|

시장보고서

상품코드

2083077

온실 환기 시스템 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Greenhouse Ventilation Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

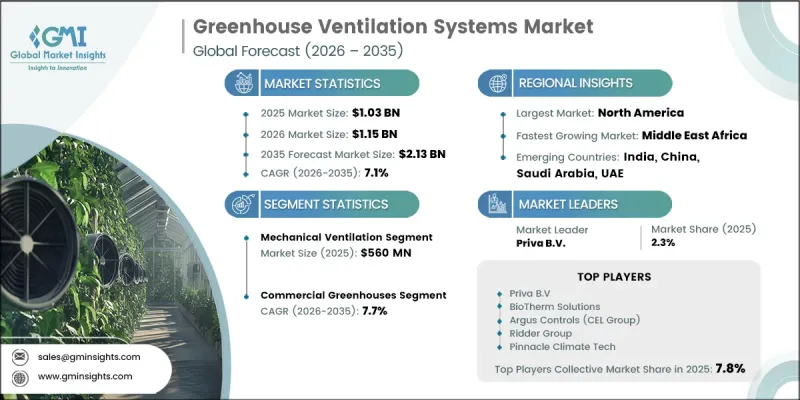

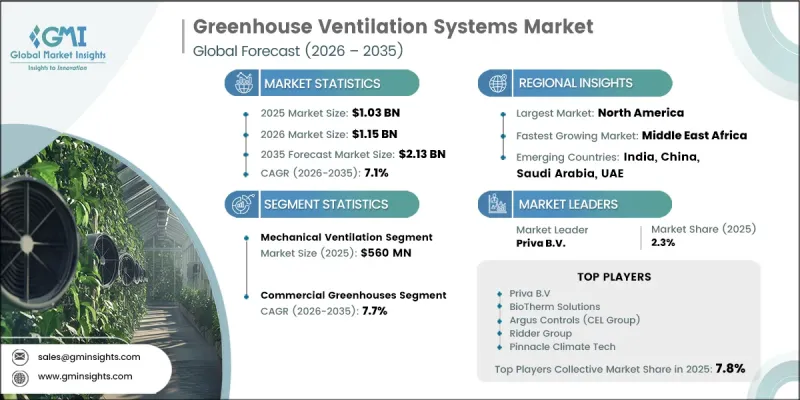

세계의 온실 환기 시스템 시장은 2025년에 10억 3,000만 달러로 평가되었고, CAGR 7.1%로 성장하여 2035년까지 21억 3,000만 달러에 달할 것으로 예측됩니다.

시장 확대는 선진적인 환경 관리 시스템을 통해 온실의 생산성을 극대화하고, 자원 활용을 최적화하며, 작물의 품질을 향상시키는 데 대한 관심이 높아짐에 따라 주도되고 있습니다. 환기 기술은 온실 구조 내의 온도, 습도, 공기 순환 및 대기 균형을 조절함으로써 이상적인 재배 조건을 유지하는 데 매우 중요한 역할을 합니다. 지속 가능한 농업 관행, 식품 품질 기준, 그리고 기후 변화에 강한 재배 방법에 대한 관심이 높아지고 있는 점도 현대적인 온실 인프라에 대한 수요를 더욱 부추기고 있습니다. 기술의 발전으로 인해 온실 운영 방식이 크게 변화하여, 자동화가 진전되고 감시 능력이 향상되었으며, 더욱 정밀한 기후 관리가 가능해졌습니다. 농업 현대화를 위한 노력과 지속가능성에 중점을 둔 재배 프로그램에 대한 정부의 지원도 시장 성장에 기여하고 있습니다. 소규모 생산자들에게는 설치 비용이 여전히 과제로 남아 있지만, 대규모 온실 프로젝트, 보호 재배 시스템 및 첨단 농업 시설에 대한 투자가 증가함에 따라 온실 환기 시스템 시장 전체에 걸쳐 계속해서 큰 성장 기회가 창출되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 10억 3,000만 달러 |

| 예측액 | 21억 3,000만 달러 |

| CAGR | 7.1% |

기계 환기 부문은 2025년에 5억 6,000만 달러 시장 규모를 기록했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 7.1%로 성장할 것으로 전망됩니다. 이 부문은 다양한 재배 조건 하에서도 안정적인 성능, 정확한 환경 제어, 그리고 신뢰성 높은 운영을 실현할 수 있기 때문에 선도적인 위치를 유지하고 있습니다. 수동적인 기류 방식과 달리, 기계식 시스템은 온실 내 환경을 능동적으로 조절하기 때문에 생산자는 외부 기상 변화에 관계없이 안정적인 온도, 습도 및 대기 조건을 유지할 수 있습니다. 제어 환경 농업(CEA)의 운영을 지원하고, 첨단 온실 인프라와 원활하게 통합될 수 있는 능력 덕분에, 생산성 향상과 작물 품질의 안정성을 추구하는 상업적 생산자들 사이에서 기계식 환기 시스템은 선호되는 선택지가 되고 있습니다. 자동화 및 기후 제어 기술에 대한 지속적인 투자로 인해, 예측 기간 동안 기계식 환기 솔루션에 대한 수요가 더욱 증가할 것으로 예측됩니다.

