|

시장보고서

상품코드

2083051

순항 미사일 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Cruise Missile Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

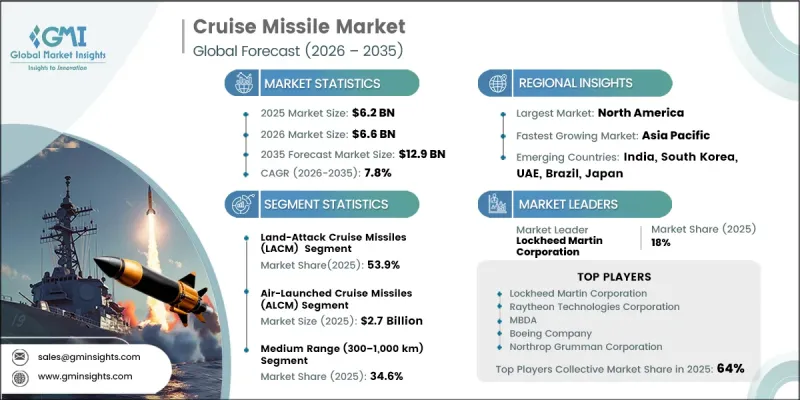

세계의 순항 미사일 시장은 2025년에 62억 달러로 평가되었고, CAGR 7.8%로 성장하여 2035년까지 129억 달러에 달할 것으로 예측됩니다.

시장 성장은 정밀 유도형 장거리 공격 능력에 대한 수요 증가, 첨단 방어 시스템의 배치 확대, 해군 현대화 계획의 추진, 그리고 국내 미사일 개발 프로그램에 대한 투자 확대에 힘입어 이루어지고 있습니다. 전 세계의 국방 기관들은 작전상 안전 거리를 유지하면서, 인력과 군사 플랫폼에 대한 위험을 최소화하고 전략적 목표를 공격할 수 있는 첨단 공격 기술에 점점 더 중점을 두고 있습니다. 정밀 전술의 중요성이 커지고, 끊임없이 변화하는 안보 과제가 조달 활동을 가속화하며, 첨단 미사일 시스템에 대한 장기적인 투자를 뒷받침하고 있습니다. 또한, 해상 안보 요건의 확대와 해군 함대의 현대화에 따라 해상 공격 능력에 대한 수요가 크게 증가하고 있습니다. 방위 분야의 자급자족, 기술 발전, 전략적 억지력에 대한 지속적인 노력이 시장 확대에 더욱 기여하고 있습니다. 군가 작전 준비 태세를 강화하고 정밀 타격 능력을 향상시키려는 가운데, 전 세계 국방비의 지속적인 지출과 현대화 프로그램에 힘입어 순항 미사일 시장은 향후 10년 동안 강력한 성장세를 유지할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 개시연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 62억 달러 |

| 예측액 | 129억 달러 |

| CAGR | 7.8% |

2025년에는 지상 공격용 순항 미사일 부문이 시장 점유율의 53.9%를 차지했습니다. 이 부문이 주도적인 위치를 차지하고 있는 것은 현대의 정밀 타격 작전이나 장거리 교전 전략에서 지극히 중요한 역할을 수행하고 있기 때문입니다. 이러한 미사일 시스템은 군에 원거리에서 방어 체계가 구축된 전략적으로 중요한 목표물을 정밀 타격할 수 있는 능력을 제공하며, 작전 중 발사 플랫폼이 피격될 위험을 줄여줍니다. 여러 군사 플랫폼에 걸친 폭넓은 배치 호환성과 범용성이 높은 임무 수행 능력에 대한 수요가 증가함에 따라, 이 부문의 강력한 성장이 계속해서 뒷받침되고 있습니다.

300-1,000킬로미터의 사거리를 커버하는 중거리 부문은 2025년에 34.6%의 시장 점유율을 차지했습니다. 이 부문은 작전상의 효과성, 배치의 유연성, 그리고 조달 비용의 합리성 사이에서 균형을 잘 맞추고 있다는 점이 강점입니다. 중거리 시스템은 전술적 타격 임무, 지역 억제 작전 및 해상 교전 요건에 폭넓게 활용되고 있으며, 많은 국방 기관에 있어 선호되는 선택지가 되고 있습니다. 비용 효율성을 유지하면서도 실효성 있는 원거리 대응 능력을 제공할 수 있다는 점이 계속해서 조달 활동을 촉진하고, 해당 부문의 성장을 뒷받침하고 있습니다.

