|

시장보고서

상품코드

2071322

공작기계 시장 : 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Machine Tools Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

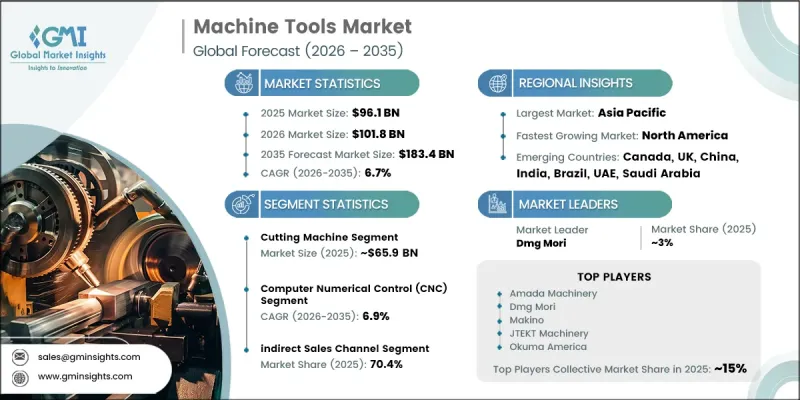

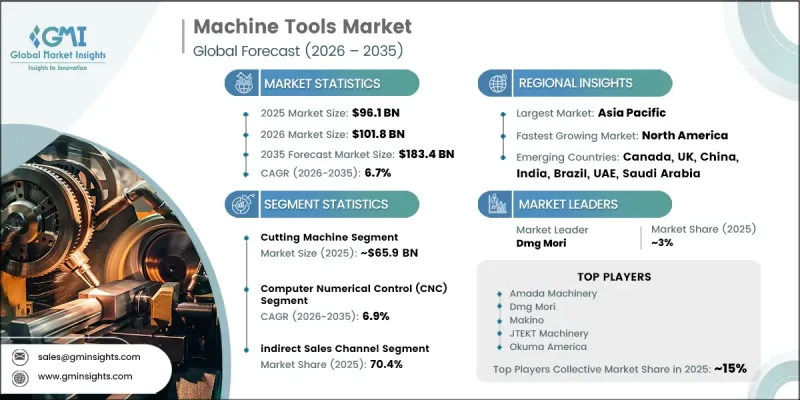

세계의 공작기계 시장은 2025년에 961억 달러 규모가 되어, 2035년까지 연평균 복합 성장률(CAGR) 6.7%로 성장하여 1,834억 달러에 이를 것으로 추정되고 있습니다.

이러한 성장은 신흥국의 산업 인프라가 급속히 발전하고, 아시아 및 라틴아메리카 전역에서 생산 생태계가 확대됨에 따라 강력한 뒷받침을 받고 있습니다. 정부 주도의 산업 진흥 프로그램은 국내 제조 역량을 증진하고, 해외 투자를 유치하며, 생산 경쟁력을 강화하고 있습니다. 자동차, 항공우주, 전자, 의료기기 등 주요 산업 분야 수요는 해당 분야에서 고정밀·고내구성이며 복잡한 부품이 요구됨에 따라 공작기계 도입을 더욱 가속화하고 있습니다. 공작기계는 현대 제조업에 필수적인 엄격한 공차, 정교한 형상, 우수한 표면 마감을 실현하는 데 있어 지극히 중요한 역할을 하고 있습니다. 고강도 합금이나 복합재료 등 첨단 소재의 사용이 증가하고 있는 점도, 가공이 어려운 소재를 다룰 수 있는 차세대 가공 기술에 대한 수요를 이끌고 있습니다. 자동화, 디지털 제조, 스마트 팩토리 환경으로의 전환은 효율성과 생산성을 한층 더 높여, 세계 산업 밸류체인에서 첨단 공작기계의 중요성을 더욱 부각시키고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 961억 달러 |

| 예측 금액 | 1,834억 달러 |

| CAGR | 6.7% |

절삭 가공기 부문은 2025년에 659억 달러 시장 규모를 기록하고, 2035년까지 연평균 성장률(CAGR) 7.3%로 성장할 것으로 전망됩니다. 이 부문은 밀링 가공, 선반 가공, 드릴링 가공, 연삭 가공 등 고정밀 제조 공정에 널리 활용되고 있어 계속해서 시장을 주도하고 있습니다. 이러한 시스템은 일관된 치수 정밀도, 고속 생산, 우수한 표면 품질을 실현하는 데 필수적입니다. 첨단 엔지니어링 소재의 채택 확대와 복잡한 형상의 부품에 대한 수요 증가가 이 부문의 성장을 더욱 뒷받침하고 있습니다.

