|

시장보고서

상품코드

2071200

기후 위험 관리 시장 : 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Climate Risk Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

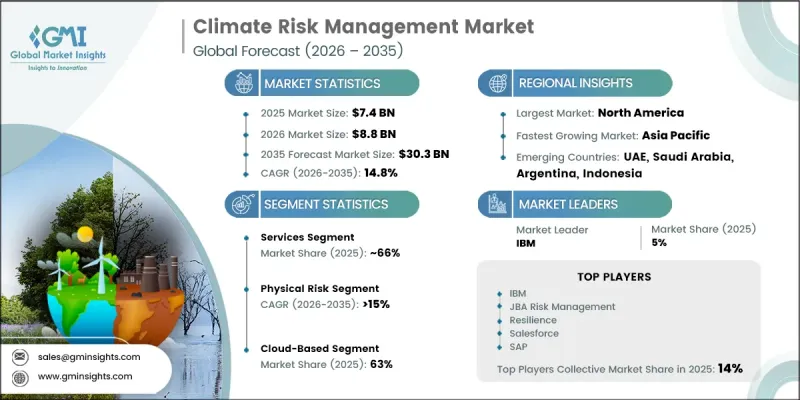

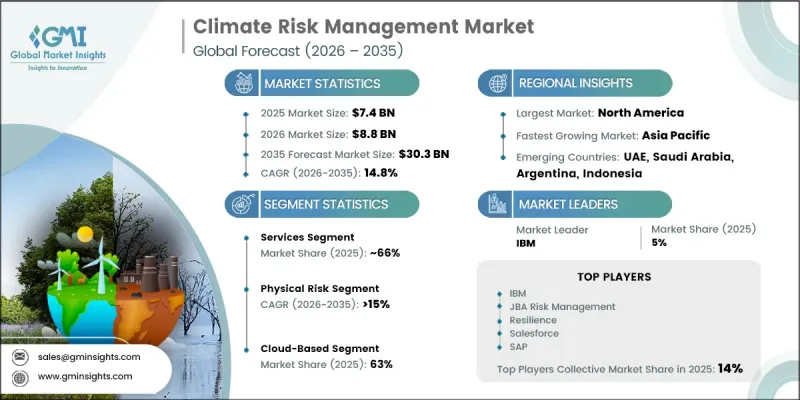

세계의 기후 위험 관리 시장은 2025년에 74억 달러 규모가 되어, 2035년까지 연평균 복합 성장률(CAGR) 14.8%로 성장하여 303억 달러에 이를 것으로 추정되고 있습니다.

시장 성장을 주도하고 있는 요인은 장기적인 사업 운영 및 재무 실적에 영향을 미칠 수 있는 기후 관련 위험을 파악, 평가 및 완화해야 할 필요성이 높아지고 있다는 점입니다. 기후 위험 관리 시장의 큰 변화 중 하나로, 미래의 기후 위험 노출을 정확하게 평가하기 위해서는 기존의 과거 손실 데이터 세트만으로는 더 이상 충분하지 않다는 인식이 확산되고 있습니다. 그 결과, 기업, 금융기관, 공공 부문 조직들은 예측 정확도를 높이고 리스크 계획 수립 능력을 강화하기 위해 시나리오 기반 및 확률론적 모델링 도구를 점점 더 많이 도입하고 있습니다. 또한, 여러 지역의 규제 체계도 자발적인 보고 관행에서 의무적인 규정 준수 요건으로 전환되고 있어, 첨단 기후 위험 솔루션에 대한 수요가 더욱 증가하고 있습니다. 인공지능, 머신러닝, 기후 데이터 분석 분야의 기술 발전으로 인해 기후 위험 평가의 정확도는 더욱 향상되고 있습니다. 데이터 수집 능력의 향상과 고해상도 기후 모니터링 시스템을 통해 솔루션 제공업체는 더욱 상세하고 실행 가능한 인사이트를 제공할 수 있게 되었습니다. 이러한 발전에 힘입어, 기후 위험 관리는 전 세계 모든 산업 분야에서 기업의 회복탄력성, 규제 준수 및 장기적인 전략적 계획의 핵심 요소로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 74억 달러 |

| 예측 금액 | 303억 달러 |

| CAGR | 14.8% |

아시아태평양의 기후 위험 관리 시장은 기후 변화로 인한 혼란에 대한 노출 증가, 급속한 도시 개발, 그리고 환경 리스크 관리에 대한 인식 제고에 힘입어 가장 빠르게 성장하는 지역 시장으로 부상하고 있습니다. 기후 변화로 인한 경제적·운영상의 영향이 두드러지게 나타나면서, 해당 지역의 조직들은 기후 회복력 계획의 중요성을 점점 더 강조하고 있습니다. 기후 인텔리전스 플랫폼, 예측 분석, 위험 평가 기술에 대한 투자 확대가 공공 부문과 민간 부문 모두에서 시장의 강력한 성장을 뒷받침하고 있습니다. 정부와 기업이 적응 전략을 강화하고 장기적인 지속가능성을 제고해 나가는 가운데, 해당 지역 전체에서 기후 위험 관리 솔루션에 대한 수요가 크게 증가할 것으로 예측됩니다.

