|

시장보고서

상품코드

2071241

질소 고정 곡물 시장 : 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Nitrogen-Fixing Cereals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

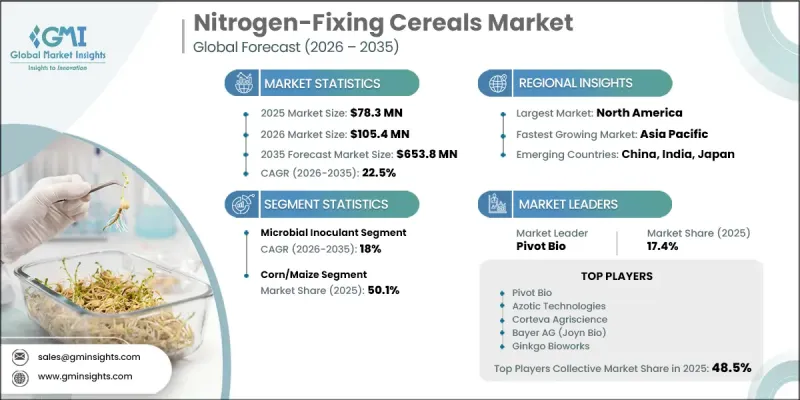

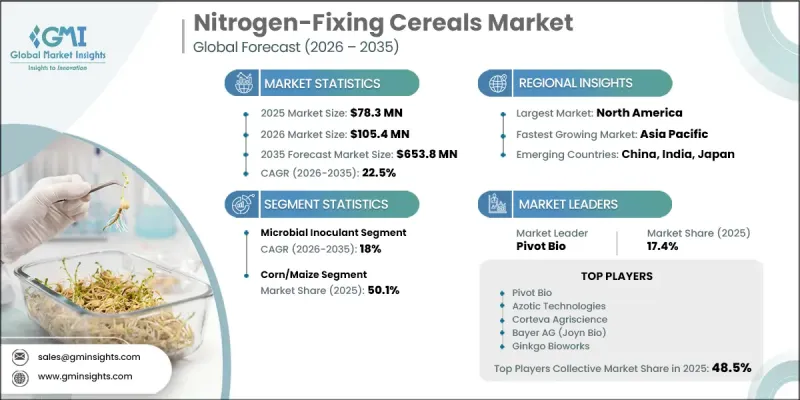

세계의 질소 고정 곡물 시장은 2025년에 7,830만 달러 규모가 되어, 22.5%의 연평균 복합 성장률(CAGR)로 확대되어 2035년까지 6억 5,380만 달러에 이를 것으로 추정되고 있습니다.

시장의 성장은 지속 가능한 영양 관리 방식의 도입 확대에 힘입고 있습니다. 이러한 급속한 확대는 곡물 생산에서 질소 관리 방식을 변화시키고 있는 경제적, 환경적, 규제적 요인들이 복합적으로 작용한 결과입니다. 기존 비료와 관련된 투입 비용의 상승과 질소 배출을 대상으로 한 환경 규제의 강화로 인해, 생물학적 대체 수단에 대한 관심이 높아지고 있습니다. 동시에, 미생물 과학 및 생명공학의 기술 발전으로 인해 주요 곡물 작물에 질소 고정 능력이 부여되면서 전 세계 농업 시스템에 새로운 기회가 열리고 있습니다. 이러한 혁신을 통해 생물 유래 자재의 역할은 기존의 용도를 넘어 확대되고 있으며, 질소 고정 솔루션은 환경에 미치는 영향을 줄이면서 작물 생산성을 향상시키기 위한 실현 가능하고 확장성 있는 대안으로서의 입지를 확고히 다지고 있습니다. 지속적인 비용 압박과 지속가능성에 관한 규제 요건이 대규모 농업 경영에서 이러한 솔루션의 장기적인 가치 제안을 더욱 공고히 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 7,830만 달러 |

| 예측 금액 | 6억 5,380만 달러 |

| CAGR | 22.5% |

2025년, 미생물 제제 부문은 95.5%의 시장 점유율을 차지하며 7,480만 달러에 달했습니다. 이 부문에는 질소 고정 미생물을 기반으로 한 생물 제제가 포함되어 있으며, 다양한 시용 방법을 통해 활용되기 때문에 상업적으로 가장 확고하게 자리 잡은 솔루션 범주입니다. 이러한 보급은 표준적인 농업 유통 채널을 통해 구하기 쉬워진 점과, 기존의 농업 관행에 원활하게 통합될 수 있다는 점에 힘입어 이루어지고 있습니다.

옥수수(maize) 부문은 2025년에 50.1%의 점유율을 차지하며, 전 세계 질소 수요에서 중심적인 역할을 하고 있음이 부각되었습니다. 이 부문의 강력한 입지는 이러한 작물의 대규모 재배와, 해당 생산 시스템에 맞춘 생물학적 질소 솔루션의 도입 확대에 힘입어 유지되고 있습니다. 이 분야의 상업적 전개는 비교적 진전된 단계에 이르렀으며, 시장 전체의 수익에 크게 기여하고 있습니다.

