|

시장보고서

상품코드

2071243

에너지 및 전력 분야 디지털 트윈 시장 : 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Digital Twin in Energy and Power Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

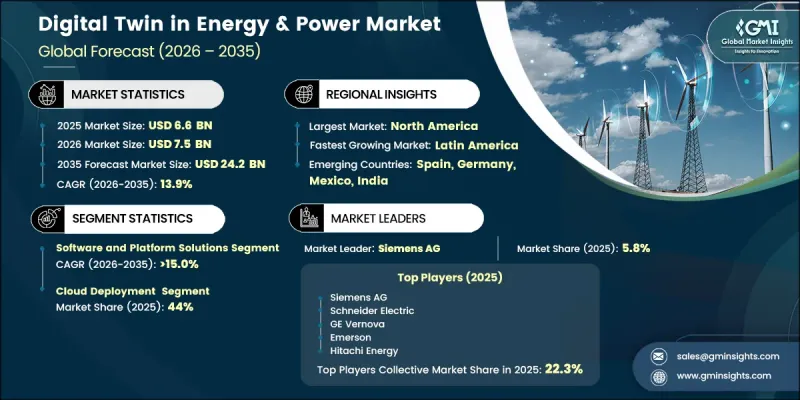

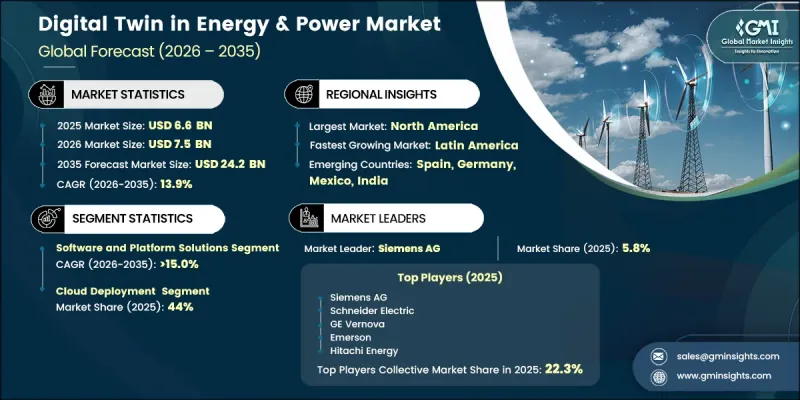

세계의 에너지 및 전력 분야 디지털 트윈 시장은 2025년에 66억 달러로 평가되었고 CAGR 13.9%로 성장하여 2035년까지 242억 달러에 이를 것으로 추정되고 있습니다.

전력 회사, 송전망 사업자, 에너지 자산 운용사가 운용 효율을 높이기 위해 첨단 시뮬레이션 및 실시간 모니터링 도구에 대한 의존도를 높이고 있어, 해당 시장은 급속히 확대되고 있습니다. 이러한 성장은 풍력 및 태양광에 의한 간헐적인 발전이 기존의 조절 가능한 전원을 대체하는 재생에너지 발전이 주도하는 전력 시스템으로의 전 세계적 전환에 큰 영향을 받고 있습니다. 그 결과, 송전망 사업자들은 물리적 확장에만 의존하기보다는 기존 인프라를 최적화할 수 있는 지능형 시스템을 우선시하고 있습니다. 디지털 트윈 솔루션을 통해 송전망의 동작을 지속적으로 모델링할 수 있게 되어, 운영자는 고장 시뮬레이션, 부하 상황 평가 및 혼잡 관리 개선을 실시간으로 수행할 수 있습니다. 송전, 배전, 발전 자산 전반에 걸쳐 IoT 지원 기기의 도입이 확대됨에 따라 데이터의 가용성과 모델의 정확도가 크게 향상되고 있습니다. 스마트 센서, 엣지 컴퓨팅 기기, 동기화 파소어 시스템, 지능형 계량 인프라 등의 기술이 고해상도 디지털 트윈 플랫폼의 기반을 강화하고 있습니다. 그러나 도입에는 하드웨어 구축, 통합 시스템, 소프트웨어 플랫폼 및 직원 역량 강화를 위한 막대한 투자가 필요하기 때문에 전력사 전체 차원의 대규모 도입은 단계적인 과정으로 진행되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 66억 달러 |

