|

시장보고서

상품코드

2083121

적층 제조용 후처리 장비 시장 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Global Post Processing Equipment for Additive Manufacturing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

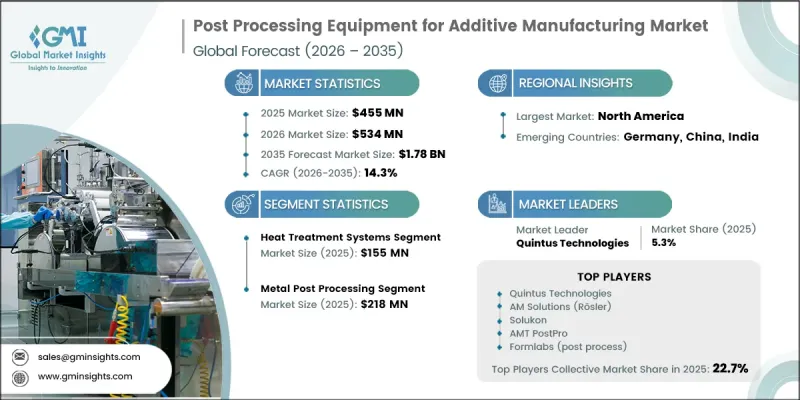

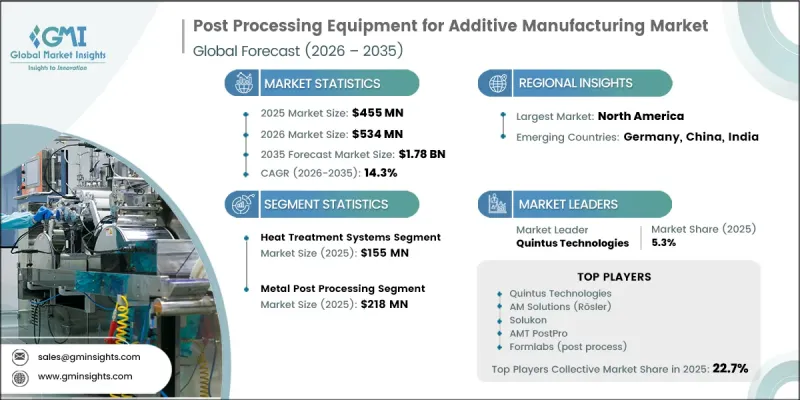

세계의 적층 제조용 후처리 장비 시장은 2025년에 4억 5,500만 달러 규모에 달하고, 2035년까지 CAGR 14.3%로 성장하여 17억 8,000만 달러에 달할 것으로 예측됩니다.

그러나 후처리 장비는 자동화 기술 및 열처리 솔루션 분야에서 강력한 성장세를 보이고 있으며, 주요 적층 제조 하드웨어에서 나타나는 투자 동향과는 확연히 차별화되고 있습니다. 장비 비용의 감소, 자재 조달의 용이성 확대, 그리고 입증된 투자 수익률에 힘입어 인쇄량이 증가함에 따라, 후처리 시스템이 필요한 도입 기반은 계속해서 확대되고 있습니다. 적층 제조가 산업 생산 분야에 더욱 확산됨에 따라, 제조업체들은 더욱 엄격한 품질 보증, 인증 및 규정 준수 요건에 직면하고 있으며, 표준화되고 재현 가능한 후처리 작업의 필요성이 높아지고 있습니다. 이러한 변화로 인해 노동 집약적인 방식에서 장비 중심의 업무 흐름으로의 전환이 촉진되어, 생산되는 부품 1개당 수익이 증가하고 있습니다. 또한, 자동화 솔루션이 생산량이 적어도 경제적으로 실현 가능해짐에 따라, 자동화 도입 확대가 대상 시장을 넓혀가고 있습니다. 또한, 이 시장은 적층 제조 생산 생태계 전반에 걸친 설비 투자를 지속적으로 뒷받침하는 유리한 장기 투자 환경의 혜택도 누리고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 4억 5,500만 달러 |

