|

시장보고서

상품코드

2071161

양방향 전기자동차 충전 시장 : 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Bidirectional EV Charging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

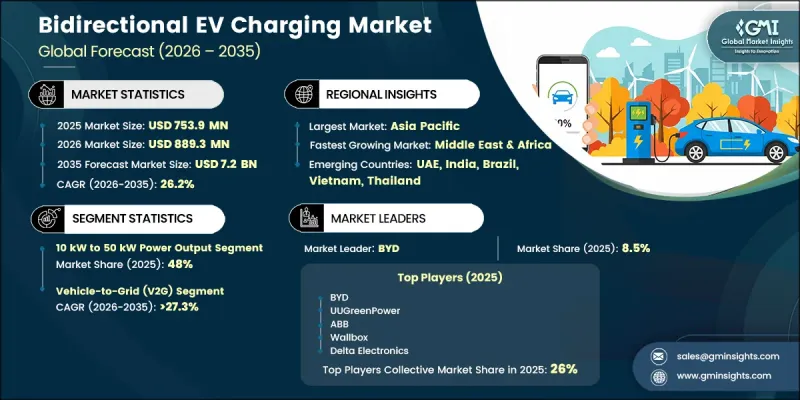

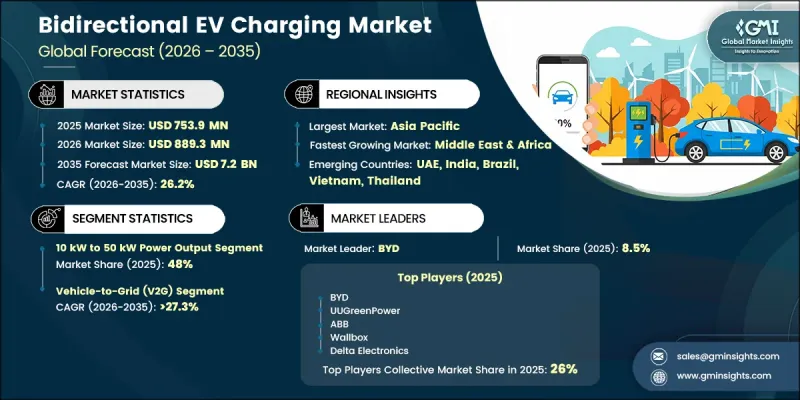

세계의 양방향 전기자동차 충전 시장은 2025년에 7억 5,390만 달러 규모가 되어, 2035년까지 연평균 복합 성장률(CAGR) 26.2%로 성장하여 72억 달러에 이를 것으로 추정되고 있습니다.

양방향 전기자동차 충전 업계 전반의 성장은 전기자동차의 급속한 보급, 상업용 운송 차량의 전기화 확대, 그리고 더욱 탄력적이고 유연한 에너지 시스템에 대한 수요 증가에 힘입어 이루어지고 있습니다. 전력망에 재생에너지원을 통합하는 움직임이 확대됨에 따라, 에너지 공급과 소비의 균형을 조절할 수 있는 기술에 대한 수요가 더욱 높아지고 있습니다. 동시에, 주요 경제권에서 시행되고 있는 지원적인 규제 조치와 탈탄소화 목표가 첨단 충전 인프라에 대한 투자를 가속화하고 있습니다. V2G(Vehicle-to-Grid) 지원 하드웨어, 지능형 에너지 관리 플랫폼, 그리고 분산형 에너지 자원에 대한 관심이 높아지면서, 전기자동차 충전 시스템은 현대 전력망에서 능동적인 역할을 수행하는 존재로 변모하고 있습니다. 상용 차량 플릿 사업자는 다수의 연결된 차량을 통합하여 에너지 관련 서비스를 제공할 수 있기 때문에 큰 성장 기회를 가지고 있습니다. 또한, 전기자동차 소유자들이 주택의 에너지 관리를 개선할 수 있는 솔루션을 점점 더 많이 찾으면서, 주택에서의 도입도 확대되고 있습니다. 에너지 시스템이 지속적으로 발전함에 따라, 양방향 충전 기술은 보다 지속 가능하고 효율적인 에너지 생태계로의 광범위한 전환 과정에서 중요한 요소로 부상하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 7억 5,390만 달러 |

| 예측 금액 | 72억 달러 |

| CAGR | 26.2% |

2025년에는 출력 10kW-50kW 구간이 시장 점유율의 48%를 차지하고, 2035년까지 연평균 성장률(CAGR) 24.6%로 성장할 것으로 전망됩니다. 이 부문은 일반적인 가정용 설비보다 높은 충전 요구 사항을 충족하는 다양한 상업용 및 준상업용 용도에 대응하면서도, 대용량 충전 인프라보다 비용 효율성이 뛰어납니다. 이 부문은 차량 운용, 직장 내 충전 환경, 기타 중용량 에너지 관리 용도에 대응할 수 있는 확장성이 뛰어난 충전 솔루션을 필요로 하는 조직들 수요가 확대됨에 따라 계속해서 혜택을 보고 있습니다.

