|

시장보고서

상품코드

2071396

관절 재건 기기 시장 : 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Joint Reconstruction Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

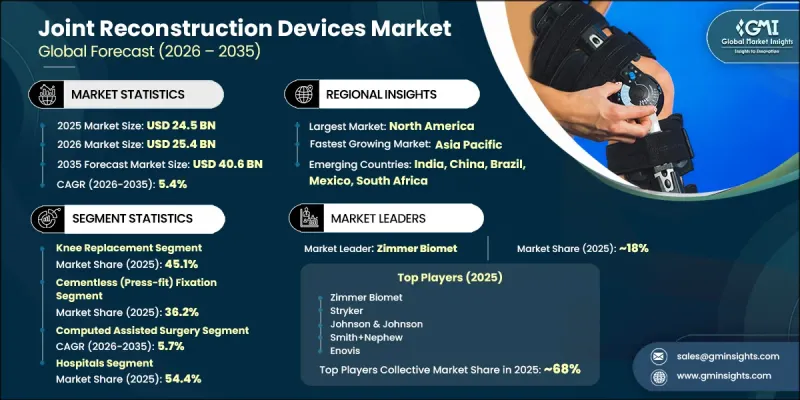

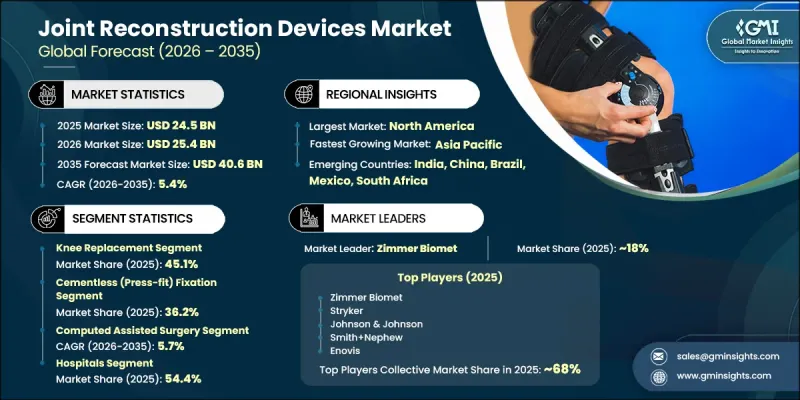

세계의 관절 재건 기기 시장은 2025년에 245억 달러로 평가되었고 CAGR 5.4%로 성장하여 2035년까지 406억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 근골격계 질환의 유병률 증가, 급속한 인구 고령화, 그리고 최소 침습 수술에 대한 선호도 증가에 힘입어 이루어지고 있습니다. 또한, 임플란트 기술과 수술 기법의 지속적인 발전으로 치료 성과가 향상되고 있으며, 이것이 시장 성장을 더욱 뒷받침하고 있습니다. 평균 수명의 연장에 따라 노화에 따른 관절 퇴행성 질환의 유병률이 높아지고 있으며, 이로 인해 관절 치환술에 대한 수요가 지속적으로 증가하고 있습니다. 또한, 비만율의 상승이나 신체 활동 증가와 같은 생활 습관과 관련된 요인들도 관절 손상 증가에 기여하고 있으며, 이로 인해 관절 재건 솔루션에 대한 수요가 높아지고 있습니다. 이 시장은 이동성을 개선하고 통증을 완화하며 환자의 삶의 질(QOL)을 전반적으로 향상시키는 수술에 대한 꾸준한 수요 덕분에 계속해서 혜택을 보고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 245억 달러 |

| 예측 금액 | 406억 달러 |

| CAGR | 5.4% |

관절 재건 기기는 손상된 관절(주로 무릎, 고관절, 어깨, 발목)을 복원하거나 대체하기 위해 설계된 정형외과용 임플란트입니다. 이러한 기기들은 퇴행성 관절 질환, 외상으로 인한 손상 및 기타 정형외과적 질환의 치료에 널리 사용되고 있습니다. 관절 퇴행 및 외상과 관련된 질환의 사례 수가 증가하고 있는 만큼, 이러한 임플란트에 대한 전 세계적인 수요는 계속해서 증가하고 있습니다. 평균 수명의 연장 및 만성 관절 질환으로 인한 부담의 증대가 재건 수술의 시행률 증가에 기여하는 주요 요인으로 작용하고 있습니다.