상업 부문은 2025년에 56.86%의 점유율을 차지했으며, 2035년까지 연평균 성장률(CAGR) 7.7%로 성장할 것으로 전망됩니다. 상업용 재배 시설은 생산 효율 극대화, 작물 품질 유지, 그리고 견실한 재무 실적 달성에 중점을 두고 있어 시장 수요를 주도하고 있습니다. 이러한 목표를 뒷받침하기 위해 운영사는 환경 조건을 정밀하게 제어할 수 있는 첨단 환기 기술에 대한 의존도를 높이고 있습니다. 이 부문이 주도적인 위치를 차지하고 있는 주된 요인은 전 세계적으로 대규모로 전개되고 있는 상업용 온실 사업에 있습니다. 이러한 사업에서는 최적의 재배 환경을 유지하기 위해 첨단 인프라가 필요합니다. 소규모 재배 시설에 비해 상업적 사업자는 더 풍부한 자금력을 보유하고 있으며, 생산성, 운영 신뢰성 및 자원 효율성을 향상시키는 첨단 환기 시스템에 대한 투자 의지도 더 강합니다.

북미의 온실 환기 시스템 시장은 2025년에 2억 1,000만 달러 시장 규모를 기록했으며, 2035년까지 연평균 성장률(CAGR) 5.8%로 성장할 것으로 전망됩니다. 이 지역의 성장은 지속적인 기술 혁신, 환경 제어 농업의 보급 확대, 그리고 고품질 농산물에 대한 소비자 수요 증가에 힘입어 이루어지고 있습니다. 지능형 모니터링 기술, 데이터 기반 기후 관리, 그리고 자동화된 환기 솔루션의 통합을 통해 농업 사업자들은 생산성을 최적화하는 동시에 노동력에 대한 의존도를 낮추고, 전반적인 재배 성과를 향상시킬 수 있게 되었습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 환기 방식별, 2022년-2035년

제6장 시장 추산 및 예측 : 컴포넌트별, 2022년-2035년

제7장 시장 추산 및 예측 : 설치 유형별, 2022년-2035년

제8장 시장 추산 및 예측 : 용도별, 2022년-2035년

제9장 시장 추산 및 예측 : 지역별, 2022년-2035년

제10장 기업 개요

LSHThe Global Greenhouse Ventilation Systems Market was valued at USD 1.03 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 2.13 billion by 2035.

Market expansion is driven by the growing focus on maximizing greenhouse productivity, optimizing resource utilization, and improving crop quality through advanced environmental management systems. Ventilation technologies play a critical role in maintaining ideal growing conditions by regulating temperature, humidity, air circulation, and atmospheric balance within greenhouse structures. Increasing emphasis on sustainable agricultural practices, food quality standards, and climate-resilient cultivation methods is further strengthening demand for modern greenhouse infrastructure. Technological advancements have significantly transformed greenhouse operations, enabling greater automation, enhanced monitoring capabilities, and more precise climate management. Government support for agricultural modernization initiatives and sustainability-focused cultivation programs is also contributing to market growth. Although installation costs remain a challenge for smaller growers, increasing investments in large-scale greenhouse projects, protected cultivation systems, and advanced agricultural facilities continue to create significant growth opportunities across the Greenhouse Ventilation Systems Market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.03 Billion |

| Forecast Value | $2.13 Billion |

| CAGR | 7.1% |

The mechanical ventilation segment generated USD 560 million in 2025 and is expected to grow at a CAGR of 7.1% between 2026 and 2035. This segment maintains a leading position due to its ability to deliver consistent performance, accurate environmental control, and dependable operation under varying cultivation conditions. Unlike passive airflow methods, mechanical systems actively regulate internal greenhouse environments, enabling growers to maintain stable temperature, humidity, and atmospheric conditions regardless of external weather fluctuations. Their ability to support controlled environment agriculture operations and integrate seamlessly with advanced greenhouse infrastructure has made them a preferred choice among commercial producers seeking greater productivity and crop consistency. Continued investments in automation and climate control technologies are expected to further strengthen demand for mechanical ventilation solutions throughout the forecast period.

