|

시장보고서

상품코드

2071252

자동차용 컴퓨터 비전 시장 : 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Computer Vision Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

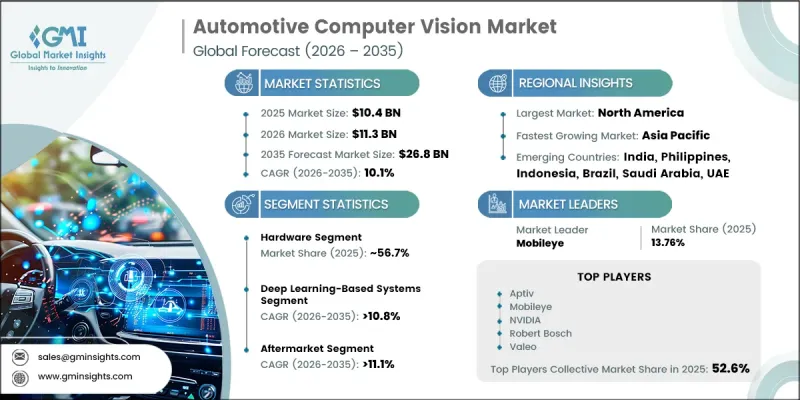

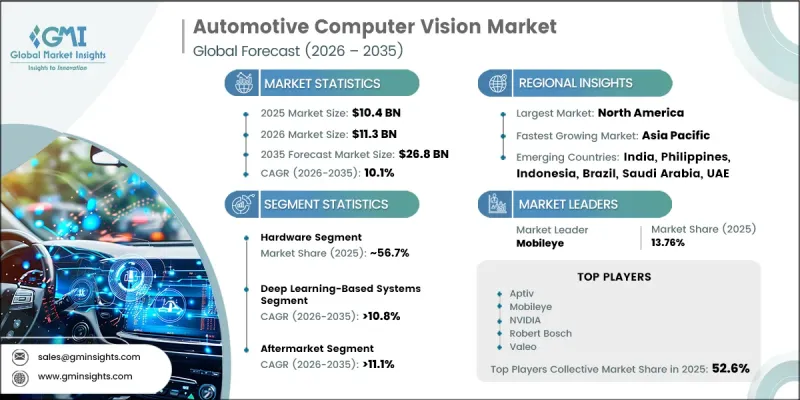

세계의 자동차용 컴퓨터 비전 시장은 2025년에 104억 달러 규모가 되어, 2035년까지 연평균 복합 성장률(CAGR) 10.1%로 성장하여 268억 달러에 이를 것으로 추정되고 있습니다.

이러한 성장은 승용차 및 상용차에 ADAS(첨단 운전자 보조 시스템), 자율주행 기능, 그리고 지능형 안전 기술의 도입이 확대됨에 따라 주도되고 있습니다. 자동차 제조업체와 기술 제공업체들은 상황 인식 능력 향상, 충돌 위험 감소, 그리고 실시간 환경 인식 능력 향상을 도모하기 위해 AI를 활용한 비전 시스템의 탑재를 점점 더 확대되고 있습니다. 정부가 더욱 엄격한 차량 안전 요건을 시행하고 차세대 모빌리티 기준을 추진하는 가운데, 교통 안전 당국의 규제 압력 또한 이 기술의 도입을 더욱 가속화하고 있습니다. 또한, 전기차와 커넥티드카의 보급 확대 역시 반자율 주행 및 자율 주행 기능을 지원할 수 있는 고성능 비전 시스템에 대한 수요를 뒷받침하고 있습니다. 인공지능, 센서 융합, 실시간 데이터 처리 분야의 지속적인 발전은 자동차 설계의 우선순위를 재편하고 있으며, 컴퓨터 비전은 전 세계 자동차 생태계에서 현대 차량 아키텍처의 핵심 구성 요소로 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 104억 달러 |

| 예측 금액 | 268억 달러 |

| CAGR | 10.1% |

하드웨어 부문은 2025년에 56.7%의 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 9.2%로 성장할 것으로 전망됩니다. 이러한 우위는 실시간 차량 인식에 필요한 첨단 센싱 및 컴퓨팅 구성 요소의 통합이 진전되고 있는 데 기인합니다. 자동차용 비전 시스템은 정확한 환경 매핑과 신속한 의사 결정을 뒷받침하는 고성능 이미지 처리 및 감지 기술에 크게 의존하고 있습니다. 지능형 안전 기능 및 운전 지원 기능의 도입이 확대됨에 따라, 동적인 주행 환경에서 발생하는 복잡한 데이터 처리 요구 사항을 충족할 수 있는 견고한 하드웨어 시스템에 대한 수요가 계속해서 증가하고 있습니다.