인공 슬관절 치환술 부문은 2025년에 45.1%의 시장 점유율을 차지했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 5.6%로 성장할 것으로 전망됩니다. 무릎 관련 질환, 특히 퇴행성 질환의 높은 발병률이 인공 슬관절 치환술에 대한 수요를 지속적으로 견인하고 있습니다. 이 수술은 다른 관절 재건 치료에 비해 관절 가동 범위 회복과 장기적인 불편 증상 완화에 효과적이기 때문에 널리 시행되고 있습니다.

시멘트 없는 고정 부문은 2025년에 36.2%의 시장 점유율을 차지했습니다. 이 부문의 성장은 자연스러운 골유착을 촉진하는 첨단 고정 기술의 도입 확대에 힘입고 있습니다. 이러한 임플란트는 장기적인 안정성을 높이고, 기존의 고정 방식에서 발생하는 합병증을 줄이도록 설계되어, 현대 정형외과 수술에서 선호되는 선택지가 되고 있습니다. 재료 과학 및 임플란트 설계의 지속적인 개선이 이 부문의 성장을 더욱 뒷받침하고 있습니다.

2025년, 북미의 관절 재건 기기 시장은 43.3%의 점유율을 차지했습니다. 이 지역의 활발한 수요는 관절 관련 질환의 높은 유병률과 잘 구축된 의료 인프라에 힘입어 견인되고 있습니다. 만성 정형외과 질환의 부담 증가와 첨단 치료 옵션에 대한 접근성 확대가 맞물려, 해당 지역 시장 성장을 지속적으로 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품 유형별(2022-2035년)

제6장 시장 추정 및 예측 : 고정 방식별(2022-2035년)

제7장 시장 추정 및 예측 : 외과 수술 유형별(2022-2035년)

제8장 시장 추정 및 예측 : 최종 용도별(2022-2035년)

제9장 시장 추정 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTHThe Global Joint Reconstruction Devices Market was valued at USD 24.5 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 40.6 billion by 2035.

Market expansion is driven by the increasing incidence of musculoskeletal conditions, a rapidly aging population, and the growing preference for minimally invasive surgical approaches. Continuous advancements in implant technologies and surgical procedures are also enhancing treatment outcomes, further supporting market growth. Rising life expectancy has led to a higher prevalence of age-related joint degeneration, which continues to fuel demand for joint replacement procedures. Additionally, lifestyle-related factors, including rising obesity levels and increased physical activity, are contributing to a growing number of joint injuries, thereby boosting the need for reconstruction solutions. The market continues to benefit from consistent demand for procedures that improve mobility, alleviate pain, and enhance overall patient quality of life.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.5 Billion |

| Forecast Value | $40.6 Billion |

| CAGR | 5.4% |

Joint reconstruction devices are orthopedic implants designed to repair or replace damaged joints, commonly involving the knee, hip, shoulder, and ankle. These devices are widely used in the treatment of degenerative joint conditions, injury-related damage, and other orthopedic disorders. Growing cases of joint deterioration and trauma-related conditions continue to accelerate global demand for these implants. Increased longevity and the rising burden of chronic joint disorders are key factors contributing to higher adoption rates of reconstruction procedures.

The knee replacement segment held a 45.1% share in 2025 and is expected to grow at a CAGR of 5.6% during 2026-2035. The high occurrence of knee-related conditions, particularly degenerative disorders, continues to drive demand for knee replacement procedures. These procedures are widely performed due to their effectiveness in restoring mobility and reducing long-term discomfort compared to other joint reconstruction treatments.

The cementless fixation segment held a share of 36.2% in 2025. Growth in this segment is supported by the increasing adoption of advanced fixation techniques that promote natural bone integration. These implants are designed to enhance long-term stability and reduce complications associated with traditional fixation methods, making them a preferred choice in modern orthopedic procedures. Continuous improvements in material science and implant design are further strengthening segment growth.

