|

시장보고서

상품코드

2083129

식품 접촉 재료 및 포장 안전성 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Food Contact Materials and Packaging Safety Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

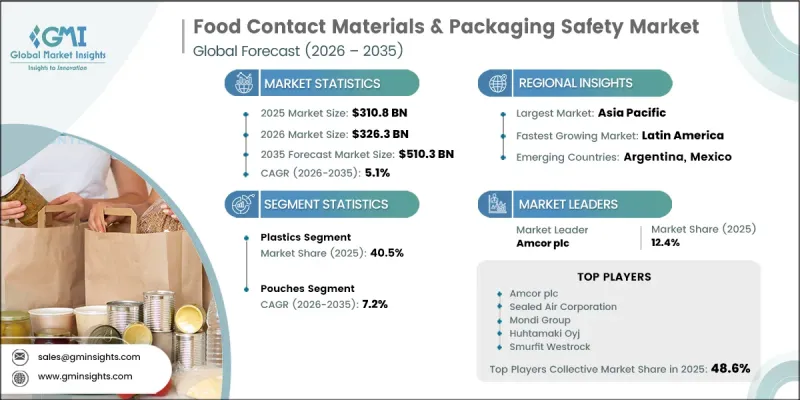

세계의 식품 접촉 재료 및 포장 안전성 시장은 2025년에 3,108억 달러로 평가되었고, CAGR 5.1%로 성장하여 2035년까지 5,103억 달러에 달할 것으로 추정되고 있습니다.

시장의 성장은 신흥 경제국에서의 체계적인 소매 네트워크 및 외식 산업의 지속적인 확장에 힘입고 있으며, 이로 인해 안전하고 규정을 준수하는 식품 접촉 재료에 대한 지속적인 수요가 발생하고 있습니다. 포장 공급망이 점점 더 세계화됨에 따라, 제조업체들은 여러 지역에 걸쳐 더욱 엄격해진 규제 감독과 끊임없이 변화하는 안전 요건에 직면하고 있습니다. 동시에, 지속 가능한 포장재와 바이오 대체재의 채택이 확대됨에 따라 시험, 검증 및 규정 준수 활동에 대한 수요가 더욱 증가하고 있습니다. 새로운 포장 기재, 재생 소재, 혁신적인 고분자 배합에 대해서는 끊임없이 변화하는 규제를 준수하기 위해 종합적인 안전성 평가가 필요합니다. 전 세계 규제 당국은 식품 접촉 재료에 대한 요건을 지속적으로 강화하고 있어, 제조업체의 규정 준수 절차가 점점 더 복잡해지고 있습니다. 끊임없이 변화하는 규제 상황에 더해, 식품 안전성, 지속가능성 및 포장 투명성에 대한 소비자의 인식이 높아지면서 식품 접촉 재료 및 포장 안전성 시장 전반에 대한 투자를 지속적으로 견인하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 3,108억 달러 |

| 예측 금액 | 5,103억 달러 |

| CAGR | 5.1% |

2025년에는 플라스틱 부문이 시장 점유율의 40.5%를 차지했습니다. 정부와 규제 당국이 재료 구성, 화학 물질의 이동, 환경에 미치는 영향에 관한 더 엄격한 요건을 도입함에 따라, 해당 부문은 계속해서 규제 당국의 강화된 감시를 받고 있습니다. 동시에, 외식 산업 및 소매 포장 분야에서 종이 기반, 섬유 기반, 재생 소재, 바이오 유래 솔루션을 포함한 대체 포장 재료로의 단계적 전환이 진행되고 있습니다. 이러한 변화에도 불구하고, 식품용 플라스틱 소재는 그 다용도성, 내구성 및 폭넓은 용도로 인해 여전히 시장을 독점하고 있습니다. 플라스틱 소재는 연포장, 경질 용기, 캡 및 다양한 식품 포장 용도로 계속해서 널리 사용되고 있으며, 시장 전체에서 그 중요성은 앞으로도 변함없이 유지될 것입니다.