딥러닝 기반 시스템 부문은 2025년에 49%의 시장 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 10.8%로 성장할 것으로 전망됩니다. 이 부문이 주도적인 위치를 차지하고 있는 것은 방대한 양의 시각 데이터를 높은 정확도와 적응성을 바탕으로 처리할 수 있는 능력 덕분입니다. 딥러닝 기술은 물체 감지, 분류, 인식 능력을 향상시켜 차량이 다양한 조건 하에서 복잡한 도로 환경을 해석할 수 있게 해줍니다. 대규모 데이터 세트를 활용한 지속적인 모델 학습을 통해 시간이 지남에 따라 성능이 향상되므로, 이러한 시스템은 첨단 모빌리티 용도에 매우 적합합니다.

미국 자동차용 컴퓨터 비전 시장은 83.5%의 점유율을 차지했으며, 2025년에는 30억 달러 규모 시장 규모를 기록했습니다. 해당 국가 시장 성장은 모든 차종에 걸친 ADAS(첨단 운전자 보조 시스템), 자율주행 기술 및 커넥티드 모빌리티 플랫폼의 급속한 도입에 힘입어 이루어지고 있습니다. 대형 기술 기업과 자동차 제조업체들의 적극적인 진출이 AI 기반 지각 시스템, 센서 통합 및 실시간 분석 분야의 혁신을 가속화하고 있습니다. 확립된 혁신 생태계의 존재가 자동차용 컴퓨터 비전 개발 분야에서 해당 국가의 리더십을 더욱 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 컴포넌트별, 2022-2035년

제6장 시장 추산 및 예측 : 판매 채널별, 2022-2035년

제7장 시장 추산 및 예측 : 기술별, 2022-2035년

제8장 시장 추산 및 예측 : 용도별, 2022-2035년

제9장 시장 추산 및 예측 : 차량별, 2022-2035년

제10장 시장 추산 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

JHS 26.07.01The Global Automotive Computer Vision Market was valued at USD 10.4 billion in 2025 and is estimated to grow at a CAGR of 10.1% to reach USD 26.8 billion by 2035.

Growth is driven by the rising deployment of advanced driver assistance systems, autonomous driving capabilities, and intelligent safety technologies across passenger and commercial vehicles. Automotive manufacturers and technology providers are increasingly embedding AI-powered vision systems to enhance situational awareness, reduce collision risks, and improve real-time environmental perception. Regulatory pressure from transportation safety authorities is further accelerating adoption, as governments enforce stricter vehicle safety requirements and promote next-generation mobility standards. Expanding penetration of electric and connected vehicles is also reinforcing demand for high-performance vision systems capable of supporting semi-autonomous and autonomous driving functions. Continuous advancements in artificial intelligence, sensor fusion, and real-time data processing are reshaping automotive design priorities, making computer vision a core component of modern vehicle architecture across global automotive ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.4 Billion |

| Forecast Value | $26.8 Billion |

| CAGR | 10.1% |

The hardware segment held 56.7% share in 2025 and is projected to grow at a CAGR of 9.2% through 2035. Its dominance is attributed to the increasing integration of advanced sensing and computing components required for real-time vehicle perception. Automotive vision systems rely heavily on high-performance imaging and detection technologies that support accurate environmental mapping and rapid decision-making. Rising deployment of intelligent safety and driver assistance features continues to drive demand for robust hardware systems capable of handling complex data processing requirements in dynamic driving environments.

The deep learning-based systems segment accounted for 49% share in 2025 and is expected to grow at a CAGR of 10.8% through 2035. This segment leads due to its ability to process vast volumes of visual data with high precision and adaptability. Deep learning technologies enhance object detection, classification, and recognition capabilities, allowing vehicles to interpret complex road environments under varying conditions. Continuous model training using large datasets enables performance improvements over time, making these systems highly suitable for advanced mobility applications.

United States Automotive Computer Vision Market held an 83.5% share, generating USD 3 billion in 2025. Market growth in the country is supported by the rapid integration of advanced driver assistance systems, autonomous driving technologies, and connected mobility platforms across vehicle categories. Strong participation from leading technology firms and automotive manufacturers is accelerating innovation in AI-driven perception systems, sensor integration, and real-time analytics. The presence of established innovation ecosystems continues to reinforce the country's leadership in automotive computer vision development.

Key companies operating in the global automotive computer vision market include Valeo, Robert Bosch, Renesas Electronics, Qualcomm Technologies, Onsemi, NXP Semiconductors, NVIDIA, Mobileye, Continental, and Aptiv. Market participants are focusing on strengthening their competitive positioning through continuous investment in artificial intelligence, machine learning, and high-performance computing technologies. Companies are enhancing their product portfolios with advanced vision sensors, AI-enabled processors, and integrated software platforms designed for real-time vehicle perception. Strategic collaborations with automotive OEMs and mobility service providers are accelerating deployment across next-generation vehicle platforms. Firms are also investing in research and development to improve object detection accuracy, system reliability, and processing speed under diverse driving conditions. Expansion of global manufacturing capabilities and localization of supply chains are further supporting scalability.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast Model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Sales channel

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 Vehicle

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of advanced driver assistance systems (ADAS)