V2G(Vehicle-to-Grid) 부문은 2025년에 36%의 시장 점유율을 차지했습니다. 이러한 강력한 성장은 그리드 지원 프로그램 참여 확대, 에너지 관리 전략에 대한 전기자동차의 보다 광범위한 통합, 그리고 유연한 에너지 자원 수요 증가에 힘입어 이루어지고 있습니다. 전력 회사와 에너지 공급 사업자들이 전력 시스템의 현대화를 추진하는 가운데, V2G 기술은 전력망의 안정성을 높이고 에너지 효율을 개선하며, 장기적인 재생에너지 통합 목표를 뒷받침하는 효과적인 해결책으로 인식되고 있습니다.

북미의 양방향 전기자동차 충전 시장은 2025년에 22%의 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 25.6%로 성장할 것으로 전망됩니다. 이 지역의 성장은 첨단 충전 인프라에 대한 투자 확대, 유리한 정책 체계, 전기화 이니셔티브의 확대, 그리고 지능형 에너지 관리 시스템의 도입 확대에 힘입어 이루어지고 있습니다. 에너지 네트워크의 현대화와 전기자동차 보급을 지원하기 위한 지속적인 노력으로 인해, 북미 전역에서 시장 확대를 위한 큰 기회가 창출될 것으로 전망됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 충전기별, 2022-2035년

제6장 시장 추산 및 예측 : 출력별, 2022-2035년

제7장 시장 추산 및 예측 : 차량별, 2022-2035년

제8장 시장 추산 및 예측 : 용도별, 2022-2035년

제9장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제10장 시장 추산 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

JHS 26.07.01The Global Bidirectional EV Charging Market was valued at USD 753.9 million in 2025 and is estimated to grow at a CAGR of 26.2% to reach USD 7.2 billion by 2035.

Growth across the bidirectional EV charging industry is fueled by the rapid adoption of electric vehicles, expanding electrification of commercial transportation fleets, and increasing demand for more resilient and flexible energy systems. Rising integration of renewable energy sources into power networks is creating additional demand for technologies capable of balancing energy supply and consumption. At the same time, supportive regulatory initiatives and decarbonization objectives across major economies are accelerating investment in advanced charging infrastructure. The combination of vehicle-to-grid capable hardware, intelligent energy management platforms, and growing interest in distributed energy resources is transforming EV charging systems into active participants within modern electricity networks. Commercial fleet operators represent a significant growth opportunity due to their ability to aggregate large numbers of connected vehicles and provide energy-related services. Residential adoption is also expanding as electric vehicle owners increasingly seek solutions that improve household energy management. As energy systems continue to evolve, bidirectional charging technology is emerging as a critical component of the broader transition toward a more sustainable and efficient energy ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $753.9 Million |

| Forecast Value | $7.2 Billion |

| CAGR | 26.2% |

The 10 kW to 50 kW power output category accounted for 48% share in 2025 and is projected to grow at a CAGR of 24.6% through 2035. This segment serves a wide range of commercial and semi-commercial applications where charging requirements exceed those typically associated with residential installations, while remaining more cost-effective than high-capacity charging infrastructure. The segment continues to benefit from growing demand among organizations seeking scalable charging solutions capable of supporting fleet operations, workplace charging environments, and other medium-capacity energy management applications.

The vehicle-to-grid (V2G) segment held a 36% share in 2025. Strong growth is driven by increasing participation in grid-support programs, broader integration of electric vehicles into energy management strategies, and rising demand for flexible energy resources. As utilities and energy providers continue to modernize power systems, V2G technology is gaining recognition as an effective solution for enhancing grid stability, improving energy efficiency, and supporting long-term renewable energy integration objectives.

North America Bidirectional EV Charging Market captured 22% share in 2025 and is forecast to grow at a CAGR of 25.6% through 2035. Regional growth is supported by increasing investments in advanced charging infrastructure, favorable policy frameworks, expanding electrification initiatives, and growing deployment of intelligent energy management systems. Continued efforts to modernize energy networks and support electric vehicle adoption are expected to create substantial opportunities for market expansion across North America.

Key participants operating in the Global Bidirectional EV Charging Market include Nuvve Corporation, ABB, ChargePoint, Delta Electronics, Eaton, Schneider Electric, UUGreenPower, Tesla Energy, Kaluza, PowerFlex, Siemens, Fermata Energy, BYD, Nissan Motor, Indra Renewable, Ohme, and Kia. Companies competing in the bidirectional EV charging market are implementing a range of strategies to strengthen their market position and expand their global footprint. Leading organizations are investing heavily in research and development to enhance charging efficiency, improve interoperability, and advance energy management capabilities. Strategic partnerships with utilities, automotive manufacturers, energy providers, and technology firms are enabling companies to accelerate deployment and broaden market access. Market participants are also focusing on expanding product portfolios, strengthening software capabilities, and developing integrated charging ecosystems that support grid interaction and distributed energy management. In addition, firms are pursuing geographic expansion, regulatory compliance initiatives, and investments in smart charging infrastructure to capitalize on emerging opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Charger

