements in monocrystalline and bifacial technologies that enhance energy output and system performance. Supportive policy frameworks, including subsidies, tax benefits, and rebate programs, are encouraging widespread adoption of grid-connected solar systems across multiple regions. The expansion of structured incentive mechanisms across major economies is further strengthening the deployment of on-grid solar infrastructure.

The ground-mounted solar segment is expected to grow at a CAGR of 6.5% through 2035. Rising deployment is supported by advancements in high-efficiency photovoltaic technologies, including monocrystalline and bifacial panels, which enable higher energy output per installation area. Improvements in thin-film photovoltaic technology are also contributing to increased adoption due to their lightweight structure and flexibility, making them suitable for large-scale installations.

U.S. Solar PV Module Market is projected to reach USD 57 billion by 2035. North America accounted for 9.4% of the global market share in 2025, reflecting a structural shift from import reliance toward expanding domestic manufacturing capabilities. Policy support mechanisms have significantly accelerated production capacity growth, strengthening the regional solar manufacturing ecosystem.

Major companies operating in the Global Solar PV Module Industry include Jinko Solar, Trina Solar, Canadian Solar, First Solar, LONGi, JA Solar Technology, Hanwha Group, Risen Energy, REC Group, SunPower Corporation, Vikram Solar, Adani Solar, Tongwei Solar, Yingli Energy, Waaree Energies, DAS Solar, Emmvee Solar, GCL-SI, Aiko Solar Technology, CsunSolarTech, Huasan Energy, Renesola, Solaria Corporation, and SunPower Corporation. Companies operating in the Solar PV Module Market are actively adopting diversified strategies to strengthen their global competitiveness and market presence. Industry participants are investing heavily in advanced photovoltaic technologies to improve conversion efficiency, durability, and overall system performance. Expansion of large-scale manufacturing capacities is being prioritized to achieve cost advantages and meet rising global demand. Strategic partnerships with energy developers, utilities, and government-backed projects are helping companies expand distribution networks and project pipelines. Firms are also focusing on vertical integration to enhance supply chain control and reduce production costs. Continuous research and development efforts are enabling innovation in next-generation solar technologies, including high-efficiency cell architectures and lightweight module designs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Product trends

- 2.5 Mounting trends

- 2.6 Connectivity trends

- 2.7 End Use trends

- 2.8 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw Material Suppliers

- 3.1.2 Component Manufacturers

- 3.1.3 Module Manufacturers

- 3.1.4 Distributors & System Integrators

- 3.1.5 End Users & Project Developers

- 3.2 Regulatory landscape

- 3.2.1 Global Policy & Incentive Programs

- 3.2.2 Net Metering & Feed-in Tariff Mechanisms

- 3.2.3 Carbon Credit & Renewable Energy Certification Standards

- 3.2.4 Trade Policies & Anti-Dumping Regulations

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.7.1 Bill of Materials Breakdown

- 3.7.2 Manufacturing Cost Evolution & Learning Curve

- 3.7.3 Balance of System Cost Trends

- 3.8 Price trend analysis (Driven by Primary Research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy by player type

- 3.9 Trade data analysis (Driven by Primary Research)

- 3.9.1 Import/export value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Production capacity & utilization (Driven by Primary Research)

- 3.10.1 Production capacity by country

- 3.10.2 Utilization rates and expansion pipeline

- 3.11 Impact of AI & generative AI on the market [SOLUTION CORE]

- 3.11.1 Predictive maintenance & fault detection

- 3.11.2 Grid optimization & load forecasting

- 3.11.3 Digital twin simulation & testing

- 3.11.4 Risks, limitations & regulatory considerations

- 3.12 Emerging opportunities & trends

- 3.13 Digitalization & IoT integration

- 3.14 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Billion & MW)

- 5.1 Key trends

- 5.2 Thin Film

- 5.2.1 Cadmium Telluride

- 5.2.2 Amorphous Silicon

- 5.2.3 Copper Indium Gallium Diselenide

- 5.3 Crystalline Silicon

Chapter 6 Market Size and Forecast, By Product, 2022 - 2035 (USD Billion & MW)

- 6.1 Key trends

- 6.2 Monocrystalline

- 6.2.1 PERC

- 6.2.2 TopCon

- 6.2.3 HJT

- 6.2.4 IBC/TBC

- 6.3 Polycrystalline

Chapter 7 Market Size and Forecast, By Connectivity, 2021 - 2034 (USD Billion & MW)

- 7.1 Key trends

- 7.2 On Grid

- 7.3 Off Grid

Chapter 8 Market Size and Forecast, By Mounting, 2022 - 2035 (USD Billion & MW)

- 8.1 Key trends

- 8.2 Ground Mounted

- 8.3 Roof Top

Chapter 9 Market Size and Forecast, By End Use, 2022 - 2035 (USD Billion & MW)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial & Industrial

- 9.4 Utility

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion & MW)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Austria

- 10.3.2 Norway

- 10.3.3 Denmark

- 10.3.4 Finland

- 10.3.5 France

- 10.3.6 Germany

- 10.3.7 Italy

- 10.3.8 Switzerland

- 10.3.9 Spain

- 10.3.10 Sweden

- 10.3.11 UK

- 10.3.12 Netherlands

- 10.3.13 Poland

- 10.3.14 Belgium

- 10.3.15 Ireland

- 10.3.16 Baltics

- 10.3.17 Portugal

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Australia

- 10.4.3 India

- 10.4.4 Japan

- 10.4.5 South Korea

- 10.4.6 Thailand

- 10.4.7 Philippines

- 10.4.8 Vietnam

- 10.4.9 Malaysia

- 10.4.10 Singapore

- 10.5 Middle East

- 10.5.1 Israel

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

- 10.5.4 Jordan

- 10.5.5 Oman

- 10.5.6 Kuwait

- 10.5.7 Turkey

- 10.6 Africa

- 10.6.1 South Africa

- 10.6.2 Egypt

- 10.6.3 Algeria

- 10.6.4 Nigeria

- 10.6.5 Morocco

- 10.7 Latin America

- 10.7.1 Brazil

- 10.7.2 Chile

- 10.7.3 Argentina

- 10.7.4 Peru

Chapter 11 Company Profiles

- 11.1 Aiko Solar Technology

- 11.2 Adani Solar

- 11.3 CsunSolarTech

- 11.4 Canadian Solar

- 11.5 DAS Solar

- 11.6 Emmvee Solar

- 11.7 First Solar

- 11.8 GCL-SI

- 11.9 Huasan Energy

- 11.10 Hanwha Group

- 11.11 Jinko Solar

- 11.12 JA SOLAR Technology

- 11.13 LONGi

- 11.14 RENESOLA

- 11.15 Risen Energy

- 11.16 REC Solar Holdings

- 11.17 SunPower Corporation

- 11.18 Solaria Corporation

- 11.19 Trina Solar

- 11.20 Tongwei Solar

- 11.21 Vikram Solar

- 11.22 Waaree Energies

- 11.23 Yingli Energy