|

시장보고서

상품코드

2071301

선박용 디젤 엔진 시장 : 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Marine Diesel Engines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

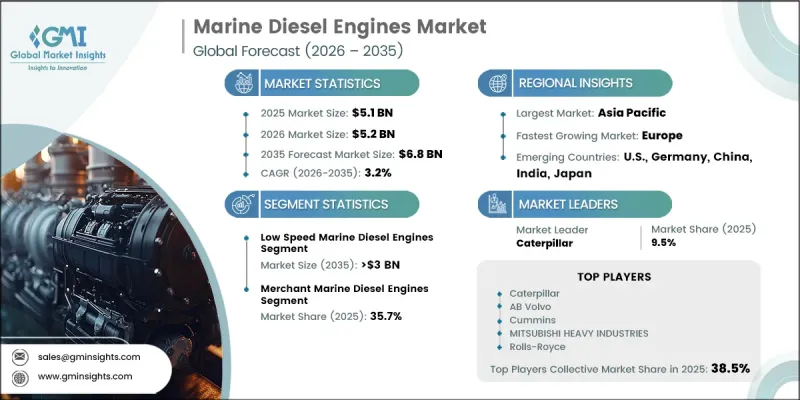

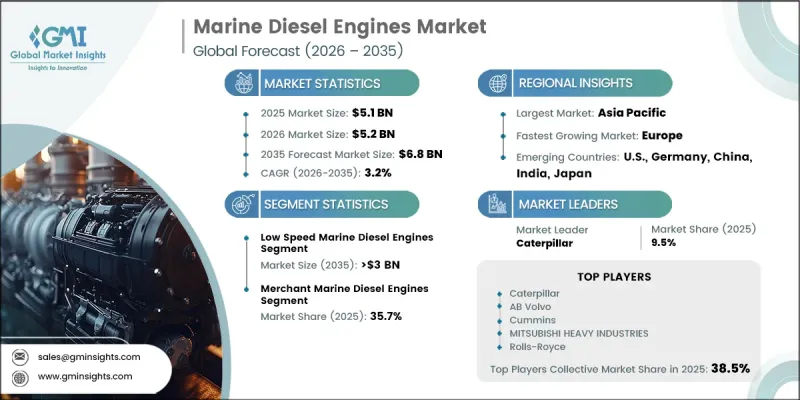

세계의 선박용 디젤 엔진 시장은 2025년에 51억 달러 규모가 되어, CAGR 3.2%로 성장하여 2035년까지 68억 달러에 이를 것으로 추정되고 있습니다.

해운 업계가 배기가스 감축, 점점 더 엄격해지는 환경 규제 준수, 그리고 끊임없이 변화하는 이해관계자들의 기대에 부응하기 위한 노력을 강화함에 따라, 선박용 디젤 엔진 시장은 큰 변화를 겪고 있습니다. 이러한 변화에 따라 선주, 선박 운항 사업자 및 엔진 제조업체는 환경에 미치는 영향을 줄이면서 더 높은 운영 효율을 실현하는 추진 기술에 대한 투자를 확대되고 있습니다. 선박용 디젤 엔진은 추진력과 선내 발전 기능을 모두 제공함으로써, 여전히 전 세계 해운 산업에서 없어서는 안 될 핵심 요소로서의 역할을 수행하고 있습니다. 국제 무역량 증가, 해상 운송 네트워크의 확대, 그리고 새로운 항로의 개발이 계속해서 시장의 성장을 뒷받침하고 있습니다. 동시에 업계 관계자들은 연비 효율 향상과 차세대 추진 솔루션 도입 간의 균형을 모색하고 있습니다. 엔진 기술의 지속적인 발전으로 성능이 향상됨과 동시에, 보다 친환경적인 선박 운항으로의 전환이 촉진되고 있습니다. 또한, 해양 에너지 탐사 활동 증가와 온실가스 감축 노력에 대한 전 세계적인 관심이 높아짐에 따라, 예측 기간 동안 선박용 디젤 엔진 시장에 지속적인 성장 기회가 창출될 것으로 전망됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 51억 달러 |

