|

시장보고서

상품코드

2083126

커넥티드카 핀테크 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Connected Vehicle Fintech Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

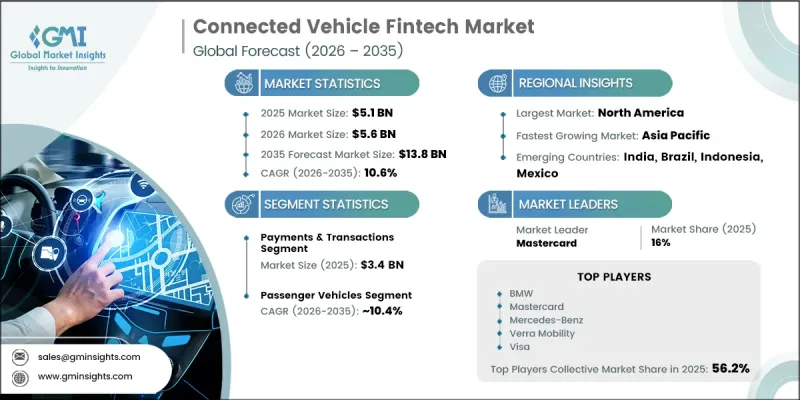

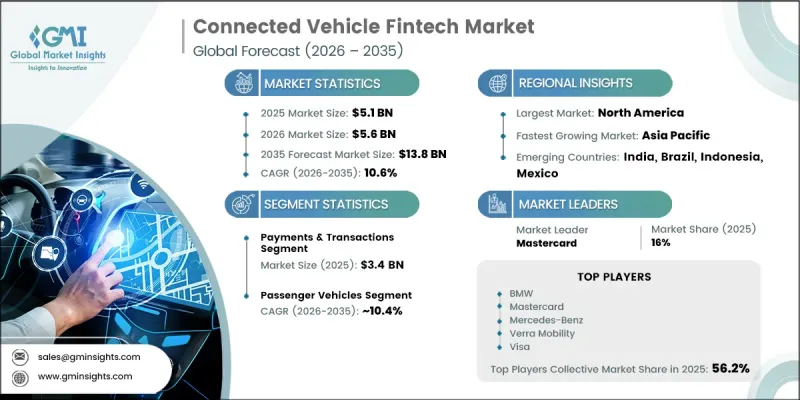

세계의 커넥티드카 핀테크 시장은 2025년에 51억 달러 규모로 평가되었고, CAGR 10.6%로 성장하여 2035년까지 138억 달러에 달할 것으로 추정되고 있습니다.

이러한 성장을 주도하고 있는 요인은 전 세계적으로 커넥티드카 생태계의 도입이 가속화되고, 소프트웨어 중심의 차량 플랫폼이 널리 보급되며, 자동차 분야에서의 디지털 금융 서비스 통합이 진행되고 있다는 점입니다. 차량의 연결성이 높아짐에 따라, 차량은 기존의 단순한 이동 수단이라는 틀을 넘어, 광범위한 금융 거래를 지원할 수 있는 상시 연결형 디지털 플랫폼으로 진화하고 있습니다. 이러한 변화는 결제 사업자, 보험사, 모빌리티 사업자, 차량 관리 업체, 그리고 자동차 제조업체에게 새로운 기회를 창출하고 있습니다. 동시에, 자동차 제조업체들은 차량의 전동화와 첨단 기술에 대한 투자 증가를 상쇄하기 위해 소프트웨어를 활용한 서비스와 구독형 비즈니스 모델을 확대하며, 수익원의 다각화를 적극적으로 추진하고 있습니다. 또한, 소비자 수요도 차량 이용 중에 자연스럽게 발생하는 원활하고 자동화된 구매 경험으로 전환되고 있으며, 이로 인해 커넥티드카용 핀테크 솔루션의 상업적 잠재력이 더욱 강화되고, 전 세계 자동차 및 금융 생태계 전반에 걸친 장기적인 시장 성장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 51억 달러 |

| 예측액 | 138억 달러 |

| CAGR | 10.6% |

결제·거래 부문은 2025년에 34억 달러의 매출을 기록하고, 시장 점유율의 66.6%를 차지하며, 2035년까지 연평균 성장률(CAGR) 10.5%로 성장할 것으로 전망됩니다. 이 부문의 성장은 다양한 자동차 관련 서비스에 내장형 결제 기능이 널리 보급되고, 전 세계적으로 커넥티드카의 보급률이 지속적으로 확대됨에 따라 뒷받침되고 있습니다. 거래 활동 증가와 차량 내 통합형 금융 서비스의 보급 확대에 힘입어, 예측 기간 동안 수익 창출이 더욱 강화될 것으로 전망됩니다.