- 3.2.1.2 Growing development of autonomous and semi-autonomous vehicles

- 3.2.1.3 Increasing government vehicle safety regulations and mandates

- 3.2.1.4 Expansion of electric and connected vehicle ecosystems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and integration costs of vision systems

- 3.2.2.2 Complexity in real-time data processing and sensor calibration

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for driver monitoring and in-cabin sensing systems

- 3.2.3.2 Expansion of robotaxi and autonomous mobility services

- 3.2.3.3 Increasing integration of Ai-powered vision systems in commercial vehicles

- 3.2.3.4 Emerging smart city and intelligent transportation infrastructure projects

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and Innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Cost breakdown analysis

- 3.7 Regulatory guidline

- 3.7.1 North America

- 3.7.1.1 U.S.: NHTSA Vehicle Safety Standards & FMVSS ADAS Compliance Regulations

- 3.7.1.2 Canada: Transport Canada Motor Vehicle Safety Regulations & Autonomous Vehicle Testing Frameworks.

- 3.7.2 Europe

- 3.7.2.1 Germany: EU General Safety Regulation (GSR) & KBA Autonomous Driving Compliance Standards

- 3.7.2.2 UK: Automated Vehicles Act & DVSA Vehicle Safety Compliance Framework

- 3.7.2.3 France: CNIL Automotive Data Protection Regulations & Intelligent Transport System Standards

- 3.7.2.4 Italy: EU ADAS Mandates & UNECE Vehicle Cybersecurity Regulations

- 3.7.3 Asia Pacific

- 3.7.3.1 China: Intelligent Connected Vehicle (ICV) Regulations & Automotive Data Security Laws

- 3.7.3.2 India: Bharat NCAP Safety Standards & AIS-140 Intelligent Transportation Regulations

- 3.7.3.3 Japan: MLIT Autonomous Driving Safety Guidelines & APPI Data Protection Framework

- 3.7.3.4 South Korea: KNCAP Vehicle Safety Standards & Personal Information Protection Act (PIPA)

- 3.7.3.5 Australia: Australian Design Rules (ADR) & Automated Vehicle Safety Frameworks

- 3.7.4 Latin America

- 3.7.4.1 Brazil: CONTRAN Vehicle Safety Regulations & Intelligent Mobility Compliance Standards

- 3.7.4.2 Mexico: NOM Vehicle Safety Standards & Connected Vehicle Regulatory Framework

- 3.7.4.3 Argentina: National Road Safety Agency (ANSV) ADAS Compliance Guidelines

- 3.7.5 MEA

- 3.7.5.1 UAE: UAE Autonomous Mobility Strategy & Smart Vehicle Safety Regulations

- 3.7.5.2 Saudi Arabia: SASO Vehicle Safety Standards & Smart Mobility Regulatory Framework

- 3.7.5.3 South Africa: National Road Traffic Act & Vehicle Safety Compliance Regulations

- 3.7.1 North America

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Patent Landscape (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.12.2 Optimistic Scenarios - Favourable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 OEM

- 6.3 Aftermarket

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Machine Vision-Based Systems

- 7.3 Deep Learning-Based Systems

- 7.4 Sensor Fusion-Based Systems

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Advanced Driver Assistance Systems (ADAS)

- 8.3 Autonomous Driving

- 8.4 In-Cabin Monitoring

- 8.5 Traffic & Infrastructure Vision

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Passenger Cars

- 9.2.1 Hatchbacks

- 9.2.2 Sedans

- 9.2.3 SUVs

- 9.3 Commercial Vehicles

- 9.3.1 Light Commercial Vehicles

- 9.3.2 Heavy Commercial Vehicles

- 9.4 Electric Vehicles (EVs)

- 9.4.1 Battery Electric Vehicles (BEV)

- 9.4.2 Plug-In Hybrid Electric Vehicles (PHEV)

- 9.5 Autonomous Vehicles

- 9.5.1 Robotaxis & Shared Autonomous Mobility

- 9.5.2 Self-Driving Trucks & Freight

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Belgium

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aptiv

- 11.1.2 Continental

- 11.1.3 Mobileye

- 11.1.4 NVIDIA

- 11.1.5 NXP Semiconductors

- 11.1.6 Onsemi

- 11.1.7 Qualcomm Technologies

- 11.1.8 Renesas Electronics

- 11.1.9 Robert Bosch

- 11.1.10 Sony Semiconductor

- 11.1.11 Valeo

- 11.2 Regional Players

- 11.2.1 Black Sesame Technologies

- 11.2.2 Denso

- 11.2.3 FORVIA HELLA

- 11.2.4 Hikvision Automotive

- 11.2.5 Hitachi Astemo

- 11.2.6 Horizon Robotics

- 11.2.7 Hyundai Mobis

- 11.2.8 Magna International

- 11.2.9 ZF Friedrichshafen

- 11.3 Emerging Players

- 11.3.1 Ambarella

- 11.3.2 Autobrains Technologies

- 11.3.3 indie Semiconductor

- 11.3.4 STRADVision