|

시장보고서

상품코드

2071407

우주관광 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)Space Tourism Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

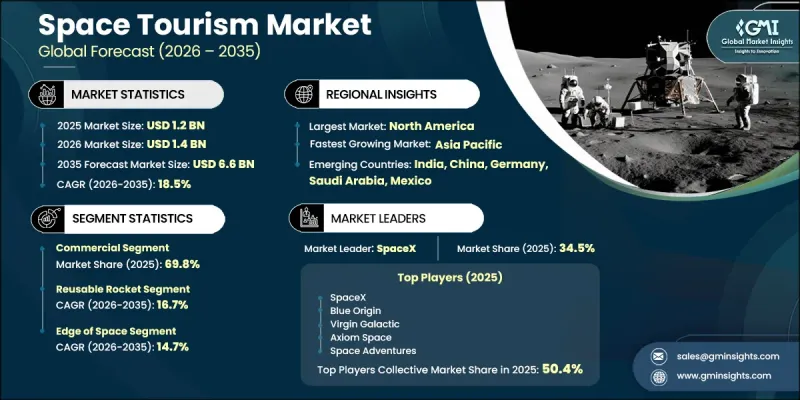

세계의 우주관광 시장은 2025년에 12억 달러 규모에 달하고, CAGR 18.5%로 성장하여 2035년에는 66억 달러에 달할 것으로 예측됩니다.

이 업계는 항공우주공학, 특히 재사용형 로켓과 차세대 우주선 개발 분야의 지속적인 발전에 힘입어 성장하고 있습니다. 이러한 혁신을 통해 운영 비용 절감, 안전 기준 향상, 상업 우주 여행의 신뢰성 제고가 이루어짐에 따라 상업적 실현 가능성이 높아지고, 더 많은 사람들이 이를 이용할 수 있게 되었습니다. 재사용형 로켓 시스템에 대한 민간 부문의 투자가 확대됨에 따라 발사 비용이 대폭 절감되는 동시에, 임무 수행 빈도와 운영 효율성이 향상되고 있습니다. 또한, 독점적이고 고급스러운 여행 경험을 추구하는 부유층의 관심이 높아지면서 시장 확대가 더욱 가속화되고 있습니다. 우주 여행은 배타성과 위신의 상징으로 점점 더 인식되고 있으며, 이것이 수요를 자극하고 업계의 성장을 지속적으로 뒷받침하고 있습니다. 재사용 기술의 발전으로 2020년 이후 발사 간격이 40% 단축되어, 비행 용량이 증가하고 관광 임무의 선택 폭이 넓어졌습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 12억 달러 |

| 예측 금액 | 66억 달러 |

| CAGR | 18.5% |

2025년에는 상업 부문이 시장 점유율의 69.8%를 차지했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 18.4%로 성장할 것으로 전망됩니다. 이 부문이 주도적인 위치를 차지하고 있는 것은 민간 사업자의 진출이 증가하고 있을 뿐만 아니라, 기존의 관광 서비스를 뛰어넘는 독특한 경험을 추구하는 부유층 여행객들의 수요가 높아지고 있기 때문입니다. 상업용 우주 서비스 제공업체들은 재사용 가능한 우주선 기술과 통합된 프리미엄 체험 모델을 기반으로 한 승객 중심의 서비스에 주력하고 있습니다. 민간 우주 기업 간의 경쟁이 치열해짐에 따라, 예약 기회가 확대되고 있으며, 고객 입장에서의 전반적인 이용 편의성이 향상되고 있습니다.

단기 체류 부문은 2025년에 65%의 점유율을 차지했으며, 2035년까지 연평균 성장률(CAGR) 15.1%로 성장할 것으로 전망됩니다. 이 부문이 주도적인 위치를 차지하고 있는 이유는 준비 기간이 짧고, 임무 계획이 간단하며, 참가 자격 요건이 폭넓기 때문입니다. 단기 체류 체험은 주로 첫 우주 여행을 하는 사람들을 대상으로 한 단시간의 준궤도 비행에 중점을 두고 있으며, 상업 우주관광으로의 더 쉬운 진입로를 제공하고 있습니다.

북미의 우주관광 시장은 2025년에 4억 5,930만 달러에 달했습니다. 이 지역은 확립된 항공우주 생태계, 강력한 민간 투자 유입, 그리고 상업용 유인 우주 비행 프로그램의 조기 도입을 통해 선도적인 위치를 유지하고 있습니다. 이 지역은 선진적인 발사 인프라, 지원적인 규제 체계, 그리고 재사용 가능한 발사 시스템과 우주 여행객 대상 서비스에 주력하는 주요 민간 우주 기업들의 존재로부터 혜택을 받고 있습니다. 우주선 기술의 지속적인 혁신과 상업용 비행 서비스의 꾸준한 개발이 이 지역의 성장을 더욱 뒷받침하고 있습니다.