북미의 순항 미사일 시장은 2025년에 37.6%의 점유율을 기록하며 최대 지역 시장으로서의 위상을 유지했습니다. 이 지역의 성장은 장거리 공격 능력의 현대화, 첨단 방위 기술, 그리고 군사 능력 강화 프로그램에 대한 지속적인 투자를 바탕으로 이루어지고 있습니다. 수요는 광범위한 미사일 범주와 군사 용도에 걸쳐 있으며, 고도로 발달한 방위 산업 기반, 대규모 조달 프로그램, 그리고 지속적인 현대화 노력에 의해 뒷받침되고 있습니다. 강력한 연구개발 역량, 선진적인 제조 인프라, 그리고 장기적인 국방 투자 전략이 세계 순항 미사일 산업에서 북미의 주도적 위치를 지속적으로 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 미사일 유형별, 2022년-2035년

제6장 시장 추산 및 예측 : 탄두 유형별, 2022년-2035년

제7장 시장 추산 및 예측 : 발사 플랫폼별, 2022년-2035년

제8장 시장 추산 및 예측 : 범위별, 2022년-2035년

제9장 시장 추산 및 예측 : 속도별, 2022년-2035년

제10장 시장 추산 및 예측 : 지역별, 2022년-2035년

제11장 기업 개요

LSH 26.07.13The Global Cruise Missile Market was valued at USD 6.2 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 12.9 billion by 2035.

Market growth is driven by rising demand for precision-guided long-range strike capabilities, increasing deployment of sophisticated defense systems, expanding naval modernization initiatives, and growing investments in domestic missile development programs. Defense organizations across the world are placing greater emphasis on advanced strike technologies that enable engagement of strategic targets while maintaining operational stand-off distances and minimizing risks to personnel and military platforms. The growing importance of precision warfare and evolving security challenges are accelerating procurement activities and supporting long-term investment in advanced missile systems. In addition, expanding maritime security requirements and the modernization of naval fleets are generating significant demand for sea-based strike capabilities. Continued focus on defense self-sufficiency, technological advancement, and strategic deterrence is further contributing to market expansion. As military forces seek to strengthen operational readiness and enhance precision engagement capabilities, the cruise missile market is expected to maintain a strong growth trajectory over the coming decade, supported by sustained defense spending and modernization programs worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.2 Billion |

| Forecast Value | $12.9 Billion |

| CAGR | 7.8% |

The land-attack cruise missiles segment accounted for 53.9% share in 2025. The segment's dominance is attributed to its critical role in modern precision-strike operations and long-range engagement strategies. These missile systems provide armed forces with the ability to accurately engage protected and strategically important targets from extended distances, reducing the exposure of launch platforms during operations. Broad deployment compatibility across multiple military platforms and increasing demand for versatile mission capabilities continue to support strong growth within this segment.

The medium-range segment, covering distances between 300 and 1,000 kilometers, held a 34.6% share in 2025. The segment benefits from its balance of operational effectiveness, deployment flexibility, and procurement affordability. Medium-range systems are widely utilized for tactical strike missions, regional deterrence operations, and maritime engagement requirements, making them a preferred choice for many defense organizations. Their ability to provide meaningful stand-off capability while maintaining cost efficiency continues to drive procurement activity and support segment growth.

North America Cruise Missile Market accounted for 37.6% share in 2025, maintaining its position as the largest regional market. Regional growth is supported by ongoing investments in long-range strike modernization, advanced defense technologies, and military capability enhancement programs. Demand spans a broad range of missile categories and military applications, supported by a highly developed defense industrial base, extensive procurement programs, and continuous modernization initiatives. Strong research and development capabilities, advanced manufacturing infrastructure, and long-term defense investment strategies continue to reinforce North America's leadership within the global cruise missile industry.