간접 판매 채널은 2025년에 70.4%의 점유율을 차지하고, 2026년부터 2035년까지 연평균 성장률(CAGR) 7%로 성장할 것으로 전망됩니다. 이 채널이 여전히 주류를 이루는 이유는 제조업체가 유통업체, 딜러 및 제3자 공급업체를 통해 더 폭넓은 고객층, 특히 중소기업에 접근할 수 있기 때문입니다. 또한, 이러한 중개업체들은 고부가가치이며 기술적으로 정교한 공작기계에 필수적인 설치, 유지보수, 기술 교육, 사후 서비스 등의 중요한 서비스도 제공합니다.

미국의 공작기계 시장은 2025년에 211억 달러에 달하고, 2035년까지 연평균 성장률(CAGR) 6%로 성장할 것으로 전망됩니다. 항공우주, 자동차, 방위, 의료기기 제조 등 산업 분야의 견조한 수요가 시장의 꾸준한 성장을 이끌고 있습니다. CNC 자동화, 로봇 공학의 통합, IoT 대응 시스템 등 스마트 제조 기술의 도입이 확대됨에 따라 생산성과 조작 정밀도가 향상되고 있습니다. 현재 진행 중인 리쇼어링 노력과 국내 제조업에 대한 정부의 지원이 첨단 가공 솔루션에 대한 수요를 더욱 부추기고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기계 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 운영 기술별, 2022-2035년

제7장 시장 추산 및 예측 : 용도별, 2022-2035년

제8장 시장 추산 및 예측 : 최종 사용자별, 2022-2035년

제9장 시장 추산 및 예측 : 유통 채널별, 2022-2035년

제10장 시장 추산 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

JHS 26.07.01The Global Machine Tools Market was valued at USD 96.1 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 183.4 billion by 2035.

Growth is strongly supported by the rapid development of industrial infrastructure in emerging economies and the expansion of production ecosystems across Asia and Latin America. Government-backed industrial programs are encouraging domestic manufacturing capabilities, attracting foreign investment, and strengthening production competitiveness. Demand from core industries such as automotive, aerospace, electronics, and medical devices is further accelerating adoption, as these sectors require highly precise, durable, and complex components. Machine tools play a critical role in enabling tight tolerances, advanced geometries, and superior surface finishes essential for modern manufacturing. Increasing use of advanced materials such as high-strength alloys and composites is also driving demand for next-generation machining technologies capable of handling difficult-to-process inputs. The transition toward automation, digital manufacturing, and smart factory environments is further enhancing efficiency and productivity, reinforcing the importance of advanced machine tools in global industrial value chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $96.1 Billion |

| Forecast Value | $183.4 Billion |

| CAGR | 6.7% |

The cutting machine segment generated USD 65.9 billion in 2025 and is expected to grow at a CAGR of 7.3% through 2035. This segment continues to dominate due to its widespread use in high-precision manufacturing processes, including milling, turning, drilling, and grinding operations. These systems are essential for achieving consistent dimensional accuracy, high-speed production, and superior surface quality. Growing adoption of advanced engineering materials and increasing demand for complex part geometries are further strengthening segment expansion.

The indirect sales channel accounted for 70.4% share in 2025 and is projected to grow at a CAGR of 7% during 2026-2035. This channel remains dominant as distributors, dealers, and third-party suppliers enable manufacturers to reach a wider customer base, particularly small and medium enterprises. These intermediaries also provide essential services such as installation, maintenance, technical training, and after-sales support, which are critical for high-value and technologically advanced machine tools.

United States Machine Tools Market reached USD 21.1 billion in 2025 and is expected to grow at a CAGR of 6% through 2035. Strong demand from industries such as aerospace, automotive, defense, and medical equipment manufacturing is driving consistent market growth. Increasing adoption of smart manufacturing technologies, including CNC automation, robotics integration, and IoT-enabled systems, is improving productivity and operational precision. Ongoing reshoring initiatives and government support for domestic manufacturing are further reinforcing demand for advanced machining solutions.