세계 우주관광 업계에서 사업을 전개하는 주요 기업으로는 스페이스X(SpaceX), 블루 오리진(Blue Origin), 버진 갤럭틱(Virgin Galactic), 액시옴 스페이스(Axiom Space), 스페이스 어드벤처스(Space Adventures), 보잉(The Boeing Company), 에어버스(Airbus), 스페이스 퍼스펙티브(Space Perspective), 월드 뷰 엔터프라이즈(World View Enterprises) 등이 있습니다. 우주관광 시장의 각 기업은 임무 비용 절감과 비행 빈도 증대를 위해 재사용형 발사 기술 및 우주선 혁신에 막대한 투자를 단행하며, 적극적으로 입지를 강화하고 있습니다. 항공우주 공급업체 및 연구기관과의 전략적 제휴를 통해 개발 주기 단축과 안전 기준 향상이 뒷받침되고 있습니다. 각사는 부유층 고객을 위해 맞춤화된 준궤도 및 궤도 임무 등 차별화된 여행 경험을 도입함으로써 상업 비행 포트폴리오를 확대하고 있습니다. 또한, 많은 사업자들이 승객의 대비 태세와 안전성 확보를 강화하기 위해 첨단 훈련 인프라 및 시뮬레이션 시스템에 투자하고 있습니다. 마케팅 전략에서는 부유층 여행객을 유치하기 위해 배타성을 중시하는 브랜딩에 점점 더 중점을 두고 있습니다. 또한, 각사는 발사 운영을 위한 인프라를 확충하고, 고객의 접근성을 개선하기 위한 장기 예약 체계를 마련하고 있습니다. 우주 기관 및 민간 투자자와의 협력을 통해 자본 집약적인 프로젝트의 실현이 더욱 촉진되고 있는 한편, 추진 시스템 및 재사용 시스템에 대한 지속적인 연구 개발이 장기적인 비용 효율성과 시장 경쟁력을 확보하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 고도별, 2022-2035년

제6장 시장 추정 및 예측 : 차량별, 2022-2035년

제7장 시장 추정 및 예측 : 목적지별, 2022-2035년

제8장 시장 추정 및 예측 : 비행 시간별, 2022-2035년

제9장 시장 추정 및 예측 : 최종사용자별, 2022-2035년

제10장 시장 추정 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

KSMThe Global Space Tourism Market was valued at USD 1.2 billion in 2025 and is projected to grow at a CAGR of 18.5% to reach USD 6.6 billion in 2035.

The industry is propelled by continuous advancements in aerospace engineering, especially in reusable launch vehicles and next-generation spacecraft development. These innovations are reducing operational costs, improving safety standards, and enhancing the reliability of commercial space travel, making it more commercially viable and accessible. Growing private sector investment in reusable rocket systems is significantly lowering launch costs while increasing mission frequency and operational efficiency. Rising interest from high-net-worth individuals seeking exclusive and premium travel experiences is further accelerating market expansion. Space tourism is increasingly perceived as a symbol of exclusivity and prestige, which continues to stimulate demand and strengthen industry growth. Improvements in reusable technologies have also reduced launch turnaround times by 40% since 2020, enabling higher flight capacity and broader tourism mission availability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.2 Billion |

| Forecast Value | $6.6 Billion |

| CAGR | 18.5% |

The commercial segment accounted for 69.8% share in 2025 and is expected to grow at a CAGR of 18.4% from 2026 to 2035. This segment leads due to rising participation from private operators and increasing demand from wealthy travelers seeking unique experiences beyond conventional tourism offerings. Commercial providers are focusing on passenger-oriented services supported by reusable spacecraft technologies and integrated premium experience models. Increasing competition among private space companies is expanding booking opportunities and improving overall accessibility for customers.

The short-duration segment held a 65% share in 2025 and is projected to grow at a CAGR of 15.1% through 2035. This segment leads because it requires shorter preparation timelines, simpler mission planning, and broader customer eligibility. Short-duration experiences primarily focus on brief sub-orbital journeys designed for first-time space travelers, offering a more accessible entry point into commercial space tourism.

North America Space Tourism Market reached USD 459.3 million in 2025. The region maintains its leadership due to a well-established aerospace ecosystem, strong private investment inflows, and early adoption of commercial human spaceflight programs. It benefits from advanced launch infrastructure, supportive regulatory frameworks, and the presence of leading private space enterprises focused on reusable launch systems and astronaut tourism services. Continuous innovation in spacecraft technologies and sustained development of commercial flight offerings further reinforce regional growth.

