|

시장보고서

상품코드

2061486

수의용 자가면역질환 치료제 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Veterinary Autoimmune Disease Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

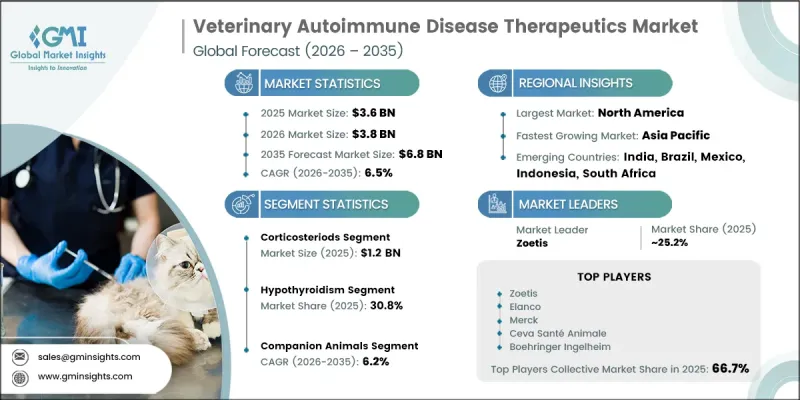

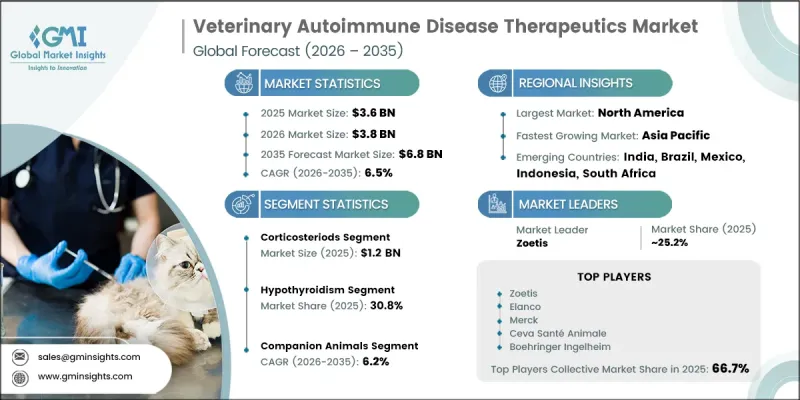

세계의 수의용 자가면역질환 치료제 시장은 2025년에 36억 달러로 평가되고 CAGR 6.5%로 성장하며, 2035년까지 68억 달러에 달할 것으로 추정되고 있습니다.

시장 성장은 전 세계에서 반려동물 사육이 증가하는 데 더해, 동물에서 자가면역 질환의 발생률이 높아짐에 따라 주도되고 있습니다. 수의학용 자가면역질환 치료제는 면역계가 건강한 조직을 잘못 공격하여 장기적인 의료적 개입이 필요한 질환의 관리에 중점을 두고 있습니다. 치료법으로는 주로 면역억제제, 코르티코스테로이드 계열 치료법, 그리고 면역매개성 빈혈, 루푸스, 천포창 등의 질환을 조절하기 위해 개발된 생물제제가 포함됩니다. 반려동물의 ‘인간화’ 추세가 강화됨에 따라 고도로 전문적인 수의학 솔루션에 대한 수요가 크게 증가하고 있습니다. 동시에, 제약회사와 연구기관은 혁신적인 치료법에 대한 접근성을 확대하고 치료 성과를 향상시키기 위해 협력을 더욱 강화하고 있습니다. 표적형 바이오로직스와 단일클론 항체 연구의 진전은 이 분야의 치료법 혁신을 더욱 가속화하고 있습니다. 또한 환경을 고려한 보다 안전한 제제에 대한 관심이 높아지는 가운데, 시장에서는 자연 유래이며 지속가능한 치료법으로의 전환이 서서히 진행되고 있습니다. 규제 체계의 강화와 연구 투자 확대를 통해 제품 개발 주기의 단축이 촉진되고 있습니다. 또한 특정 견종이나 질환에 특화된 치료법에 대한 수요가 증가함에 따라 전 세계 시장에서 더욱 개인화된 수의학적 접근 방식의 개발이 촉진되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 36억 달러 |

| 예측액 | 68억 달러 |

| CAGR | 6.5% |

코르티코스테로이드 시장은 2025년에 12억 달러에 달하며, 2035년까지 22억 달러에 달할 것으로 전망되어 연평균 성장률(CAGR)은 6.4%를 기록할 것으로 보입니다. 이 부문의 경쟁력은 신속한 치료 효과, 높은 비용 대비 효과, 그리고 동물의 다양한 자가면역 질환에 대한 폭넓은 적용 가능성 덕분에 지원되고 있습니다. 코르티코스테로이드를 기반으로 한 치료법은 면역 과반응을 신속하게 억제하고 염증을 완화하는 효과가 있으며, 수의학 분야에서 여전히 기본적인 치료 옵션으로 자리 잡고 있습니다. 이러한 치료법은 면역 조절이 질환 관리에 필수적인 면역 매개성 관절염, 자가면역성 빈혈, 내분비 관련 면역 기능 장애 등의 질환 관리에 널리 사용되고 있습니다.