승용차 부문은 2025년에 38억 달러에 달했습니다. 해당 부문은 2035년까지 연평균 성장률(CAGR) 10.4%를 기록하며 성장할 것으로 전망됩니다. 이러한 주도적인 위상은 13억 대를 넘는 전 세계 승용차 보유 대수의 방대함은 물론, 신차 모델에 커넥티비티 기술이 확대 적용되고 있는 데 크게 기인하고 있습니다. 승용차에 커넥티드 기술이 통합되는 추세가 이어지면서, 핀테크 용도에 유리한 환경이 지속적으로 조성되고 있으며, 이는 해당 부문의 성장에 크게 기여하고 있습니다.

미국의 커넥티드카 핀테크 시장은 2025년에 18억 달러 규모에 달했습니다. 신차 판매 대수에서 내장형 커넥티비티 기술의 높은 보급률은 차량 기반 금융 서비스 도입을 위한 견고한 기반을 마련하고 있습니다. 커넥티드 인프라의 광범위한 구축에 더해, 자동차 관련 디지털 거래에 대한 소비자의 수용도가 높아짐에 따라 미국은 계속해서 커넥티드카 및 핀테크 업계의 주요 성장 거점으로서의 입지를 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 솔루션별, 2022년-2035년

제6장 시장 추산 및 예측 : 차량별, 2022년-2035년

제7장 시장 추산 및 예측 : 용도별, 2022년-2035년

제8장 시장 추산 및 예측 : 최종 용도별, 2022년-2035년

제9장 시장 추산 및 예측 : 지역별, 2022년-2035년

제10장 기업 개요

LSH 26.07.14The Global Connected Vehicle Fintech Market was valued at USD 5.1 billion in 2025 and is estimated to grow at a CAGR of 10.6% to reach USD 13.8 billion by 2035.

Growth is fueled by the accelerating deployment of connected vehicle ecosystems worldwide, increasing adoption of software-centric vehicle platforms, and the growing integration of digital financial services within automotive environments. As vehicles become increasingly connected, they are evolving beyond traditional transportation assets into continuously connected digital platforms capable of supporting a wide range of financial interactions. This transformation is creating new opportunities for payment providers, insurers, mobility operators, fleet managers, and automotive manufacturers. At the same time, automakers are actively diversifying revenue streams by expanding software-enabled services and subscription-based business models to offset mounting investments in vehicle electrification and advanced technologies. Consumer demand is also shifting toward seamless and automated purchasing experiences that occur naturally during vehicle usage, further strengthening the commercial potential of connected vehicle fintech solutions and supporting long-term market growth across global automotive and financial ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.1 Billion |

| Forecast Value | $13.8 Billion |

| CAGR | 10.6% |

The payments and transactions segment generated USD 3.4 billion in 2025, representing 66.6% share, and is anticipated to grow at a CAGR of 10.5% through 2035. Segment growth is being supported by the wider implementation of embedded payment capabilities across various vehicle-related services and the continuous expansion of connected vehicle penetration worldwide. Increasing transaction activity and broader adoption of integrated financial services within vehicles are expected to further strengthen revenue generation throughout the forecast period.

The passenger vehicles segment reached USD 3.8 billion in 2025. The segment is forecast to grow at a CAGR of 10.4% through 2035. Its leadership position is largely attributed to the immense size of the global passenger vehicle fleet, which exceeds 1.3 billion units, along with rising connectivity adoption across new vehicle models. Growing integration of connected technologies in passenger cars continues to create favorable conditions for fintech applications, contributing significantly to segment growth.

U.S. Connected Vehicle Fintech Market generated USD 1.8 billion in 2025. High penetration of embedded connectivity technologies in newly sold vehicles has established a strong foundation for the adoption of vehicle-based financial services. The widespread availability of connected infrastructure, combined with growing consumer acceptance of digital automotive transactions, continues to position the United States as a key growth center for the connected-vehicle fintech industry.

Key participants operating in the global connected vehicle fintech market include Mastercard, Visa, Verra Mobility, Mercedes-Benz, BMW Group, Hyundai Motor, and PayPal. Companies operating in the connected vehicle fintech market are focusing on strategic initiatives designed to strengthen their competitive positions and expand market reach. Many industry participants are investing heavily in connected mobility platforms, digital payment integration, and software-driven vehicle ecosystems to enhance customer engagement and generate recurring revenue streams. Strategic partnerships between automotive manufacturers, payment technology providers, financial institutions, and mobility service companies are becoming increasingly common as organizations seek to accelerate innovation and improve service delivery. Companies are also prioritizing investments in cybersecurity, data protection, and secure transaction capabilities to build consumer trust and support regulatory compliance.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Solution