North America Joint Reconstruction Devices Market accounted for 43.3% share in 2025. Strong demand in this region is driven by the high prevalence of joint-related disorders and well-established healthcare infrastructure. The growing burden of chronic orthopedic conditions, combined with increased access to advanced treatment options, continues to support regional market expansion.

Key players in the global joint reconstruction devices market include Auxein, B. Braun, Conformis, Enovis, Exactech, Globus Medical, GPC Medical, Johnson & Johnson, Medacta International, Meril Life Sciences, MicroPort Scientific, NextStep Arthropedix, Smith+Nephew, Stryker, and Zimmer Biomet. Companies operating in the joint reconstruction devices industry are focusing on innovation, strategic partnerships, and product development to strengthen their competitive position. Investments in advanced implant technologies, including personalized and minimally invasive solutions, are helping improve surgical outcomes and patient satisfaction. Many players are expanding their global footprint through collaborations and distribution network enhancements. Additionally, companies are emphasizing research and development to introduce next-generation implants with improved durability and performance. Digital integration, including robotic-assisted surgeries and data-driven treatment planning, is also gaining traction. These strategies collectively enable companies to enhance their market presence and maintain long-term growth in a highly competitive environment.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Fixation type trends

- 2.2.4 Surgery type trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geriatric population

- 3.2.1.2 Rising incidence of sports-related injuries

- 3.2.1.3 Technological advancements

- 3.2.1.4 Need for personalized and patient specific implants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the devices

- 3.2.2.2 Stringent FDA regulations

- 3.2.2.3 Post-surgical complications

- 3.2.3 Market opportunities

- 3.2.3.1 Surging adoption of patient-specific and 3D-printed implants

- 3.2.3.2 Growing healthcare infrastructure investment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing trend analysis (Driven by primary research)

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.11 Value chain analysis (Driven by primary research)

- 3.12 Investment & funding analysis (Driven by primary research)

- 3.13 Consumer insights (Driven by primary research)

- 3.14 Treatment infrastructure & clinical adoption landscape

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Knee replacement devices

- 5.2.1 Primary knee systems

- 5.2.2 Partial knee systems

- 5.2.3 Revision knee systems

- 5.3 Hip replacement devices

- 5.3.1 Total hip replacement (THR) implants

- 5.3.2 Partial hip replacement (Hemiarthroplasty) implants

- 5.3.3 Hip resurfacing implants

- 5.3.4 Revision hip implants

- 5.4 Shoulder replacement devices

- 5.4.1 Total shoulder arthroplasty (TSA) implants

- 5.4.2 Reverse shoulder arthroplasty (RSA) implants

- 5.4.3 Partial shoulder replacement implants

- 5.5 Ankle replacement devices

- 5.5.1 Two-component fixed bearing

- 5.5.2 Three-component mobile bearing

- 5.6 Elbow replacement devices

- 5.6.1 Total elbow replacement

- 5.6.2 Partial elbow replacement

- 5.6.3 Revision elbow replacement

- 5.7 Other product types

Chapter 6 Market Estimates and Forecast, By Fixation Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Cemented fixation

- 6.3 Cementless (Press-Fit) fixation

- 6.4 Hybrid fixation

- 6.5 Reverse hybrid fixation

Chapter 7 Market Estimates and Forecast, By Surgery Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Traditional surgery

- 7.3 Minimally invasive Surgery

- 7.4 Computed assisted surgery

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Orthopedic specialty centers

- 8.4 Ambulatory surgical centers

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Auxein

- 10.2 B. Braun

- 10.3 Conformis

- 10.4 Enovis

- 10.5 Exactech

- 10.6 Globus Medical

- 10.7 GPC Medical

- 10.8 Johnson & Johnson

- 10.9 Medacta International

- 10.10 Meril Life Sciences

- 10.11 MicroPort Scientific

- 10.12 NextStep Arthropedix

- 10.13 Smith+Nephew

- 10.14 Stryker

- 10.15 Zimmer Biomet