갑상선 기능 저하증 부문은 2025년에 30.8%의 시장 점유율을 차지하며, 반려동물에서 치료되는 가장 흔한 자가면역 질환 중 하나가 되고 있습니다. 이 질환은 특히 개에게서 흔히 나타나며, 면역 기능의 이상으로 인해 정상적인 갑상선 기능이 저해되고 호르몬 분비가 감소함으로써 발병합니다. 이 질병에 걸린 동물에서는 피로, 체중 증가, 피부 증상 등의 증상이 자주 관찰됩니다. 이러한 높은 발병률을 배경으로, 호르몬 균형을 회복시키고 반려동물의 장기적인 건강 상태를 개선하는 것을 목적으로 한 표적 치료법 개발이 진행되고 있습니다.

북미의 수의학용 자가면역질환 치료제 시장은 2025년에 42.3%의 점유율을 기록했습니다. 이 지역의 경쟁력은 높은 반려동물 보유율, 잘 갖춰진 의료 시스템, 그리고 동물 자가면역 질환에 대한 의식의 향상 등에 힘입어 지원되고 있습니다. 특히 개와 고양이를 중심으로 한 반려동물의 수가 엄청나게 늘어나면서, 루푸스나 면역매개성 용혈성 빈혈 등의 질환 진단률이 높아지고 있습니다. 지역 전체에 걸쳐 있는 첨단 동물병원과 진료소 덕분에 조기 발견과 효과적인 질환 관리가 가능해졌습니다. 또한 반려동물 보험의 보급 확대와 맞춤형 수의학적 접근 방식의 도입 증가가 시장의 추가적인 성장을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 요법 유형별, 2022-2035년

제6장 시장 추산·예측 : 질환별, 2022-2035년

제7장 시장 추산·예측 : 동물 유형별, 2022-2035년

제8장 시장 추산·예측 : 투여 경로별, 2022-2035년

제9장 시장 추산·예측 : 유통 채널별, 2022-2035년

제10장 시장 추산·예측 : 지역별, 2022-2035년

제11장 기업 개요

KSA 26.06.24The Global Veterinary Autoimmune Disease Therapeutics Market was valued at USD 3.6 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 6.8 billion by 2035.

Market growth is driven by the rising incidence of autoimmune conditions in animals alongside increasing global adoption of companion pets. Veterinary autoimmune disease therapeutics focus on managing disorders in which the immune system mistakenly attacks healthy tissues, requiring long-term medical intervention. Treatment options primarily include immunosuppressive agents, corticosteroid-based therapies, and biologics designed to control conditions such as immune-mediated anemia, lupus, and pemphigus. Growing pet humanization trends are significantly increasing demand for advanced and specialized veterinary care solutions. At the same time, pharmaceutical companies and research organizations are increasingly collaborating to expand access to innovative therapies and improve treatment outcomes. Advancements in targeted biologics and monoclonal antibody research are further accelerating therapeutic innovation in this space. The market is also experiencing a gradual shift toward natural and sustainable treatment alternatives, driven by rising preference for eco-conscious and safer formulations. Strengthened regulatory frameworks and higher research investments are supporting faster product development cycles. Additionally, increasing demand for breed-specific and condition-specific therapies is encouraging the development of more personalized veterinary treatment approaches across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.6 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 6.5% |

The corticosteroids segment reached USD 1.2 billion in 2025 and is expected to reach USD 2.2 billion by 2035, growing at a CAGR of 6.4%. This segment's dominance is supported by its rapid therapeutic action, cost-effectiveness, and broad applicability across multiple autoimmune conditions in animals. Corticosteroid-based treatments remain a foundational option in veterinary care due to their ability to quickly suppress immune overactivity and reduce inflammation. These therapies are widely used in managing disorders such as immune-mediated arthritis, autoimmune anemia, and endocrine-related immune dysfunctions, where immune modulation is critical for disease control.