The commercial segment accounted for 56.86% share in 2025 and is projected to grow at a CAGR of 7.7% through 2035. Commercial cultivation facilities dominate market demand due to their focus on maximizing production efficiency, maintaining crop quality, and achieving strong financial performance. To support these objectives, operators increasingly rely on advanced ventilation technologies capable of regulating environmental conditions with high precision. The segment's leadership position is primarily attributed to the extensive scale of commercial greenhouse operations worldwide, which require sophisticated infrastructure to maintain optimal growing environments. Compared with smaller cultivation setups, commercial operators possess greater financial resources and stronger incentives to invest in advanced ventilation systems that improve productivity, operational reliability, and resource efficiency.

North America Greenhouse Ventilation Systems Market generated USD 210 million in 2025 and is anticipated to grow at a CAGR of 5.8% through 2035. Regional growth is supported by ongoing technological innovation, increasing adoption of controlled environment agriculture, and rising consumer demand for high-quality agricultural products. The integration of intelligent monitoring technologies, data-driven climate management, and automated ventilation solutions is enabling agricultural operators to optimize productivity while reducing labor dependency and improving overall cultivation performance.

Major companies operating in the Global Greenhouse Ventilation Systems Market include Ridder Group, Priva B.V., Munters Group AB, Certhon, Harnois Greenhouses, Vostermans Ventilation B.V., J&D Manufacturing, ULMA Agricola S.Coop., Agra Tech Inc., Dalsem B.V., Argus Controls (CEL Group), Van der Valk Horti Systems, Link4 Greenhouse Controls, Pinnacle Climate Tech (Schaefer), Richel Group, Enerdes (Reinders Corporation), BioTherm Solutions, Prospiant (fmr. Nexus + Rough Bros), Alumat Parts (fmr. Alumat Zeeman), Gigola & Riccardi SpA, and GGS Structures Inc. Companies operating in the Greenhouse Ventilation Systems Market are focusing on technological innovation, product customization, and strategic collaborations to strengthen their market position. Manufacturers are investing in advanced climate-control solutions that improve energy efficiency, environmental regulation, and overall greenhouse productivity. The integration of automation technologies, smart sensors, data analytics, and intelligent control platforms has become a key strategy for enhancing system performance and differentiating product offerings. Many companies are expanding partnerships with greenhouse operators, agricultural technology providers, and infrastructure developers to increase market reach and accelerate adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.2.1 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Region

- 2.2.2 Ventilation Type

- 2.2.3 Component

- 2.2.4 Installation Type

- 2.2.5 Application

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supply chain analysis

- 3.2.1 Critical raw material sourcing (motors, aluminum profiles, PVC components)

- 3.2.2 Manufacturing concentration & geographic supply risks

- 3.2.3 Supply chain disruption impact assessment (post-covid, tariff exposure)

- 3.2.4 Near-shoring & supplier diversification trends

- 3.3 Industry impact forces

- 3.3.1 Market drivers

- 3.3.1.1 Rising global food security concerns accelerating controlled environment agriculture (CEA) adoption

- 3.3.1.2 Government subsidies & favorable agricultural policies promoting greenhouse infrastructure investment

- 3.3.1.3 Energy efficiency mandates driving demand for smart & automated ventilation systems

- 3.3.1.4 Expansion of vertical farming & year-round crop production requirements

- 3.3.2 Market restraints

- 3.3.2.1 High initial capital expenditure deterring small & medium-scale greenhouse operators

- 3.3.2.2 Technical complexity of advanced ventilation integration in existing greenhouse structures

- 3.3.3 Market opportunities

- 3.3.3.1 IoT, AI & Sensor Integration Creating Next-Generation Smart Ventilation Systems

- 3.3.3.2 Retrofit Demand in Aging Greenhouse Infrastructure Across Europe & North America

- 3.3.3.3 Untapped Growth Potential in Asia Pacific & Middle East Protected Agriculture Expansion

- 3.3.1 Market drivers

- 3.4 Growth potential analysis

- 3.5 Technology & innovation landscape

- 3.5.1 Smart ventilation & IoT-enabled climate control systems

- 3.5.2 Variable speed drive (VSD) fan technology

- 3.5.3 Energy recovery ventilation (ERV) in greenhouse applications

- 3.5.4 Ai & predictive climate control integration

- 3.5.5 Emerging materials in fan & vent component design

- 3.6 Regulatory framework

- 3.6.1 Agricultural & environmental regulations by region

- 3.6.2 Energy efficiency standards for industrial fans & blowers (EU Ecodesign, US DOE)

- 3.6.3 Building codes & greenhouse construction standards

- 3.6.4 Carbon emission & sustainability compliance requirements

- 3.7 Major market trends and disruptions

- 3.8 Future market trends

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 price variance by ventilation type (natural vs. Mechanical vs. Hybrid)

- 3.9.4 regional price (differentials & import duty impact)