서비스 부문은 2025년에 66%의 점유율을 차지하고, 2026년부터 2035년까지 연평균 성장률(CAGR) 14%로 성장할 것으로 전망됩니다. 이 부문이 주도적인 위치를 차지하고 있는 이유는 기후 위험 대응 프로젝트가 복잡한 성격을 띠고 있어 대부분의 경우 전문적인 지식이나 맞춤형 솔루션이 필요하기 때문입니다. 조직들은 기후 위험 모델링, 규제 준수 지원, 시나리오 계획 수립, 위험 평가 프레임워크 및 데이터 통합 활동에서 전문 서비스 제공업체에 자주 의존하고 있습니다. 맞춤형 자문 및 구현 서비스에 대한 수요가 증가함에 따라, 시장 내 이 부문의 우위가 계속해서 공고해지고 있습니다.

물리적 위험 부문은 46%의 점유율을 차지하고 있으며, 2035년까지 연평균 성장률(CAGR) 15%로 성장할 것으로 전망됩니다. 기후 변화와 관련된 혼란이 증가함에 따라, 업종을 불문하고 물리적 위험 평가 능력에 대한 수요가 높아지고 있습니다. 기업, 인프라 사업자, 정부 기관은 취약성 평가, 대비 전략 개선, 업무 중단 최소화, 그리고 정보에 기반한 투자 결정 지원을 위해 고도의 분석 및 예측 인텔리전스 도구를 점점 더 많이 활용하고 있습니다. 조직들이 회복탄력성과 장기적인 자산 보호를 우선시하는 가운데, 물리적 위험 관리는 보다 광범위한 기후 위험 관리 업계에서 여전히 중요한 중점 분야로 남아 있습니다.

미국 기후 위험 관리 시장은 88%의 점유율을 차지했으며, 2025년에는 24억 달러 시장 규모를 기록했습니다. 기후 변화로 인한 혼란에 따른 경제적 손실이 확대됨에 따라, 전미에서 정교한 기후 위험 평가 및 예측 솔루션에 대한 수요가 증가하고 있습니다. 조직들은 잠재적 취약점 파악, 중요 인프라 보호, 사업 연속성 계획 강화, 그리고 운영 회복탄력성 제고 측면에서 예측적 기후 정보의 중요성을 점차 인식하고 있습니다. 기후 변화와 관련된 불확실성이 기업의 의사결정 과정에서 더욱 중요한 고려 사항으로 부상함에 따라, 미국 내 여러 부문에서 기후 위험 관리 기술의 도입이 지속적으로 확대되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 솔루션별, 2022-2035년

제6장 시장 추산 및 예측 : 위험별, 2022-2035년

제7장 시장 추산 및 예측 : 도입 모드별, 2022-2035년

제8장 시장 추산 및 예측 : 용도별, 2022-2035년

제9장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제10장 시장 추산 및 예측 : 기업 규모별, 2022-2035년

제11장 시장 추산 및 예측 : 지역별, 2022-2035년

제12장 기업 개요

JHS 26.07.01The Global Climate Risk Management Market was valued at USD 7.4 billion in 2025 and is estimated to grow at a CAGR of 14.8% to reach USD 30.3 billion by 2035.