The hypothyroidism segment accounted for 30.8% share in 2025, making it one of the most prevalent autoimmune conditions treated in companion animals. This disorder is especially common in dogs and occurs when immune dysfunction disrupts normal thyroid activity, leading to reduced hormone production. Symptoms such as fatigue, weight gain, and dermatological complications are frequently observed in affected animals. The high occurrence rate has encouraged the development of targeted therapeutic approaches aimed at restoring hormonal balance and improving long-term health outcomes in pets.

North America Veterinary Autoimmune Disease Therapeutics Market held a 42.3% share in 2025. The region's dominance is supported by high pet ownership rates, a well-developed veterinary healthcare system, and increasing awareness of autoimmune disorders in animals. The large population of companion animals, particularly dogs and cats, contributes to higher diagnosis rates for conditions such as lupus and immune-mediated hemolytic anemia. Advanced veterinary clinics and hospitals across the region enable early detection and effective disease management. In addition, the growing penetration of pet insurance and the rising adoption of personalized veterinary care approaches are further supporting market expansion.

Key companies operating in the Global Veterinary Autoimmune Disease Therapeutics Market include Zoetis, Elanco, Merck Animal Health, Boehringer Ingelheim, Virbac, Dechra Pharmaceuticals, Vetoquinol, Ceva Sante Animale, Animalcare Group, Norbrook, Bimeda, and Dopharma. Companies in the veterinary autoimmune disease therapeutics market are focusing on expanding their product portfolios through the development of advanced immunomodulatory therapies that offer improved safety and efficacy profiles. A key strategy involves strengthening research and development capabilities to accelerate the introduction of targeted biologics and next-generation monoclonal antibody treatments. Firms are also pursuing strategic collaborations with veterinary research institutes and academic organizations to enhance clinical innovation and improve disease understanding. Geographic expansion into emerging pet care markets is being prioritized to capture rising demand for specialized veterinary services. Companies are further investing in sustainable and natural formulation development to align with changing consumer preferences for eco-friendly products. Strengthening distribution networks and expanding partnerships with veterinary clinics and hospitals are also central to improving product accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Therapy type trends

- 2.2.3 Disease trends

- 2.2.4 Animal type trends

- 2.2.5 Route of administration trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing threat of transfer of zoonotic diseases among humans

- 3.2.1.2 Rising incidence of autoimmune diseases in livestock animals

- 3.2.1.3 Increasing awareness and diagnosis of autoimmune diseases

- 3.2.1.4 Growing companion animal ownership

- 3.2.1.5 Increasing expenditure on animal healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of veterinary autoimmune therapies

- 3.2.2.2 Increase risk of infection due to autoimmune drugs

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for breed-specific and personalized treatments

- 3.2.3.2 Growth in telemedicine and remote veterinary diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technology

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.6 Regulatory landscape (Driven by primary research)

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends (Driven by primary research)

- 3.10 Impact of AI and generative AI on the market (Driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Therapy Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Corticosteroids

- 5.3 Azathioprine

- 5.4 Cyclosporine

- 5.5 Mycophenolate

- 5.6 Leflunomide

- 5.7 Cyclophosphamide

- 5.8 Levothyroxine

- 5.9 Folic acid

- 5.10 Hydroxychloroquine

- 5.11 Chloroquine

Chapter 6 Market Estimates and Forecast, By Disease, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hypothyroidism

- 6.3 Pemphigus disease

- 6.4 Canine lupus

- 6.5 Autoimmune haemolytic anaemia

- 6.6 Bullous pemphigoid

- 6.7 Discoid lupus erythematosus (DLE)

- 6.8 Immune-related arthritis

- 6.9 Other diseases

Chapter 7 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Companion animals

- 7.2.1 Dogs

- 7.2.2 Cats

- 7.2.3 Horses

- 7.2.4 Other companion animals

- 7.3 Livestock animals

- 7.3.1 Cattle

- 7.3.2 Swine

- 7.3.3 Poultry

- 7.3.4 Sheep

- 7.3.5 Other livestock animals

- 7.4 Other animals

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Injectable

- 8.4 Topical

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospitals

- 9.3 Veterinary clinics

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Animalcare group

- 11.2 Bimeda

- 11.3 Boehringer Ingelheim

- 11.4 Ceva Sante Animal

- 11.5 Dechra Pharmaceuticals

- 11.6 Dopharma

- 11.7 Elanco

- 11.8 Merck Animal Health

- 11.9 Norbrook

- 11.10 Vetoquinol

- 11.11 Virbac

- 11.12 Zoetis