| 예측액 | 17억 8,000만 달러 |

| CAGR | 14.3% |

열처리 시스템 부문은 2025년에 1억 5,500만 달러의 매출을 기록하며 시장 점유율 34.1%를 차지했습니다. 이러한 시스템에 대한 수요는, 규제가 엄격한 산업 분야에서 널리 사용되는 금속 적층 제조 부품의 구조적 무결성, 성능 및 신뢰성을 향상시키는 데 있어 이 시스템들이 수행하는 매우 중요한 역할에 힘입어 증가하고 있습니다. 생산 워크플로우에서 열처리 기술이 필수적이기 때문에 이 부문에는 계속해서 막대한 설비 투자가 집중되고 있습니다. 산업 분야에서 적층 제조의 채택이 확대됨에 따라, 품질 및 성능 요건을 충족하는 데 있어 열처리 시스템이 중요한 역할을 수행하고 있으므로, 해당 시스템은 시장에서 주도적인 위치를 유지할 것으로 예상됩니다.

금속 부문은 2025년에 2억 1,800만 달러의 매출을 기록하며 시장 점유율의 47.9%를 차지했습니다. 이러한 강력한 성장은 주로 생산 환경에서 금속 적층 제조의 활용 확대에 힘입은 것입니다. 여러 최종 용도 분야에서 첨단 금속 소재로 제조된 고성능 부품에 대한 수요가 증가함에 따라, 부품의 품질, 일관성 및 성능을 향상시키기 위해 설계된 전문적인 후처리 기술에 대한 투자가 지속적으로 확대되고 있습니다.

북미의 적층 제조용 후처리 장비 시장은 2025년에 1억 5,900만 달러의 매출을 기록하며 시장 점유율의 35%를 차지했습니다. 미국은 적층 제조 생산 활동이 집중되어 있고, 첨단 제조 기술에 대한 지속적인 투자가 이루어지고 있기 때문에 여전히 지역 수요의 최대 견인차 역할을 하고 있습니다. 확립된 산업 기반의 존재, 주요 산업 분야에서의 적층 제조 도입 확대, 그리고 국내 제조 혁신에 대한 지속적인 지원이 지역 전체의 시장 성장에 크게 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 장비 유형별, 2022-2035년

제6장 시장 추정 및 예측 : 재료 적합성별, 2022-2035년

제7장 시장 추정 및 예측 : 최종 이용 산업별, 2022-2035년

제8장 시장 추정 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

KSMThe Global Post Processing Equipment for Additive Manufacturing Market was valued at USD 455 million in 2025 and is estimated to grow at a CAGR of 14.3% to reach USD USD 1.78 Billion by 2035.

However, post-processing equipment experienced strong momentum in automation technologies and heat treatment solutions, setting it apart from investment trends observed in primary additive manufacturing hardware. The expansion of print volumes, supported by declining equipment costs, wider material availability, and proven returns on investment, continues to enlarge the installed base requiring post-processing systems. As additive manufacturing moves further into industrial production, manufacturers face stricter quality assurance, certification, and compliance requirements, increasing the need for standardized and repeatable post-processing operations. This shift is driving the transition from labor-intensive methods to equipment-driven workflows, resulting in greater revenue generation per manufactured component. Additionally, increasing automation adoption is broadening the addressable market, as automated solutions become economically viable at lower production volumes. The market is also benefiting from favorable long-term investment conditions that continue to support capital expenditures across additive manufacturing production ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $455 Million |

| Forecast Value | $1.78 Billion |

| CAGR | 14.3% |

The heat treatment systems segment generated USD 155 million in 2025, accounting for 34.1% share. Demand for these systems is driven by the critical role they play in improving the structural integrity, performance, and reliability of metal additive manufacturing components used across highly regulated industries. The segment continues to attract significant capital investment due to the essential nature of thermal processing technologies within production workflows. As additive manufacturing adoption expands across industrial applications, heat treatment systems are expected to maintain their leading position within the market due to their importance in meeting quality and performance requirements.

The metal segment generated USD 218 million, representing 47.9% share in 2025. This strong expansion is primarily supported by the increasing use of metal additive manufacturing in production environments. Growing demand for high-performance components manufactured from advanced metal materials across multiple end-use sectors continues to drive investments in specialized post-processing technologies designed to enhance component quality, consistency, and performance.

North America Post Processing Equipment for Additive Manufacturing Market generated USD 159 million in 2025, accounting for 35% share. The United States remains the largest contributor to regional demand due to its strong concentration of additive manufacturing production activities and ongoing investments in advanced manufacturing technologies. The presence of a well-established industrial base, increasing adoption of additive manufacturing across critical industries, and continued support for domestic manufacturing innovation are contributing significantly to market growth throughout the region.