The major companies operating in the Global Space Tourism Industry include SpaceX, Blue Origin, Virgin Galactic, Axiom Space, Space Adventures, The Boeing Company, Airbus, Space Perspective, and World View Enterprises. Companies in the space tourism market are actively strengthening their positions through heavy investment in reusable launch technologies and spacecraft innovation to reduce mission costs and improve flight frequency. Strategic partnerships with aerospace suppliers and research institutions are supporting faster development cycles and improved safety standards. Firms are expanding commercial flight portfolios by introducing differentiated travel experiences, including sub-orbital and orbital missions tailored to high-net-worth customers. Many players are also investing in advanced training infrastructure and simulation systems to enhance passenger readiness and safety assurance. Marketing strategies are increasingly focused on exclusivity-driven branding to attract affluent travelers. Additionally, companies are scaling infrastructure for launch operations and developing long-term booking frameworks to improve customer access. Collaboration with space agencies and private investors is further enabling capital-intensive projects, while continuous R&D in propulsion and reusable systems is ensuring long-term cost efficiency and market competitiveness.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Altitude

- 2.2.3 Vehicle

- 2.2.4 Destination

- 2.2.5 Flight Duration

- 2.2.6 End User

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements in aerospace innovation and efficiency.

- 3.2.1.2 Rising demand from affluent individuals seeking unique experiences.

- 3.2.1.3 Supportive government policies and partnerships.

- 3.2.1.4 Private sector investments fostering competition and innovation.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs inhibit widespread accessibility.

- 3.2.2.2 Limited infrastructure for space tourism operations.

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of private space stations enabling orbital accommodation and long duration tourism experiences.

- 3.2.3.2 Development of reusable spacecraft technology reducing launch costs and improving mission frequency.

- 3.2.3.3 Growth in near space tourism through high altitude balloon platforms and alternative flight systems.

- 3.2.3.4 Partnerships between aerospace companies and luxury travel providers creating integrated premium travel experiences.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 U.S. - Commercial Space Launch Competitiveness Act & FAA Space Tourism Regulations

- 3.6.1.2 Canada - Canadian Space Agency Licensing & Commercial Spaceflight Framework

- 3.6.2 Europe

- 3.6.2.1 Germany - German Aerospace Safety & EU Space Transportation Regulations

- 3.6.2.2 UK - UK Space Industry Act & Civil Aviation Authority Spaceflight Rules

- 3.6.2.3 France - French Space Operations Act & CNES Regulatory Framework

- 3.6.3 Asia Pacific

- 3.6.3.1 China - China National Space Administration Commercial Spaceflight Policies

- 3.6.3.2 India - IN-SPACe Commercial Spaceflight & Space Activities Regulations

- 3.6.3.3 Japan - Japanese Space Activities Act & JAXA Commercial Space Policies

- 3.6.4 Latin America

- 3.6.4.1 Brazil - Brazilian Space Agency Commercial Launch Regulations

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Arabia - Saudi Space Commission Space Tourism & Commercial Space Regulations

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 Gen AI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation intensity

Chapter 5 Market Estimates & Forecast, By Altitude, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Orbital

- 5.3 Sub-orbital

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Reusable Rocket

- 6.3 Spaceplane

- 6.4 High-Altitude Balloon

Chapter 7 Market Estimates & Forecast, By Destination, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Edge of Space

- 7.3 LEO/ISS

- 7.4 Private Station

- 7.5 Lunar Fly-By

Chapter 8 Market Estimates & Forecast, By Flight Duration, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Short-duration (mins-2hrs)

- 8.3 Extended (days-weeks)

Chapter 9 Market Estimates & Forecast, By End User, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Government

- 9.3 Commercial

- 9.4 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.4.8 Philippines

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 SpaceX

- 11.1.2 Blue Origin

- 11.1.3 Virgin Galactic

- 11.1.4 Axiom Space

- 11.1.5 Space Adventures

- 11.1.6 The Boeing Company

- 11.1.7 Airbus

- 11.1.8 Space Adventures

- 11.1.9 Space Perspective

- 11.1.10 World View Enterprises

- 11.2 Regional players

- 11.2.1 Sierra Space

- 11.2.2 Zero 2 Infinity

- 11.2.3 Zero Gravity

- 11.2.4 Starchaser Industries

- 11.2.5 Blue Abyss

- 11.2.6 HALO Space

- 11.2.7 Vast Space

- 11.2.8 Deep Blue Aerospace

- 11.2.9 PD AeroSpace

- 11.2.10 Orbite

- 11.2.11 Excalibur Almaz