|

시장보고서

상품코드

2071411

레이더 흡수 재료 시장 : 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Radar Absorbing Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

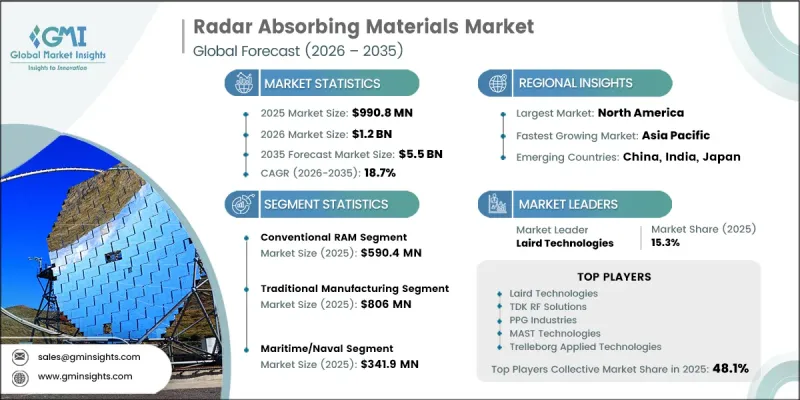

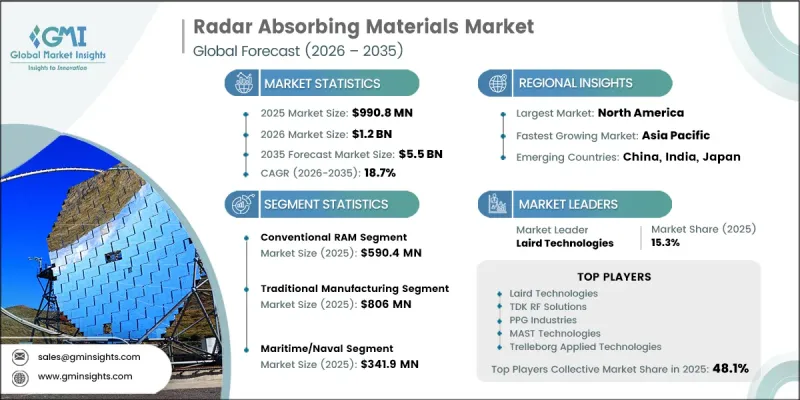

세계의 레이더 흡수 재료 시장은 2025년에 9억 9,080만 달러 규모로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 18.7%로 성장하여 55억 달러에 이를 것으로 추정되고 있습니다.

레이더 흡수 재료(RAM)는 주로 레이더 주파수 대역 내의 전자파를 흡수하여 레이더 신호의 반사를 줄이고, 이를 통해 감지 가능성을 낮추도록 설계된 특수한 공학 재료입니다. 이러한 재료는 입사하는 전자기 에너지를 열로 변환하거나, 유전 손실 및 자기 손실 메커니즘을 통해 재료 구조 내에서 소산시킴으로써 기능을 발휘합니다. RAM의 조성에는 일반적으로 전도성 폴리머, 페라이트, 탄소계 화합물 및 첨단 복합재료 블렌드가 포함되어 있어, 용도에 따른 요구 사항에 맞추어 성능을 맞춤 설정할 수 있습니다. 설계 요건에 따라, 이러한 재료는 코팅으로 도포되거나, 구조용 복합재료에 통합되거나, 적층 시트로 사용되거나, 또는 재료 시스템에 직접 내장될 수 있습니다. 주요 성능 요인으로는 동작 주파수 범위, 두께, 밀도, 환경 내구성 등이 있습니다. 다양한 산업 분야에서 전자기 간섭(EMI) 대책에 대한 요구가 높아짐에 따라, 레이더 흡수 재료에 대한 수요가 증가하고 있습니다. 현재 그 용도는 방위 분야뿐만 아니라 통신, 자동차용 전자기기, 전자 차폐 시스템까지 확대되고 있습니다. 전자 플랫폼이 점점 더 복잡해짐에 따라 전자기 시그니처를 관리해야 할 필요성이 커지고 있으며, 이것이 더 광범위한 도입을 촉진하고 있습니다. 또한, 항공우주 및 운송 시스템 분야에서 경량 복합재 구조의 활용 확대도 성장을 뒷받침하고 있으며, 이러한 시스템에서는 흡수 기능을 통합함으로써 구조물의 무게를 늘리지 않고도 성능을 향상시킬 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 9억 9,080만 달러 |

| 예측 금액 | 55억 달러 |

| CAGR | 18.7% |

2025년 기준으로, 기존 레이더 흡수 소재 시장 규모는 5억 9,040만 달러였습니다. 이러한 소재들은 확립된 제조 공정과 특정 주파수 대역에서 보여주는 안정적인 성능 덕분에 계속해서 널리 채택되고 있습니다. 기존 RAM(레이더 흡수재)의 배합에는 일반적으로 페라이트, 탄소계 폴리머 및 코팅 시스템이 사용되고 있으며, 성능 향상을 위해 지속적으로 개량이 이루어지고 있습니다. 현재 진행 중인 기술 개발은 특히 신뢰성과 비용 효율성이 여전히 최우선 과제인 항공우주 및 방위 분야에서 내구성, 내환경성 및 시공 효율의 향상에 중점을 두고 있습니다.