Key participants operating in the global post-processing equipment for additive manufacturing market include Quintus Technologies, AM Solutions (Rosler), AMT PostPro, Solukon, ALD Vacuum Technologies, DyeMansion, PostProcess Technologies, Walther Trowal, Elnik Systems, Otec, Hirtenberger, and Formlabs (Post-Process Division). Companies operating within the Global Post Processing Equipment for Additive Manufacturing Market are implementing a range of strategic initiatives to strengthen their competitive position and expand market share. Product innovation remains a major priority, with manufacturers focusing on advanced automation, improved process efficiency, and enhanced quality control capabilities. Businesses are investing heavily in research and development to introduce next-generation solutions that reduce production costs and improve operational productivity. Strategic partnerships and collaborations with additive manufacturing technology providers, material suppliers, and industrial manufacturers are helping companies broaden their market reach and enhance integrated solution offerings. Many industry participants are also pursuing geographic expansion strategies to increase their presence in high-growth regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.2.1 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Region

- 2.2.2 Equipment Type

- 2.2.3 Material Compatibility

- 2.2.4 End-use Industry

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supply chain analysis

- 3.2.1 Key Input Components & Critical Material Dependencies

- 3.2.2 Supply Chain Vulnerabilities & Risk Mapping

- 3.2.3 Near-Shoring & Localization Trends

- 3.3 Industry impact forces

- 3.3.1 Market drivers

- 3.3.1.1 Rising Industrialization of Additive Manufacturing Driving Demand for Scalable Post-Processing Solutions

- 3.3.1.2 Automation Imperative: Manual Labor Bottleneck Accelerating Equipment Adoption

- 3.3.1.3 Expanding Metal AM Applications in Aerospace & Medical Requiring Heat Treatment & HIP Systems

- 3.3.1.4 Sustainability & Environmental Regulations Pushing Adoption of Eco-Friendly Finishing Technologies

- 3.3.2 Market restraints

- 3.3.2.1 High Capital Cost of Automated Post-Processing Equipment Limiting SME Adoption

- 3.3.2.2 Lack of Standardization Across AM Technologies Creating Process Compatibility Barriers

- 3.3.2.3 Hazardous Chemical Handling Requirements (IPA, Reactive Metal Powders) Adding Compliance Burden

- 3.3.3 Market opportunities

- 3.3.3.1 Integration of Robotics & AI for Intelligent, Closed-Loop Post-Processing Automation

- 3.3.3.2 Emergence of Hybrid Platforms Consolidating Multiple Post-Processing Steps in One System

- 3.3.3.3 Asia Pacific Manufacturing Expansion Creating High-Growth Deployment Opportunity

- 3.3.3.4 Composite & Ceramic AM Growth Opening New Equipment Design Requirements

- 3.3.3.5 Expansion

- 3.3.1 Market drivers

- 3.4 Growth potential analysis

- 3.5 Technology & innovation landscape

- 3.5.1 Emerging Post-Processing Technologies (Laser Polishing, Electrochemical Finishing, Robotic Automation)

- 3.5.2 Integration of Digital Twins in Post-Processing Workflows

- 3.5.3 Technology Maturity Matrix Across Equipment Categories

- 3.6 Regulatory framework

- 3.6.1 Safety & Hazardous Substances Regulations (IPA, Reactive Powders)

- 3.6.2 Part Certification Standards for Aerospace & Medical (AS9100, ISO 13485)

- 3.6.3 Environmental Compliance & Waste Disposal Regulations

- 3.7 Major market trends and disruptions

- 3.8 Future market trends

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.10 Trade data analysis (driven by primary research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-Driven Disruption of Existing Post-Processing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Equipment Segment (Predictive Maintenance, Process Optimization, Quality Inspection)

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Investment & funding analysis

- 3.12.1 Venture Capital & Private Equity Activity

- 3.12.2 Strategic Corporate Investments & Spin-Offs

- 3.12.3 Government & Public R&D Funding Trends

- 3.13 Porter’s analysis

- 3.14 Pestel analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key Trends