- 2.2.2 Power Output

- 2.2.3 Vehicle

- 2.2.4 Application

- 2.2.5 End-Use

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Component & Electronics Manufacturers

- 3.1.1.2 Charging & Energy Specialists

- 3.1.1.3 Automotive OEMs

- 3.1.1.4 Distributors

- 3.1.1.5 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV Adoption & Fleet Expansion

- 3.2.1.2 Smart Grid & Energy Management Needs

- 3.2.1.3 Technological Advancements

- 3.2.1.4 Government Policies & Incentives

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Infrastructure & Implementation Costs

- 3.2.2.2 Regulatory & Standardization Gaps

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with Renewable Energy & Home Energy Systems

- 3.2.3.2 Fleet & Commercial Applications

- 3.2.3.3 Rapid technological investments by prominent players.

- 3.2.3.4 Advancements in Vehicle-to-Grid (V2G) technology.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 US: IEEE 2030.5 / SAE J3072 (Grid Interconnection)

- 3.5.1.2 Canada: UL 9741 (Bidirectional Charging Equipment)

- 3.5.2 Europe

- 3.5.2.1 Germany: Grid Connection Codes (ENTSO-E / National Grids)

- 3.5.2.2 France: ISO 15118-2 (Plug & Charge + V2G Communication)

- 3.5.2.3 UK: G98 / G99 Standards

- 3.5.2.4 Italy: DSO Approval & Interconnection

- 3.5.3 Asia-Pacific

- 3.5.3.1 China GB/T 27930 (Reverse Flow Protocol)

- 3.5.3.2 JIS G 3306 (Japan V2G Grid Integration)

- 3.5.3.3 South Korea: KC safety certification and ISO protocol conformance

- 3.5.3.4 India: Central Electricity Authority (CEA)

- 3.5.4 Latin America

- 3.5.4.1 ANEEL (Brazil) Distributed Generation Resolution

- 3.5.4.2 CFE (Mexico) Grid Interconnection Permit

- 3.5.5 Middle East & Africa

- 3.5.5.1 DEWA (Dubai) V2G Pilot Framework

- 3.5.5.2 ESKOM NRS 097-2-3 (South Africa)

- 3.5.1 North America

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 Automated design optimization

- 3.10.3 Supply chain AI for demand forecasting

- 3.10.4 GenAI use cases & adoption roadmap by segment

- 3.10.5 Risks, Limitations & Regulatory Considerations

- 3.11 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.11.1 Base Case - key macro & industry variables driving CAGR

- 3.11.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.11.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

- 4.5 Company tier benchmarking

- 4.5.1 Tier classification criteria & qualifying thresholds

- 4.5.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Charger, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 AC Bidirectional Charger

- 5.3 DC Bidirectional Charger

Chapter 6 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Below 10 kW

- 6.3 10 kW to 50 kW

- 6.4 Above 50 kW

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 SUV

- 7.2.2 Sedan

- 7.2.3 Hatchback

- 7.3 Commercial Vehicle

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

- 7.4 Two & Three Wheelers

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Vehicle-to-Grid (V2G)

- 8.3 Vehicle-to-Home (V2H)

- 8.4 Vehicle-to-Building (V2B)

- 8.5 Vehicle-to-Load (V2L)

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Residential

- 9.2.1 Single-Family Homes

- 9.2.2 Apartment Complexes

- 9.3 Commercial

- 9.3.1 Corporate Campuses

- 9.3.2 Hospitality

- 9.3.3 Retail

- 9.4 Industrial

- 9.4.1 Manufacturing Facilities & Warehouses

- 9.4.2 Logistics & Distribution Centers

- 9.4.3 Utilities & Grid Operators

- 9.4.4 Others

- 9.5 Public sector & emergency services

- 9.5.1 Government Offices

- 9.5.2 School & Colleges

- 9.5.3 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.3.9 Thailand

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

- 10.5.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 ABB

- 11.1.2 ChargePoint

- 11.1.3 Delta Electronics

- 11.1.4 Eaton

- 11.1.5 Nissan Motor

- 11.1.6 Nuvve

- 11.1.7 Schneider Electric

- 11.1.8 Siemens

- 11.1.9 Tesla Energy

- 11.1.10 Wallbox Chargers

- 11.2 Regional players

- 11.2.1 BYD Company

- 11.2.2 Fermata Energy

- 11.2.3 Kia Motors

- 11.2.4 Ohme

- 11.2.5 PowerFlex

- 11.2.6 V2Green

- 11.2.7 Virta

- 11.3 Emerging players

- 11.3.1 evGateway

- 11.3.2 Indra Renewable Technologies

- 11.3.3 Kaluza

- 11.3.4 Ohme