Key companies operating in the global machine tools market include DMG MORI, Makino, Okuma, Haas Automation, DN Solutions (formerly Doosan Machine Tools), Amada, Hyundai WIA, Chiron Group, Komatsu, Georg Fischer, JTEKT Machinery, Hurco, Dalian Machine Tool Group, Amera-Seiki, Datron AG, Tsugami Corporation, Citizen Machinery, FFG Group (Fair Friend Group), Shenyang Machine Tool Co., SPINNER Werkzeugmaschinen, and Nakamura-Tome Precision Industry. Market participants are strengthening their competitive position through the rapid adoption of automation, digitalization, and smart manufacturing technologies. Companies are heavily investing in CNC systems, robotics integration, and AI-driven machining solutions to improve precision and operational efficiency. Expansion of product portfolios with multi-functional and high-speed machining centers is enhancing application coverage across industries. Strategic collaborations with automotive, aerospace, and industrial manufacturers are enabling long-term supply partnerships. Firms are also focusing on predictive maintenance capabilities and IoT-enabled machine tools to reduce downtime and improve productivity.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Machine type

- 2.2.3 Operating technology

- 2.2.4 Application

- 2.2.5 End use

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid industrialization and expansion of manufacturing sectors globally

- 3.2.1.2 Strong demand from automotive, aerospace, electronics, and medical device industries

- 3.2.1.3 Increasing need for high-precision and complex component manufacturing

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and capital costs associated with advanced machine tools

- 3.2.2.2 Rising costs of raw materials and components affecting manufacturing expenses

- 3.2.3 Opportunities

- 3.2.3.1 Growing adoption of Industry 4.0 and smart manufacturing solutions

- 3.2.3.2 Increasing demand for automation and robotics in production processes

- 3.2.3.3 Expansion of electric vehicle (EV) manufacturing and related components

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Trade data analysis (HS Code 8456)

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.8 Pricing analysis

- 3.8.1 Historical price trend analysis (driven by primary research)

- 3.8.2 Pricing strategy by player type (premium / value / mass market)

- 3.8.3 Price positioning of technology vs traditional products

- 3.8.4 Regional price variations

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machine Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Cutting machine

- 5.2.1 Milling machines

- 5.2.2 Turning machines

- 5.2.3 Grinding machines

- 5.2.4 Drilling machines

- 5.2.5 Others (threading, filling, etc.)

- 5.3 Forming machine

- 5.3.1 Presses

- 5.3.2 Bending machines

- 5.3.3 Punching machines

- 5.3.4 Others (rolling, forging, etc.)

Chapter 6 Market Estimates & Forecast, By Operating Technology, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Computer Numerical Control (CNC)

- 6.3 Conventional

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Metalworking

- 7.3 Woodworking

- 7.4 Plastic manufacturing

- 7.5 Others (ceramics & glass fabrication, composites working, etc.)

Chapter 8 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.3 Automotive

- 8.4 Energy & power

- 8.5 Electronics & semiconductors

- 8.6 Building & construction

- 8.7 Others (healthcare, marine, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 Amada (Amanda)

- 11.1.2 DMG MORI

- 11.1.3 Makino

- 11.1.4 Okuma

- 11.1.5 Haas Automation

- 11.1.6 Hyundai WIA

- 11.1.7 DN Solutions (formerly Doosan Machine Tools)

- 11.1.8 Georg Fischer

- 11.2 Regional Champions

- 11.2.1 JTEKT Machinery

- 11.2.2 Komatsu

- 11.2.3 Hurco

- 11.2.4 Chiron Group

- 11.2.5 Dalian Machine Tool Group

- 11.2.6 Amera-Seiki

- 11.2.7 Datron AG

- 11.3 Emerging Players

- 11.3.1 Tsugami Corporation

- 11.3.2 Citizen Machinery

- 11.3.3 FFG Group (Fair Friend Group)

- 11.3.4 Shenyang Machine Tool Co.

- 11.3.5 SPINNER Werkzeugmaschinen

- 11.3.6 Nakamura-Tome Precision Industry