기존 제조 공정은 2025년에 8억 600만 달러 규모 시장을 차지했습니다. 이러한 방법은 확장성, 운영 안정성 및 대량 생산에의 적합성 덕분에 널리 활용되고 있습니다. 코팅, 성형, 적층과 같은 확립된 기술은 폭넓은 용도에서 일관된 제품 품질을 지속적으로 보장하고 있습니다. 동시에, 정밀도, 효율 및 재료 성능을 향상시키기 위해 새로운 하이브리드 방식과 첨단 제조 기법이 점차 도입되고 있습니다. 업계 동향으로는 기존의 제조 기술이 여전히 기반을 이루고 있는 한편, 진화하는 기술적·설계적 요건을 충족하기 위해 첨단 공정이 점점 더 통합되어 가는 단계적인 전환이 나타나고 있습니다.

북미의 레이더 흡수 재료 시장은 2025년 3억 6,130만 달러에서 2035년까지 22억 달러로 성장할 것으로 예측됩니다. 이 지역 시장 확대는 방위 시스템의 지속적인 현대화, 항공우주 프로그램의 발전, 그리고 전자·통신 시스템 전반에 걸친 전자기 호환성(EMC)에 대한 중요성이 커짐에 따라 주도되고 있습니다. 미국에서는 차세대 방위 플랫폼 및 항공우주 기술에 대한 지속적인 투자가 여러 고성능 용도에서 레이더 흡수재의 보다 광범위한 도입을 뒷받침하고 있으며, 이로 인해 해당 지역의 장기적인 시장 성장을 가속하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 소재 유형별(2022-2035년)

제6장 시장 추정 및 예측 : 제조 방법별(2022-2035년)

제7장 시장 추정 및 예측 : 주파수대별(2022-2035년)

제8장 시장 추정 및 예측 : 용도별(2022-2035년)

제9장 시장 추정 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTH 26.07.03The Global Radar Absorbing Materials Market was valued at USD 990.8 million in 2025 and is estimated to grow at a CAGR of 18.7% to reach USD 5.5 billion by 2035.

Radar absorbing materials (RAM) are specialized engineered substances designed to reduce radar signal reflection by absorbing electromagnetic waves, primarily within radar frequency ranges, thereby lowering detectability. These materials function by converting incoming electromagnetic energy into heat or dissipating it within the material structure through dielectric and magnetic loss mechanisms. RAM formulations typically incorporate conductive polymers, ferrites, carbon-based compounds, and advanced composite blends, enabling performance customization based on application needs. Depending on design requirements, these materials can be applied as coatings, integrated into structural composites, used as layered sheets, or embedded directly into material systems. Key performance factors include operating frequency range, thickness, density, and environmental durability. Demand for radar absorbing materials is rising due to increasing requirements for electromagnetic interference control across multiple industries. Their applications now extend beyond defense into telecommunications, automotive electronics, and electronic shielding systems. As electronic platforms become more complex, the need to manage electromagnetic signatures has intensified, supporting broader adoption. Growth is also supported by rising use of lightweight composite structures in aerospace and transportation systems, where embedded absorption capabilities help improve performance without increasing structural weight.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $990.8 Million |

| Forecast Value | $5.5 Billion |

| CAGR | 18.7% |

Conventional radar absorbing materials accounted for USD 590.4 million in 2025. These materials continue to be widely adopted due to their established manufacturing processes and consistent performance across specific frequency ranges. Traditional RAM formulations commonly rely on ferrites, carbon-based polymers, and coating systems that are continuously being refined for improved performance. Ongoing advancements are focused on enhancing durability, environmental resistance, and application efficiency, particularly in aerospace and defense environments where reliability and cost efficiency remain critical priorities.

The traditional manufacturing processes represented a USD 806 million in 2025. These methods are widely used due to their scalability, operational stability, and suitability for high-volume production. Established techniques such as coating application, molding, and lamination continue to ensure consistent output quality across a broad range of applications. At the same time, newer hybrid and advanced manufacturing approaches are gradually being introduced to improve precision, efficiency, and material performance. The industry trend indicates a gradual transition where conventional manufacturing remains foundational while advanced processes are increasingly integrated to meet evolving technical and design requirements.

North America Radar Absorbing Materials Market is expected grow from USD 361.3 million in 2025 to USD 2.2 billion by 2035. Regional expansion is being driven by continuous modernization of defense systems, advancement in aerospace programs, and rising emphasis on electromagnetic compatibility across electronic and communication systems. In the United States, ongoing investments in next-generation defense platforms and aerospace technologies are supporting broader integration of radar absorbing materials across multiple high-performance applications, strengthening long-term market growth in the region.