| 예측 금액 | 242억 달러 |

| CAGR | 13.9% |

소프트웨어 및 플랫폼 기반 서비스 부문은 2025년에 56%의 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 15%로 성장할 것으로 전망됩니다. 이러한 선도적인 지위는 인프라 비용을 비례적으로 증가시키지 않으면서도 부가가치를 높일 수 있는 소프트웨어 솔루션의 확장성에서 비롯됩니다. 센서 네트워크와 연결 프레임워크가 구축되면, 유틸리티자들은 소프트웨어 업그레이드나 플랫폼 기능 강화를 통해 분석 및 시뮬레이션 기능 확충에 점점 더 많은 투자를 하게 될 것입니다.

클라우드 기반 도입 모델 부문은 2025년에 44%의 점유율을 차지했습니다. 이러한 성장은 클라우드 인프라 비용의 감소, 에너지에 특화된 클라우드 서비스의 이용 가능성 향상, 그리고 분산형 에너지 네트워크 전반에 걸친 대규모 실시간 데이터의 관리 및 처리 능력에 힘입어 이루어지고 있습니다. 또한, 클라우드 플랫폼은 현대 에너지 시스템의 운영 요건에 부합하는 유연성과 확장성을 제공합니다.

2025년, 북미 에너지 및 전력 시장에서 디지털 트윈의 점유율은 38%를 차지하고, 2035년까지 연평균 성장률(CAGR) 12.6%로 성장할 것으로 전망됩니다. 이 지역의 성장은 대규모 인프라 현대화 사업, 전력 회사의 디지털화 이니셔티브 확대, 그리고 유서 깊은 기술 공급업체들의 적극적인 진출에 힘입어 이루어지고 있습니다. 송전망 현대화 및 복원력 강화 프로그램에 대한 지속적인 투자를 통해, 에너지 네트워크 전반에 걸친 첨단 디지털 트윈 기술의 지역적 도입이 더욱 강화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 컴포넌트별, 2022-2035년

제6장 시장 규모 및 예측 : 전개 형태별, 2022-2035년

제7장 시장 규모 및 예측 : 트윈 유형별, 2022-2035년

제8장 시장 규모 및 예측 : 용도별, 2022-2035년

제9장 시장 규모 및 예측 : 최종 사용자별, 2022-2035년

제10장 시장 규모 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

JHSThe Global Digital Twin in Energy & Power Market was valued at USD 6.6 billion in 2025 and is estimated to grow at a CAGR of 13.9% to reach USD 24.2 billion by 2035.

The market is expanding rapidly as utilities, grid operators, and energy asset managers increasingly rely on advanced simulation and real-time monitoring tools to improve operational efficiency. This growth is strongly influenced by the global transition toward renewable-dominant power systems, where intermittent energy generation from wind and solar is replacing conventional dispatchable sources. As a result, grid operators are prioritizing intelligent systems capable of optimizing existing infrastructure rather than relying solely on physical expansion. Digital twin solutions enable continuous modeling of grid behavior, allowing operators to simulate faults, assess load conditions, and improve congestion management in real time. The rising deployment of IoT-enabled devices across transmission, distribution, and generation assets is significantly improving data availability and model accuracy. Technologies such as smart sensors, edge computing devices, synchrophasor systems, and intelligent metering infrastructure are strengthening the foundation for high-resolution digital twin platforms. However, implementation requires considerable investment in hardware deployment, integration systems, software platforms, and workforce upskilling, making large-scale adoption a phased process across utilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.6 Billion |

| Forecast Value | $24.2 Billion |

| CAGR | 13.9% |

The software and platform-based offerings segment held a 56% share in 2025 and is expected to grow at a CAGR of 15% through 2035. This leadership is attributed to the scalable nature of software solutions, where incremental value can be added without proportional increases in infrastructure costs. Once sensor networks and connectivity frameworks are established, utilities increasingly invest in expanding analytical and simulation capabilities through software upgrades and platform enhancements.