- 2.2.3 Vehicle

- 2.2.4 Application

- 2.2.5 End-Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid Growth in Connected Vehicle Adoption & IoT Penetration

- 3.2.1.2 Consumer Demand for Seamless, Frictionless Payment Experiences

- 3.2.1.3 OEM Focus on Recurring Revenue & Subscription Models

- 3.2.1.4 Acceleration of EV Adoption Requiring Integrated Charging Payments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Payment Fragmentation & Lack of Interoperability Standards

- 3.2.2.2 Legacy Payment Infrastructure & Slow Settlement Times Capabilities

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into Emerging Markets with Growing Vehicle Connectivity

- 3.2.3.2 Fleet Management Fintech Solutions for Commercial Vehicles

- 3.2.3.3 Partnership Opportunities Between OEMs & Financial Institutions

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technological trends

- 3.3.1.1 In-vehicle payment terminals (embedded card readers)

- 3.3.1.2 Mobile wallet integration

- 3.3.1.3 Telematics-based transaction systems

- 3.3.2 Emerging technologies

- 3.3.2.1 Blockchain-based payment and settlement

- 3.3.2.2 EV charging wallet integration

- 3.3.2.3 Vehicle-to-everything (V2X) payment ecosystems

- 3.3.1 Current technological trends

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 US - NHTSA (National Highway Traffic Safety Administration)

- 3.5.1.2 US - CFPB (Consumer Financial Protection Bureau)

- 3.5.2 Europe

- 3.5.2.1 EU - EDPB / National DPAs (European Data Protection Board & Data Protection Authorities)

- 3.5.2.2 EU - ESMA (European Securities and Markets Authority)

- 3.5.3 Asia Pacific

- 3.5.3.1 China - MIIT (Ministry of Industry and Information Technology)

- 3.5.3.2 India - RBI (Reserve Bank of India)

- 3.5.4 LATAM

- 3.5.4.1 Brazil - BCB (Banco Central do Brasil)

- 3.5.4.2 Mexico - CNBV (Comision Nacional Bancaria y de Valores)

- 3.5.5 MEA

- 3.5.5.1 UAE - DFSA / ADGM (Dubai Financial Services Authority)

- 3.5.5.2 Saudi Arabia - SAMA (Saudi Central Bank)

- 3.5.1 North America

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Cybersecurity & Functional Safety Analysis

- 3.10.1 Payment Security Standards (PCI DSS, Tokenization)

- 3.10.2 Vehicle Authentication & Authorization Protocols

- 3.10.3 Data Encryption & Privacy Protection

- 3.10.4 Cybersecurity Threat Landscape

- 3.11 Integration with Autonomous & ADAS Ecosystem

- 3.11.1 Autonomous Fleet Payment Orchestration

- 3.11.2 Ride-Hailing & Robotaxi Financial Integration

- 3.11.3 Vehicle-to-Everything (V2X) Payment Infrastructure

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.12.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Solution, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Payments & Transactions

- 5.3 Insurance & Risk Services

- 5.4 Lending & Leasing

- 5.5 Mobility & Fintech Platforms

Chapter 6 Market Estimates and Forecast, By Vehicle, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Passenger Vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial Vehicles

- 6.3.1 Light Commercial Vehicles

- 6.3.2 Medium Commercial Vehicles

- 6.3.3 Heavy Commercial Vehicles

- 6.4 Two Wheelers

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 In-Vehicle Payment

- 7.2.1 Charging & Refueling

- 7.2.2 Tolls & Parking

- 7.2.3 In-car commerce

- 7.2.4 Other

- 7.3 Mobility-as-a-Service (MaaS)

- 7.4 Vehicle Ownership & Financing

- 7.5 Vehicle Operations & Lifecycle Services

Chapter 8 Market Estimates and Forecast, By End-Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Commercial Fleets

- 8.4 Mobility Service Providers

- 8.5 Retail Consumers

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Poland

- 9.3.7 Norway

- 9.3.8 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Indonesia

- 9.4.6 South Korea

- 9.4.7 Thailand

- 9.4.8 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Mastercard

- 10.1.2 Visa

- 10.1.3 Mercedes-Benz

- 10.1.4 PayPal

- 10.1.5 Hyundai Motor

- 10.1.6 BMW

- 10.1.7 Parkopedia

- 10.1.8 Cerence AI

- 10.1.9 Aisin

- 10.2 Regional players

- 10.2.1 Verra Mobility

- 10.2.2 ryd

- 10.2.3 CarPay-Diem

- 10.2.4 PACE Telematics

- 10.2.5 Cubic3

- 10.3 Emerging players

- 10.3.1 Sheeva.AI

- 10.3.2 Car IQ

- 10.3.3 Aiden Automotive

- 10.3.4 Pairpoint