2025년, 북미의 질소 고정 곡물 시장은 52.9%의 점유율을 차지했으며, 그중 미국이 가장 큰 기여를 한 국가가 되었습니다. 이 지역의 선도적 지위는 주요 곡물 생산 지역에서 광범위하게 도입된 기술과, 생물학적 투입재의 통합을 촉진하는 확립된 농업 인프라에 의해 뒷받침되고 있습니다. 활발한 상업 활동과 농가들의 높은 의식이 주요 생산 지역 전반에 걸쳐 질소 고정 기술의 도입을 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기술 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 곡물 유형별, 2022-2035년

제7장 시장 추산 및 예측 : 시용 방법별, 2022-2035년

제8장 시장 추산 및 예측 : 최종 사용자별, 2022-2035년

제9장 시장 추산 및 예측 : 지역별, 2022-2035년

제10장 기업 개요

JHS 26.07.01The Global Nitrogen-Fixing Cereals Market was valued at USD 78.3 million in 2025 and is estimated to grow at a CAGR of 22.5% to reach USD 653.8 million by 2035.

Market growth is supported by increasing adoption of sustainable nutrient management practices. The rapid expansion reflects a combination of economic, environmental, and regulatory factors reshaping how nitrogen is managed in cereal crop production. Rising input costs associated with conventional fertilizers and stricter environmental regulations targeting nitrogen emissions are driving interest in biological alternatives. At the same time, technological advancements in microbial science and bioengineering are enabling nitrogen-fixing capabilities in major cereal crops, creating new opportunities across global farming systems. These innovations are expanding the role of biological inputs beyond traditional applications, positioning nitrogen-fixing solutions as a viable and scalable alternative for improving crop productivity while reducing environmental impact. Continued cost pressures and sustainability mandates are reinforcing the long-term value proposition of these solutions across large-scale agricultural operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $78.3 Million |

| Forecast Value | $653.8 Million |

| CAGR | 22.5% |

The microbial inoculants segment held a 95.5% share in 2025, accounting for USD 74.8 million. This segment includes biological formulations based on nitrogen-fixing microorganisms that are applied through multiple delivery methods, making them the most commercially established solution category. Their adoption is supported by increasing accessibility through standard agricultural distribution channels and their ability to integrate seamlessly into existing farming practices.

The corn and maize segment accounted for 50.1% share in 2025, highlighting their central role in global nitrogen demand. The strong presence of this segment is driven by the large-scale cultivation of these crops and the increasing adoption of biological nitrogen solutions tailored to their production systems. Commercial deployment in this category has reached a relatively advanced stage, contributing significantly to overall market revenue.

North America Nitrogen-Fixing Cereals Market held a 52.9% share in 2025, with the United States representing the largest contributor. The region's leadership is supported by widespread adoption across major cereal-producing areas and a well-established agricultural infrastructure that facilitates the integration of biological inputs. High levels of commercial activity and strong farmer awareness are accelerating the deployment of nitrogen-fixing technologies across key production regions.

Major companies operating in the global nitrogen-fixing cereals market include Pivot Bio, Azotic Technologies, Bayer AG (Joyn Bio), Corteva Agriscience, Ginkgo Bioworks, TerraMax (EcoCulture), Legume Technology, Kula Bio, Switch Bioworks, BNF Cereals (INIA-CSIC), UC Davis (Blumwald Lab), MIT, University of Cambridge, Oxford University, and INBIOTEC-CONICET. Companies in the Nitrogen-Fixing Cereals market are strengthening their competitive position through continuous innovation, strategic collaborations, and expansion of research capabilities. Industry participants are heavily investing in advanced biological technologies to improve nitrogen fixation efficiency and broaden crop compatibility. Partnerships with agricultural distributors and research institutions are enabling faster commercialization and wider adoption of these solutions. Companies are also focusing on scaling production capabilities to meet growing demand while maintaining product consistency and performance. Expanding geographic presence in key agricultural regions remains a priority to capture untapped market potential.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology type

- 2.2.3 Cereal crop type

- 2.2.4 Application method

- 2.2.5 End user

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Microbial inoculants

- 5.3 Genetically engineered crops

Chapter 6 Market Estimates and Forecast, By Cereal Crop Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Corn/maize

- 6.3 Wheat

- 6.4 Rice

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application Method, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Seed treatment

- 7.2.1 Dry seed coating

- 7.2.2 Liquid seed treatment

- 7.3 In-furrow application

- 7.3.1 Granular formulations

- 7.3.2 Liquid formulations

- 7.4 Foliar application

- 7.5 Integrated genetic trait

Chapter 8 Market Estimates and Forecast, By End User, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Large-scale commercial farms

- 8.3 Mid-sized farms

- 8.4 Smallholder farmers

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Azotic Technologies

- 10.2 Bayer AG (Joyn Bio)

- 10.3 BNF Cereals (INIA-CSIC)

- 10.4 Corteva Agriscience

- 10.5 Ginkgo Bioworks

- 10.6 Kula Bio

- 10.7 Legume Technology

- 10.8 Pivot Bio

- 10.9 Switch Bioworks

- 10.10 TerraMax (EcoCulture)

(주말 및 공휴일 제외)