The cloud-based deployment models segment held 44% share in 2025. Their growth is supported by improved affordability of cloud infrastructure, increased availability of energy-focused cloud services, and the ability to manage and process large-scale real-time data across distributed energy networks. Cloud platforms also offer flexibility and scalability that align with the operational requirements of modern energy systems.

North America Digital Twin in Energy & Power Market accounted for 38% share in 2025 and is projected to grow at a CAGR of 12.6% through 2035. The region's growth is supported by large-scale infrastructure modernization efforts, increasing utility digitalization initiatives, and strong participation from established technology vendors. Continued investments in grid modernization and resilience programs are further strengthening regional adoption of advanced digital twin technologies across energy networks.

Key companies operating in the Global Digital Twin In Energy & Power Market include Siemens Energy, Schneider Electric, ABB Ltd., GE Vernova, Honeywell International, IBM Corporation, Microsoft, Accenture, Dassault Systemes, Emerson, Hitachi Energy, Bentley Systems, PTC Inc., ANSYS Inc., ETAP, Hexagon AB, Cognite AS, Yokogawa Electric, Kongsberg Digital, and Siemens AG. Market participants are actively strengthening their competitive position by investing in advanced analytics capabilities, AI-driven modeling tools, and cloud-native digital twin platforms. Strategic partnerships with utilities and grid operators are helping companies integrate solutions directly into operational workflows. Many firms are focusing on expanding their software ecosystems to offer end-to-end simulation, monitoring, and predictive maintenance capabilities. Continuous product innovation, particularly in real-time data processing and asset performance optimization, is enhancing solution value. Companies are also prioritizing global expansion strategies and sector-specific customization to address varying regulatory and infrastructure needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Components trends

- 2.4 Deployment trends

- 2.5 Twin type trends

- 2.6 Application trends

- 2.7 End user trends

- 2.8 Region trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.2.1 North America

- 3.2.2 Europe

- 3.2.3 Asia Pacific

- 3.2.4 Middle East & Africa

- 3.2.5 Latin America

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Impact of AI & generative AI on the market

- 3.7.1 Predictive maintenance & fault detection

- 3.7.2 Grid optimization & load forecasting

- 3.7.3 Digital twin simulation & testing

- 3.7.4 Risks, limitations & regulatory considerations

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Overall investment scenario and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Component, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Software & platforms

- 5.3 Hardware

- 5.4 Services

Chapter 6 Market Size and Forecast, By Deployment, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

- 6.4 Hybrid

Chapter 7 Market Size and Forecast, By Twin type, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Asset twin

- 7.3 Process/system twin

- 7.4 Plant/facility twin

- 7.5 Grid/network twin

- 7.6 Enterprise/system-of-systems twin

- 7.7 Others

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Asset performance management

- 8.3 Predictive maintenance

- 8.4 Grid optimization & monitoring

- 8.5 Process optimization

- 8.6 Energy management

- 8.7 Remote monitoring & diagnostics

- 8.8 Simulation & scenario planning

- 8.9 Safety, risk & compliance management

- 8.10 Others

Chapter 9 Market Size and Forecast, By End user, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Oil & gas

- 9.3 Power generation

- 9.4 Utilities & grid operators

- 9.5 Renewable energy

- 9.6 Others

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Norway

- 10.3.5 Italy

- 10.3.6 Spain

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Qatar

- 10.5.4 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Mexico

Chapter 11 Company Profiles

- 11.1 ABB Ltd.

- 11.2 Accenture

- 11.3 ANSYS Inc.

- 11.4 Bentley Systems

- 11.5 Cognite AS

- 11.6 Dassault Systemes

- 11.7 Emerson

- 11.8 ETAP

- 11.9 GE Vernova

- 11.10 Hexagon AB

- 11.11 Hitachi Energy

- 11.12 Honeywell International

- 11.13 IBM Corporation

- 11.14 Kongsberg Digital

- 11.15 Microsoft

- 11.16 PTC Inc.

- 11.17 Schneider Electric

- 11.18 Siemens AG

- 11.19 Siemens Energy

- 11.20 Yokogawa Electric