파우치 부문은 2035년까지 연평균 성장률(CAGR) 7.2%로 성장할 것으로 전망됩니다. 이러한 성장은 여러 식품 및 음료 부문에서 가볍고 편리하며 비용 효율이 뛰어난 포장 솔루션에 대한 수요가 증가하고 있는 데서 비롯되었습니다. 플렉서블 파우치는 운송 효율, 보관 최적화, 소비자 편의성 측면에서 큰 이점을 제공하며, 제조업체와 최종 사용자 모두에게 점점 더 매력적인 선택지가 되고 있습니다. 파우치 용도에서 다층 포장 구조의 활용이 확대됨에 따라, 식품 접촉 재료의 안전성 평가의 중요성도 높아지고 있습니다. 이는 여러 재료 층으로 구성된 구조의 경우, 적용되는 식품 안전 기준을 준수하고 다양한 사용 조건 하에서 성능 요건을 충족시키기 위해서는 종합적인 평가가 필요하기 때문입니다.

북미의 식품 접촉 재료 및 포장 안전성 시장은 25%의 점유율을 차지하고 있으며, 2035년까지 연평균 성장률(CAGR) 4.1%를 나타낼 것으로 예측됩니다. 이 지역은 식품 안전성, 원재료의 투명성 및 소비자 보호 확보에 중점을 둔, 매우 잘 정비된 규제 환경의 혜택을 누리고 있습니다. 식품 접촉 재료를 규제하는 요건은 지속적으로 발전하고 있으며, 화학 물질 공개, 제품 안전성 검증 및 공급망에 대한 책임성이 더욱 중요시되고 있습니다. 연방 및 지역 차원에서 규정 준수 의무가 강화됨에 따라, 제조업체, 포장재 공급업체 및 브랜드 소유주들은 첨단 시험, 인증 및 모니터링 프로세스에 대한 투자를 확대되고 있습니다. 규제 기준이 강화됨에 따라, 북미 시장에서 사업을 전개하는 기업들은 시장 접근성을 유지하고 변화하는 업계의 기대에 부응하기 위해 규정 준수 전략을 최우선으로 삼고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 재료 유형별, 2022년-2035년

제6장 시장 추산 및 예측 : 포장 형태별, 2022년-2035년

제7장 시장 추산 및 예측 : 용도별, 2022년-2035년

제8장 시장 추산 및 예측 : 최종 용도 채널별, 2022년-2035년

제9장 시장 추산 및 예측 : 지역별, 2022년-2035년

제10장 기업 개요

LSH 26.07.14The Global Food Contact Materials & Packaging Safety Market was valued at USD 310.8 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 510.3 billion by 2035.

Market growth is supported by the continued expansion of organized retail networks and foodservice industries across emerging economies, which is generating sustained demand for safe and compliant food contact materials. As packaging supply chains become increasingly globalized, manufacturers are facing stricter regulatory oversight and evolving safety requirements across multiple regions. At the same time, the growing adoption of sustainable packaging materials and bio-based alternatives is creating additional demand for testing, validation, and compliance activities. New packaging substrates, recycled content materials, and innovative polymer formulations require comprehensive safety assessments to ensure compliance with evolving regulations. Regulatory authorities worldwide continue to strengthen requirements surrounding food contact materials, increasing the complexity of compliance processes for manufacturers. This evolving regulatory landscape, combined with growing consumer awareness regarding food safety, sustainability, and packaging transparency, continues to drive investment across the food contact materials & packaging safety market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $310.8 Billion |

| Forecast Value | $510.3 Billion |

| CAGR | 5.1% |

The plastics segment accounted for 40.5% share in 2025. The segment continues to face increasing regulatory scrutiny as governments and regulatory agencies introduce stricter requirements related to material composition, chemical migration, and environmental impact. Simultaneously, the market is witnessing a gradual transition toward alternative packaging materials, including paper-based, fiber-based, recycled, and bio-derived solutions across foodservice and retail packaging applications. Despite these shifts, food-grade plastic materials continue to maintain a dominant presence due to their versatility, durability, and broad application range. Plastic materials remain widely utilized in flexible packaging formats, rigid containers, closures, and various food packaging applications, ensuring their continued importance within the overall market.