Market growth is driven by the increasing need for organizations to identify, evaluate, and mitigate climate-related risks that can affect long-term operational and financial performance. A major shift within the climate risk management market is the growing recognition that traditional historical loss datasets are no longer sufficient for accurately assessing future climate exposure. As a result, businesses, financial institutions, and public-sector organizations are increasingly adopting scenario-based and probabilistic modeling tools to improve forecasting accuracy and strengthen risk planning capabilities. Regulatory frameworks across multiple regions are also evolving from voluntary reporting practices toward mandatory compliance requirements, creating additional demand for advanced climate risk solutions. Technological advancements in artificial intelligence, machine learning, and climate data analytics are further enhancing the precision of climate risk assessments. Improved data collection capabilities and higher-resolution climate monitoring systems are enabling solution providers to deliver more detailed and actionable insights. These developments are positioning climate risk management as a critical component of enterprise resilience, regulatory compliance, and long-term strategic planning across industries worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.4 Billion |

| Forecast Value | $30.3 Billion |

| CAGR | 14.8% |

The Asia Pacific climate risk management market is emerging as the fastest-growing regional market, supported by increasing exposure to climate-related disruptions, rapid urban development, and growing awareness of environmental risk management. Organizations throughout the region are placing greater emphasis on climate resilience planning as the economic and operational consequences of changing climate conditions become more pronounced. Rising investments in climate intelligence platforms, predictive analytics, and risk assessment technologies are supporting strong market expansion across both public and private sectors. As governments and enterprises seek to strengthen adaptation strategies and improve long-term sustainability outcomes, demand for climate risk management solutions is expected to accelerate significantly throughout the region.

The services segment accounted for 66% share in 2025 and is anticipated to grow at a CAGR of 14% between 2026 and 2035. The segment's leadership reflects the complex nature of climate risk implementation projects, which often require specialized expertise and customized solutions. Organizations frequently rely on professional service providers for climate risk modeling, regulatory compliance support, scenario planning, risk assessment frameworks, and data integration activities. The growing need for tailored advisory and implementation services continues to reinforce the segment's dominant position within the market.

The physical risk segment held a 46% share and is projected to grow at a CAGR of 15% through 2035. Increasing climate-related disruptions are intensifying demand for physical risk assessment capabilities across industries. Businesses, infrastructure operators, and government agencies are increasingly utilizing advanced analytics and predictive intelligence tools to evaluate vulnerabilities, improve preparedness strategies, minimize operational disruptions, and support informed investment decisions. As organizations prioritize resilience and long-term asset protection, physical risk management remains a key focus area within the broader climate risk management industry.

United States Climate Risk Management Market held an 88% share, generating USD 2.4 billion in 2025. Growing economic losses associated with climate-related disruptions are increasing demand for sophisticated climate risk assessment and forecasting solutions across the country. Organizations are recognizing the importance of predictive climate intelligence for identifying potential vulnerabilities, protecting critical infrastructure, strengthening business continuity planning, and improving operational resilience. As climate-related uncertainties become a greater consideration in corporate decision-making, adoption of climate risk management technologies continues to expand across multiple sectors within the United States.

Leading companies operating in the global climate risk management market include IBM, SAP, Salesforce, JBA Risk Management, Resilience, First Street, and Fathom Global. Companies in the climate risk management market are implementing a range of strategies to strengthen their market position and expand their customer base. Major industry participants are investing heavily in artificial intelligence, machine learning, and advanced analytics to improve the accuracy and scalability of climate risk assessments. Strategic partnerships with financial institutions, government agencies, and sustainability organizations are helping companies broaden their market reach and enhance solution capabilities. Many providers are expanding their service portfolios by integrating climate intelligence, regulatory compliance tools, and scenario modeling platforms into comprehensive risk management ecosystems. Businesses are also focusing on product innovation, cloud-based deployment models, and real-time data integration to improve user experience and decision-making capabilities.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Solution

- 2.2.2 Risk

- 2.2.3 Deployment Mode

- 2.2.4 Application

- 2.2.5 Enterprise Size

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing frequency and intensity of extreme weather events amplifying risk exposure

- 3.2.1.2 Mounting regulatory pressure and mandatory climate disclosure requirements (TCFD, CSRD, Basel III)

- 3.2.1.3 Growing influence of ESG investors and institutional capital allocators

- 3.2.1.4 Advances in AI-powered climate modeling and scenario analytics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited availability of high-quality, standardized climate data

- 3.2.2.2 High implementation costs and technical expertise requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for climate risk solutions in global financial services

- 3.2.3.2 Expansion of green infrastructure and climate-resilient supply chain management

- 3.2.3.3 Emerging market adoption driven by climate vulnerability and regulatory convergence

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Securities and Exchange Commission (SEC) Climate Disclosure Requirements

- 3.4.1.2 Federal Reserve Climate Scenario Analysis Framework

- 3.4.1.3 Office of the Superintendent of Financial Institutions (OSFI) Guideline B-15 (Canada)

- 3.4.1.4 National Association of Insurance Commissioners (NAIC) Climate Risk Disclosure Survey

- 3.4.1.5 California Climate Corporate Data Accountability Act (SB 253)