| 예측 금액 | 68억 달러 |

| CAGR | 3.2% |

저속 선박용 디젤 엔진 시장은 2035년까지 30억 달러에 달할 것으로 전망됩니다. 이러한 엔진은 뛰어난 열효율과 다양한 연료로 가동할 수 있는 능력을 갖추고 있어, 대형 상선에서 여전히 최적의 선택지로 꼽히고 있습니다. 각 제조업체들은 환경 성능을 향상시키면서 대체 연료에도 대응할 수 있도록 이러한 시스템의 재설계를 적극적으로 추진하고 있습니다. 현재 진행 중인 기술 혁신은 연소 공정의 최적화, 연료 이용 효율 향상, 그리고 배기가스 저감에 중점을 두고 있습니다. 또한, 첨단 센서 기술, 실시간 모니터링 시스템 및 예측 유지보수 플랫폼의 통합으로 인해 이 부문 전체 수요가 가속화될 것으로 예측됩니다.

2025년 기준으로 상선 부문의 점유율은 35.7%를 차지했습니다. 시장 확대는 각국의 해상 역량 강화 및 상선단 현대화를 목적으로 한 투자 증가에 힘입고 있습니다. 세계 무역 활동의 활성화에 힘입어, 첨단 추진 시스템을 탑재한 상선에 대한 수요가 계속해서 증가세를 보이고 있습니다. 또한, 가처분 소득 증가와 해양 관광에 대한 관심 고조가 크루즈선 및 여객선 수요를 뒷받침하고 있습니다. 소비자들이 프리미엄 여행 경험을 선호하는 경향이 강해짐에 따라, 운항 사업자들은 기술적으로 선진적인 선박 솔루션에 대한 투자를 확대하고 있으며, 이는 해당 부문의 성장을 더욱 촉진하고 있습니다.

2025년 미국 선박용 디젤 엔진 시장 규모는 4억 8,050만 달러였습니다. 이 나라는 뛰어난 제조 능력, 주요 원자재에 대한 접근성, 그리고 비용 효율적인 생산 환경을 바탕으로 강력한 경쟁력을 유지하고 있습니다. 각 조선소에서 진행 중인 선박 현대화 및 개조 프로그램은 보다 친환경적이고 연료 효율이 높은 추진 기술을 도입할 수 있는 큰 기회를 창출하고 있습니다. 해운사들이 환경 및 운항 요건을 충족하기 위해 선단을 지속적으로 현대화함에 따라, 첨단 선박용 디젤 엔진에 대한 수요는 예측 기간 동안 견조한 추세를 보일 것으로 전망됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 기술별, 2022-2035년

제6장 시장 규모 및 예측 : 파워별, 2022-2035년

제7장 시장 규모 및 예측 : 용도별, 2022-2035년

제8장 시장 규모 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

JHS 26.07.01The Global Marine Diesel Engines Market was valued at USD 5.1 billion in 2025 and is estimated to grow at a CAGR of 3.2% to reach USD 6.8 billion by 2035.

The marine diesel engines market is experiencing significant transformation as the maritime industry intensifies efforts to reduce emissions, comply with increasingly stringent environmental regulations, and meet evolving stakeholder expectations. These changes are encouraging shipowners, vessel operators, and engine manufacturers to invest in propulsion technologies that deliver greater operational efficiency while lowering environmental impact. Marine diesel engines continue to serve as a vital component of global shipping operations by providing both propulsion and onboard power generation. Growing international trade volumes, expanding maritime transportation networks, and the development of new shipping corridors continue to support market growth. At the same time, industry participants are pursuing a balance between enhanced fuel efficiency and the adoption of next-generation propulsion solutions. Continuous advancements in engine technologies are improving performance while supporting the transition toward cleaner marine operations. In addition, increasing offshore energy exploration activities and a stronger global focus on greenhouse gas reduction initiatives are expected to create sustained growth opportunities for the marine diesel engines market throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.1 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 3.2% |

The low-speed marine diesel engines segment is anticipated to reach USD 3 billion by 2035. These engines remain the preferred choice for large commercial vessels due to their superior thermal efficiency and capability to operate on a variety of fuel types. Manufacturers are increasingly redesigning these systems to accommodate alternative fuel options while enhancing environmental performance. Ongoing technological innovation is focused on optimizing combustion processes, improving fuel utilization, and lowering emissions output. Furthermore, the integration of advanced sensor technologies, real-time monitoring systems, and predictive maintenance platforms is expected to accelerate demand across this segment.