The pouches segment is expected to grow at a CAGR of 7.2% through 2035. Growth is being driven by increasing demand for lightweight, convenient, and cost-efficient packaging solutions across multiple food and beverage categories. Flexible pouch formats offer significant advantages in transportation efficiency, storage optimization, and consumer convenience, making them increasingly attractive to both manufacturers and end users. The growing use of multilayer packaging structures within pouch applications has also increased the importance of food contact material safety evaluations, as multiple material layers require comprehensive assessment to ensure compliance with applicable food safety standards and performance requirements under various usage conditions.

North America Food Contact Materials & Packaging Safety Market accounted for 25% share and is expected to grow at a CAGR of 4.1% through 2035. The region benefits from a highly developed regulatory environment focused on ensuring food safety, material transparency, and consumer protection. Regulatory requirements governing food contact materials continue to evolve, placing greater emphasis on chemical disclosure, product safety validation, and supply chain accountability. Increasing compliance obligations across both federal and regional levels are encouraging manufacturers, packaging suppliers, and brand owners to invest in advanced testing, certification, and monitoring processes. As regulatory standards become more stringent, organizations operating within the North American market are prioritizing compliance strategies to maintain market access and meet changing industry expectations.

Key companies operating in the Global Food Contact Materials & Packaging Safety Market include Amcor plc, SGS S.A., Sonoco Products Company, Mondi Group, Eurofins Scientific SE, Smurfit Westrock, Intertek Group plc, Coveris Holdings S.A., DS Smith plc, Packaging Corporation of America, Huhtamaki Oyj, Graphic Packaging International, LLC, Pactiv Evergreen Inc., Sealed Air Corporation, International Paper Company, and ProAmpac LLC. Companies competing in the food contact materials & packaging safety market are focusing on several strategic initiatives to strengthen their market position and expand their global footprint. Product innovation remains a primary area of investment, with organizations developing advanced packaging materials that meet evolving safety, sustainability, and regulatory requirements. Businesses are increasing spending on research and development to enhance material performance while ensuring compliance with changing food contact regulations. Strategic partnerships with food manufacturers, packaging converters, testing laboratories, and regulatory specialists are helping companies improve service offerings and strengthen customer relationships. Many market participants are also pursuing acquisitions and expansion initiatives to broaden geographic reach and increase technical capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 Packaging form

- 2.2.4 Application

- 2.2.5 End-use channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By material type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plastics

- 5.2.1 Flexible plastics

- 5.2.2 Rigid plastics

- 5.2.3 Bio-based plastics

- 5.3 Paper & board

- 5.3.1 Corrugated board

- 5.3.2 Folding boxboard

- 5.3.3 Kraft paper

- 5.3.4 Coated paper & board

- 5.4 Metal

- 5.5 Glass

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Packaging Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Bottles

- 6.2.1 Glass bottles

- 6.2.2 Plastic bottles (PET, HDPE)

- 6.3 Cans

- 6.3.1 Aluminum cans

- 6.3.2 Steel cans

- 6.4 Cartons

- 6.5 Pouches

- 6.6 Films & wraps

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food

- 7.2.1 Fresh food

- 7.2.2 Frozen food

- 7.2.3 Processed food

- 7.3 Beverage

- 7.3.1 Alcoholic beverages

- 7.3.2 Non-alcoholic beverages

Chapter 8 Market Estimates and Forecast, By End Use Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Retail

- 8.3 Foodservice

- 8.4 Industrial

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Amcor plc

- 10.2 Coveris Holdings S.A.

- 10.3 DS Smith plc

- 10.4 Eurofins Scientific SE

- 10.5 Graphic Packaging International, LLC

- 10.6 Huhtamaki Oyj

- 10.7 International Paper Company

- 10.8 Intertek Group plc

- 10.9 Mondi Group

- 10.10 Packaging Corporation of America

- 10.11 Pactiv Evergreen Inc

- 10.12 ProAmpac LLC

- 10.13 Sealed Air Corporation

- 10.14 SGS S.A.

- 10.15 Smurfit Westrock

- 10.16 Sonoco Products Company