- 3.4.2 Europe

- 3.4.2.1 Corporate Sustainability Reporting Directive (CSRD)

- 3.4.2.2 European Sustainability Reporting Standards (ESRS)

- 3.4.2.3 Sustainable Finance Disclosure Regulation (SFDR)

- 3.4.2.4 EU Taxonomy Regulation

- 3.4.2.5 European Banking Authority (EBA) ESG Risk Management Guidelines

- 3.4.3 Asia Pacific

- 3.4.3.1 China Environmental Information Disclosure Measures

- 3.4.3.2 China Green Finance Guidelines

- 3.4.3.3 India Business Responsibility and Sustainability Reporting (BRSR)

- 3.4.3.4 Monetary Authority of Singapore (MAS) Environmental Risk Management Guidelines

- 3.4.3.5 Japan Financial Services Agency (JFSA) Climate Disclosure Guidance

- 3.4.4 Latin America

- 3.4.4.1 Brazil Central Bank Climate and Environmental Risk Management Regulations

- 3.4.4.2 Brazilian Securities Commission (CVM) ESG Disclosure Requirements

- 3.4.4.3 Mexico Sustainable Taxonomy Framework

- 3.4.4.4 Mexico Banking and Securities Commission (CNBV) ESG Disclosure Guidelines

- 3.4.4.5 Chile Financial Market Commission (CMF) Climate Disclosure Requirements

- 3.4.5 Middle East & Africa

- 3.4.5.1 Saudi Green Initiative Sustainability Reporting Framework

- 3.4.5.2 Saudi Capital Market Authority (CMA) ESG Disclosure Guidelines

- 3.4.5.3 UAE Sustainable Finance Framework

- 3.4.5.4 South African Climate Change Bill and Climate Risk Reporting Initiatives

- 3.4.5.5 Johannesburg Stock Exchange (JSE) Sustainability and Climate Disclosure Guidance

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Software & Platforms

- 5.2.1 Risk Assessment & Scenario Analysis Platforms

- 5.2.2 Climate Risk Modeling Software

- 5.2.3 Regulatory Reporting & Compliance Platforms

- 5.2.4 Carbon Accounting & Emissions Tracking Software

- 5.2.5 Integrated Climate Risk Management Suites

- 5.3 Services

- 5.3.1 Data & Analytics Services

- 5.3.2 Professional & Consulting Services

- 5.3.2.1 Strategy & Advisory Services

- 5.3.2.2 Implementation & Integration Services

- 5.3.2.3 Training, Support & Managed Services

Chapter 6 Market Estimates & Forecast, By Risk, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Physical Risk

- 6.3 Transition Risk

- 6.4 Liability Risk

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Cloud-Based

- 7.3 On-Premises

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Carbon Accounting & Emissions Management

- 8.3 Disaster Preparedness & Early Warning Systems

- 8.4 ESG & Sustainable Investment Risk Analysis

- 8.5 Weather & Agriculture Risk Management

- 8.6 Business & Investment Risk Management

- 8.7 Climate Litigation & Liability Risk Management

- 8.8 Regulatory Reporting & Compliance

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 Energy & Utilities

- 9.4 Government & Public Sector

- 9.5 Real Estate & Infrastructure

- 9.6 Agriculture & Forestry

- 9.7 Manufacturing

- 9.8 Transportation & Logistics

- 9.9 Healthcare

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Enterprise Size, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 Large Enterprises

- 10.3 SME

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Southeast Asia

- 11.4.5.1 Indonesia

- 11.4.5.2 Malaysia

- 11.4.5.3 Singapore

- 11.4.5.4 Thailand

- 11.4.5.5 Vietnam

- 11.4.6 ANZ

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Argentina

- 11.5.3 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Fathom Global

- 12.1.2 First Street

- 12.1.3 IBM (Envizi)

- 12.1.4 JBA Risk Management

- 12.1.5 Jupiter Intelligence

- 12.1.6 Salesforce

- 12.1.7 SAP

- 12.1.8 XDI (Cross Dependency Initiative)

- 12.2 Regional Players

- 12.2.1 Climate X

- 12.2.2 ClimateAi

- 12.2.3 Mitiga Solutions

- 12.2.4 Resilience

- 12.2.5 RiskThinking.AI

- 12.2.6 StepChange

- 12.2.7 Sust Global

- 12.3 Emerging Players

- 12.3.1 Climafin

- 12.3.2 Correntics

- 12.3.3 Entelligent

- 12.3.4 Intensel

- 12.3.5 Vyzrd