Major companies operating in the global radar absorbing materials market include Saab AB, PPG Industries, TDK RF Solutions, Echodyne Inc., Kymeta Corporation, Laird Technologies, Trelleborg, Armorthane, Hyper Stealth Technologies Pvt. Ltd, MAJR Products, MWT Materials Inc., Soliani EMC, Diamond Microwave Chambers Ltd, SLTL Group, Wittenburg Group, MAST Technologies, RF Nanocomposites Pvt. Ltd, Dutch Microwave Absorber Solutions, Fractal Antenna Systems, and JEM Engineering. Companies operating in the radar absorbing materials market are focusing on strengthening their competitive position through continuous material innovation, advanced composite development, and performance optimization across wider frequency ranges. Significant investment is being directed toward research and development aimed at improving absorption efficiency, thermal stability, and environmental durability of materials used in defense and aerospace applications. Market participants are also expanding production capabilities through the scaling of advanced manufacturing technologies while maintaining conventional production lines for established applications. Strategic collaborations with defense contractors, aerospace manufacturers, and telecommunications providers are helping companies secure long-term supply agreements and expand application reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material Type

- 2.2.2 Manufacturing Method

- 2.2.3 Frequency Band

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Defense modernization and stealth platform demand

- 3.2.1.2 Miniaturization, weight reduction and multi-functional material integration

- 3.2.1.3 5G/6G infrastructure build-out and EMI shielding demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing cost and yield challenges for metamaterial-based RAM

- 3.2.2.2 Export control and ITAR/EAR compliance as market access barriers

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing demand for stealth defense technologies

- 3.2.3.2 Growing use in advanced electronic shielding

- 3.2.3.3 Expansion in aerospace composite material applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Conventional RAM

- 5.2.1 RAM Paints & Coatings

- 5.2.1.1 X-band RAM Paint

- 5.2.1.2 Other Frequency Band RAM Paints

- 5.2.2 RAM Sheets & Panels

- 5.2.3 RAM Foams

- 5.2.4 RAM Fillers

- 5.2.5 Others

- 5.2.1 RAM Paints & Coatings

- 5.3 Metamaterial-Based RAM

- 5.3.1 Split Ring Resonator (SRR) based

- 5.3.2 Wire Array based

- 5.3.3 Frequency Selective Surface (FSS) based

- 5.3.4 Others

Chapter 6 Market Estimates and Forecast, By Manufacturing Method, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Lithographic Techniques

- 6.3 3D Printing/Additive Manufacturing

- 6.4 Traditional Manufacturing

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Frequency Band, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 X-band (8-12 GHz)

- 7.2.1 Conventional RAM

- 7.2.2 Metamaterial-Based RAM

- 7.3 S-band (2-4 GHz)

- 7.3.1 Conventional RAM

- 7.3.2 Metamaterial-Based RAM

- 7.4 L-band (1-2 GHz)

- 7.4.1 Conventional RAM

- 7.4.2 Metamaterial-Based RAM

- 7.5 C-band (4-8 GHz)

- 7.5.1 Conventional RAM

- 7.5.2 Metamaterial-Based RAM

- 7.6 Ku-band (12-18 GHz)

- 7.6.1 Conventional RAM

- 7.6.2 Metamaterial-Based RAM

- 7.7 Ka-band (26-40 GHz)

- 7.7.1 Conventional RAM

- 7.7.2 Metamaterial-Based RAM

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Maritime/Naval

- 8.2.1 Ship Navigation Radar

- 8.2.1.1 Conventional RAM

- 8.2.1.2 Metamaterial-Based RAM

- 8.2.2 Naval Vessels

- 8.2.3 Others

- 8.2.1 Ship Navigation Radar

- 8.3 Aerospace & Defense

- 8.3.1 Conventional RAM

- 8.3.2 Metamaterial-Based RAM

- 8.4 Automotive

- 8.4.1 Conventional RAM

- 8.4.2 Metamaterial-Based RAM

- 8.5 Telecommunications

- 8.5.1 Conventional RAM

- 8.5.2 Metamaterial-Based RAM

- 8.6 Electronics

- 8.6.1 Conventional RAM

- 8.6.2 Metamaterial-Based RAM

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Laird Technologies

- 10.2 Soliani EMC

- 10.3 MWT Materials Inc

- 10.4 Diamond Microwave Chambers Ltd

- 10.5 MAJR Products

- 10.6 SLTL Group

- 10.7 Trelleborg

- 10.8 Wittenburggroup

- 10.9 Armorthane

- 10.10 Hyper Stealth Technologies Pvt. Ltd

- 10.11 PPG Industries

- 10.12 MAST Technologies

- 10.13 RF Nanocomposites Pvt. Ltd

- 10.14 Echodyne Inc.

- 10.15 Dutch Microwave Absorber Solutions

- 10.16 Fractal Antenna Systems

- 10.17 TDK RF Solutions

- 10.18 Saab AB

- 10.19 Kymeta Corporation

- 10.20 JEM Engineering