Leading companies operating in the global cruise missile market include MBDA, Raytheon Technologies Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, Boeing Company, Kongsberg Defence & Aerospace AS, Rafael Advanced Defense Systems Ltd., BrahMos Aerospace Pvt. Ltd., Roketsan A.S., Israel Aerospace Industries, China Aerospace Science and Industry Corporation (CASIC), LIG Nex1, Elbit Systems, and Avibras Industria Aeroespacial S/A. Companies participating in the cruise missile market are implementing a range of strategic initiatives to strengthen their competitive position and expand market presence. Significant investments in research and development remain a primary focus, enabling manufacturers to improve guidance systems, propulsion technologies, precision targeting capabilities, and overall operational effectiveness. Strategic partnerships, defense collaborations, and joint development programs are helping companies accelerate innovation while securing access to new procurement opportunities. Many market participants are also emphasizing indigenous production capabilities and technology localization to address growing demand for defense self-reliance. Product portfolio diversification, modernization of existing missile platforms, and integration of advanced digital technologies are further supporting competitive differentiation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Missile type trends

- 2.2.2 Warhead type trends

- 2.2.3 Launch platform trends

- 2.2.4 Range trends

- 2.2.5 Speed trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV adoption increasing IGBT and SiC demand

- 3.2.1.2 Industrial automation growth raising demand for power modules

- 3.2.1.3 Energy efficiency regulations mandating advanced power electronics

- 3.2.1.4 Data center power optimization increasing MOSFET consumption

- 3.2.1.5 Fast-charging infrastructure expansion boosting wide-bandgap semiconductors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing cost of SiC and GaN devices

- 3.2.2.2 Supply chain dependence on limited wafer suppliers

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of SiC in 800V electric vehicle platforms

- 3.2.3.2 Smart grid upgrades increasing demand for high-power discrete devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price Analysis (Driven by Primary Research)

- 3.8.1 Historical Price Analysis (2022-2025)

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.9.1 AI-Driven Disruption of Existing Business Models

- 3.9.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.9.3 Risks, Limitations & Regulatory Considerations

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Company market share analysis, 2025

- 4.1.1 By Region

- 4.1.1.1 North America

- 4.1.1.2 Europe

- 4.1.1.3 Asia-Pacific

- 4.1.1.4 Latin America

- 4.1.1.5 Middle East and Africa

- 4.1.2 Market Concentration Analysis

- 4.1.1 By Region

- 4.2 Competitive analysis of major market players

- 4.3 Competitive positioning matrix

- 4.3.1 Key developments

- 4.3.2 Mergers & acquisitions

- 4.3.3 Partnerships & collaborations

- 4.3.4 New product launches

- 4.3.5 Expansion plans and funding

- 4.4 Company tier benchmarking

- 4.4.1 Tier classification criteria & qualifying thresholds

- 4.4.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Missile Type, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Land-attack cruise missiles (LACM)

- 5.3 Anti-ship cruise missiles (ASCM)

- 5.4 Anti-surface cruise missiles (dual land/sea)

Chapter 6 Market Estimates and Forecast, By Warhead Type, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Nuclear

Chapter 7 Market Estimates and Forecast, By Launch Platform, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Air-launched (ALCM)

- 7.3 Sea-launched (SLCM)

- 7.4 Ground-launched (GLCM)

Chapter 8 Market Estimates and Forecast, By Range, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Short range (< 300 km)

- 8.3 Medium range (300-1,000 km)

- 8.4 Long-range (1,000-2,500 km)

- 8.5 Very long-range (> 2,500 km)

Chapter 9 Market Estimates and Forecast, By Speed, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Subsonic

- 9.3 Supersonic

- 9.4 Hypersonic

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Lockheed Martin Corporation

- 11.1.2 Raytheon Technologies Corporation

- 11.1.3 MBDA

- 11.1.4 Boeing Company

- 11.1.5 Northrop Grumman Corporation

- 11.2 Regional key players

- 11.2.1 Asia Pacific

- 11.2.1.1 BrahMos Aerospace Pvt. Ltd.

- 11.2.1.2 China Aerospace Science and Industry Corporation (CASIC)

- 11.2.2 Europe

- 11.2.2.1 Kongsberg Defence & Aerospace AS

- 11.2.3 Middle East & Africa

- 11.2.3.1 Roketsan A.S.

- 11.2.3.2 Rafael Advanced Defense Systems Ltd.

- 11.2.3.3 Israel Aerospace Industries

- 11.2.1 Asia Pacific

- 11.3 Niche Players/Disruptors

- 11.3.1 Avibras Industria Aeroespacial S/A

- 11.3.2 LIG Nex1

- 11.3.3 Elbit Systems