- 3.10 Trade data analysis (driven by primary research)

- 3.10.1 Import/export volume & value trends by HS code (841459 - industrial fans & blowers) (driven by primary research)

- 3.10.2 Key trade corridors & tariff impact (China-EU, Netherlands-global horticulture exports) (driven by primary research)

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-driven disruption of existing greenhouse climate control business models

- 3.11.2 Genai use cases & adoption roadmap by segment (commercial vs. Research greenhouses)

- 3.11.3 Risks, limitations & regulatory considerations for AI in agricultural environments

- 3.12 Investment & funding analysis

- 3.12.1 Private equity & venture capital investment in controlled environment agriculture (CEA)

- 3.12.2 Government grants & agricultural subsidies supporting greenhouse infrastructure

- 3.12.3 M&A activity impact on market consolidation

- 3.13 Porter's analysis

- 3.14 Pestel analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Ventilation Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key Trends

- 5.2 Natural Ventilation Systems

- 5.2.1 Roof Vent Systems

- 5.2.2 Side Wall Vent Systems

- 5.2.3 Ridge Vent Systems

- 5.3 Mechanical Ventilation Systems

- 5.3.1 Exhaust Fan Systems

- 5.3.2 Horizontal Circulation Fan Systems

- 5.3.3 Vertical Circulation Fan Systems

- 5.3.4 Pad-And-Fan Evaporative Cooling Systems

- 5.4 Hybrid Ventilation Systems

- 5.4.1 Passive-Mechanical Combined Systems

- 5.4.2 Automated Hybrid Systems With Smart Controls

Chapter 6 Market Estimates and Forecast, By component, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key Trends

- 6.2 Fans & Blowers

- 6.2.1 Exhaust & Circulation Fans

- 6.2.2 Centrifugal Blowers

- 6.2.3 Variable Speed Drive (VSD) Fans

- 6.3 Louvers & Vents

- 6.3.1 Roof/Ridge Louvers

- 6.3.2 Side Wall Vents

- 6.3.3 Motorized Louvered Panels

- 6.4 Dampers

- 6.4.1 Motorized Dampers

- 6.4.2 Manual Butterfly Dampers

- 6.5 Controllers & Control Systems

- 6.5.1 Thermostatic Controllers

- 6.5.2 Humidity-Based Automated Controllers

- 6.5.3 Iot-Enabled Smart Climate Controllers

- 6.5.4 Integrated Environmental Management Systems (EMS)

- 6.6 Others (Screens, Actuators, Ducting & Ancillary Hardware)

Chapter 7 Market Estimates and Forecast, By Installation Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key Trends

- 7.2 New Installation

- 7.2.1 Greenfield Greenhouse Construction Projects

- 7.2.2 Large-Scale Commercial & Agribusiness Expansions

- 7.3 Retrofit

- 7.3.1 Upgrade Of Legacy Fan & Vent Infrastructure

- 7.3.2 Integration Of Smart Controllers Into Existing Systems

- 7.3.3 Energy Efficiency Retrofit Programs

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key Trends

- 8.2 Commercial Greenhouses

- 8.2.1 Fruit & Vegetable Production Greenhouses

- 8.2.2 Cut Flower & Ornamental Crop Greenhouses

- 8.2.3 Large-Scale Agribusiness & Corporate Farming Complexes

- 8.3 Horticulture Greenhouses

- 8.3.1 Nursery & Propagation Facilities

- 8.3.2 Landscaping & Garden Center Greenhouses

- 8.4 Research & Educational Greenhouses

- 8.4.1 University & Agricultural Research Institutions

- 8.4.2 Government & Public Sector Research Facilities

- 8.5 Residential Greenhouses

- 8.5.1 Hobby & Private Greenhouses

- 8.5.2 Small-Scale Home Farming Setups

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Munters Group AB

- 10.2 Vostermans Ventilation B.V.

- 10.3 Van der Valk Horti Systems

- 10.4 Enerdes (Reinders Corporation)

- 10.5 Pinnacle Climate Tech (Schaefer)

- 10.6 Gigola & Riccardi SpA

- 10.7 Ridder Group

- 10.8 J&D Manufacturing

- 10.9 Dalsem B.V.

- 10.10 Harnois Greenhouses

- 10.11 Agra Tech Inc.

- 10.12 GGS Structures Inc.

- 10.13 Richel Group

- 10.14 Link4 Greenhouse Controls

- 10.15 Alumat Parts (fmr. Alumat Zeeman)

- 10.16 Prospiant (fmr. Nexus + Rough Bros)

- 10.17 Priva B.V.

- 10.18 Argus Controls (CEL Group)

- 10.19 BioTherm Solutions

- 10.20 Certhon

- 10.21 ULMA Agricola S.Coop.