- 5.2 Support Removal Systems

- 5.2.1 Chemical Dissolution Systems

- 5.2.2 Mechanical & Ultrasonic Support Removal Systems

- 5.2.3 Soluble Support Material Removal Systems

- 5.3 Depowdering & Blasting Equipment

- 5.3.1 Manual & Semi-Automated Depowdering Systems

- 5.3.2 Fully Automated Depowdering Systems (Robotic/SPR-Based)

- 5.3.3 Shot Blasting & Abrasive Blasting Systems

- 5.4 Surface Finishing Equipment

- 5.4.1 Vapor Smoothing Systems

- 5.4.2 Tumbling & Vibratory Finishing Systems

- 5.4.3 Electropolishing & Chemical Finishing Systems

- 5.4.4 Laser Polishing Systems

- 5.4.5 CNC-Based Hybrid Finishing Systems

- 5.5 Coloring & Coating Equipment

- 5.5.1 Industrial Dyeing Systems

- 5.5.2 Spray Coating & Painting Systems

- 5.5.3 Metallization & Functional Coating Systems

- 5.6 Heat Treatment Systems

- 5.6.1 Stress Relief & Annealing Furnaces

- 5.6.2 Hot Isostatic Pressing (HIP) Systems

- 5.6.3 Sintering & Debinding Furnaces

- 5.7 Automated Post-Processing Systems

- 5.7.1 Integrated Multi-Step Automated Platforms

- 5.7.2 Robotic Post-Processing Cells

- 5.7.3 Inline & Conveyor-Based Automated Solutions

Chapter 6 Market Estimates and Forecast, By Material Compatibility, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key Trends

- 6.2 Polymer & Plastic

- 6.2.1 Thermoplastics (FDM/FFF, SLS, MJF)

- 6.2.2 Photopolymers (SLA, DLP, PolyJet)

- 6.3 Metal

- 6.3.1 Steel & Stainless Steel

- 6.3.2 Titanium & Titanium Alloys

- 6.3.3 Aluminum & Aluminum Alloys

- 6.3.4 Nickel Superalloys

- 6.3.5 Cobalt-Chrome

- 6.3.6 Other Metals

- 6.4 Composite & Ceramic

- 6.4.1 Continuous & Short Fiber Composites

- 6.4.2 Carbon Fiber Reinforced Polymers (CFRP)

- 6.4.3 Ceramic & Technical Ceramic Parts

Chapter 7 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key Trends

- 7.2 Aerospace & Defense

- 7.2.1 Commercial Aviation

- 7.2.2 Military & Defense

- 7.2.3 Space & Satellite

- 7.3 Automotive

- 7.3.1 OEM Production & Tooling

- 7.3.2 Motorsport & Performance

- 7.3.3 Electric Vehicles & Emerging Mobility

- 7.4 Healthcare & Medical

- 7.4.1 Dental Applications

- 7.4.2 Orthopedics & Implants

- 7.4.3 Surgical Instruments & Medical Devices

- 7.5 Industrial & General Manufacturing

- 7.5.1 Tooling, Jigs & Fixtures

- 7.5.2 Spare Parts & MRO

- 7.5.3 Energy & Heavy Industry

- 7.6 Consumer Goods & Electronics

- 7.6.1 Wearables & Lifestyle Products

- 7.6.2 Consumer Electronics Enclosures & Components

- 7.7 Others (Education, Architecture, Research)

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 U.K.

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 AMT - Additive Manufacturing Technologies (PostPro)

- 9.2 PostProcess Technologies

- 9.3 AM Solutions - 3D Post Processing Technology (Rosler Group)

- 9.4 Solukon Maschinenbau GmbH

- 9.5 DyeMansion GmbH

- 9.6 GPA Innova

- 9.7 Addiblast

- 9.8 AM-Flow

- 9.9 Rivelin Robotics

- 9.10 3DNextech

- 9.11 Formlabs Inc

- 9.12 Renishaw plc

- 9.13 Additive Assurance

- 9.14 Quintus Technologies

- 9.15 Elnik Systems

- 9.16 Hirtenberger Engineered Surfaces (HES)

- 9.17 Vapormatt Ltd.

- 9.18 ULT AG

- 9.19 Walther Trowal GmbH & Co. KG

- 9.20 ALD Vacuum Technologies GmbH

- 9.21 Otec Prazisionsfinish GmbH