The merchant vessel segment accounted for 35.7% share in 2025. Market expansion is supported by rising investments aimed at strengthening national maritime capabilities and modernizing commercial shipping fleets. Increased global trade activity continues to drive demand for merchant vessels equipped with advanced propulsion systems. Additionally, growing disposable incomes and rising interest in marine tourism are supporting demand for cruise and passenger vessels. Consumer preference for premium travel experiences has encouraged operators to invest in technologically advanced marine solutions, contributing further to segment growth.

U.S. Marine Diesel Engines Market was valued at USD 480.5 million in 2025. The country maintains a strong competitive position due to favorable manufacturing capabilities, access to key raw materials, and cost-efficient production environments. Ongoing vessel modernization and retrofit programs across shipyards are creating significant opportunities for the installation of cleaner and more fuel-efficient propulsion technologies. As maritime operators continue upgrading fleets to meet environmental and operational requirements, demand for advanced marine diesel engines is expected to remain strong throughout the forecast period.

Key participants operating in the global marine diesel engines market include AB Volvo, Cummins, Kawasaki Heavy Industries, Wartsila, Caterpillar, Rolls-Royce, HD Hyundai Heavy Industries Engine & Machinery, DEUTZ, Yanmar, Mitsubishi Heavy Industries, Scania, Anglo Belgian, Wabtec Corporation, Daihatsu Diesel, IHI Corporation, Deere & Company, STX Heavy Industries, Weichai India, Everllence, and Yuchai International. Companies operating in the marine diesel engines market are implementing a range of strategic initiatives to strengthen their market position and expand their competitive footprint. A primary focus area is investment in research and development to improve fuel efficiency, reduce emissions, and support compatibility with alternative fuels. Manufacturers are also incorporating digital technologies such as predictive maintenance, remote monitoring, and intelligent engine management systems to enhance operational performance and customer value. Strategic partnerships with shipbuilders, fleet operators, and technology providers are helping companies accelerate product deployment and market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Technology trends

- 2.1.3 Power trends

- 2.1.4 Application trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of marine diesel engines

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.10 Growth in untapped markets & applications

- 3.11 Investment analysis & future prospects

- 3.12 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.12.1 By region (Driven by Primary Research)

- 3.12.2 By technology (Driven by Primary Research)

- 3.13 Trade data analysis (Driven by Primary Research)

- 3.13.1 Import/export value trends (Driven by Primary Research)

- 3.13.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.14.1 AI-Driven production optimization (Driven by Primary Research)

- 3.14.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Low speed

- 5.3 Medium speed

- 5.4 High speed

Chapter 6 Market Size and Forecast, By Power, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 < 1,000 HP

- 6.3 1,000 - 5,000 HP

- 6.4 5,001 - 10,000 HP

- 6.5 10,001 - 20,000 HP

- 6.6 > 20,000 HP

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Merchant

- 7.2.1 Container vessels

- 7.2.2 Tankers

- 7.2.3 Bulk carriers

- 7.2.4 Gas carriers

- 7.2.5 RO-RO

- 7.2.6 Others

- 7.3 Offshore

- 7.3.1 Drilling rigs & ships

- 7.3.2 Anchor handling vessels

- 7.3.3 Offshore support vessels

- 7.3.4 Floating production units

- 7.3.5 Platform supply vessels

- 7.4 Cruise & ferry

- 7.4.1 Cruise vessels

- 7.4.2 Passenger vessels

- 7.4.3 Passenger/cargo vessels

- 7.4.4 Others

- 7.5 Navy

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Norway

- 8.3.6 Russia

- 8.3.7 Denmark

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.4.6 Vietnam

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 Iran

- 8.5.4 Angola

- 8.5.5 Egypt

- 8.5.6 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Mexico

Chapter 9 Company Profiles

- 9.1 AB Volvo

- 9.2 Anglo Belgian

- 9.3 Caterpillar

- 9.4 Cummins

- 9.5 Daihatsu Diesel

- 9.6 Deere & Company

- 9.7 DEUTZ

- 9.8 Everllence

- 9.9 HD Hyundai Heavy Industries Engine & Machinery

- 9.10 IHI Corporation

- 9.11 Kawasaki Heavy Industries

- 9.12 MITSUBISHI HEAVY INDUSTRIES

- 9.13 Rolls-Royce

- 9.14 Scania

- 9.15 STX Heavy Industries

- 9.16 Wabtec Corporation

- 9.17 Wartsila

- 9.18 Weichai India

- 9.19 Yanmar

- 9.20 Yuchai International