|

시장보고서

상품코드

2083249

계란 분리기 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Egg Separator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

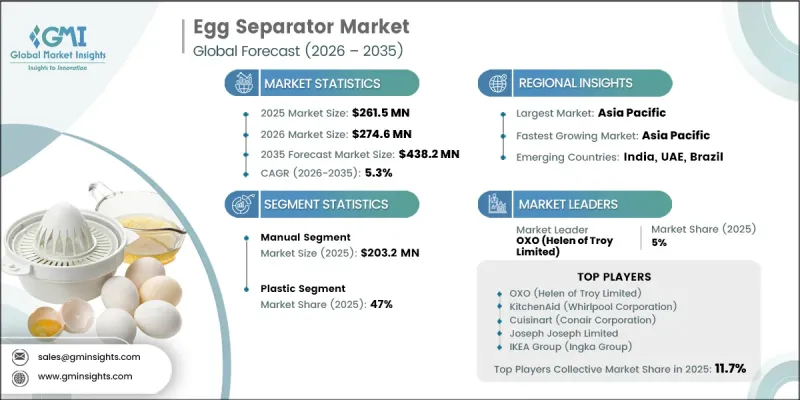

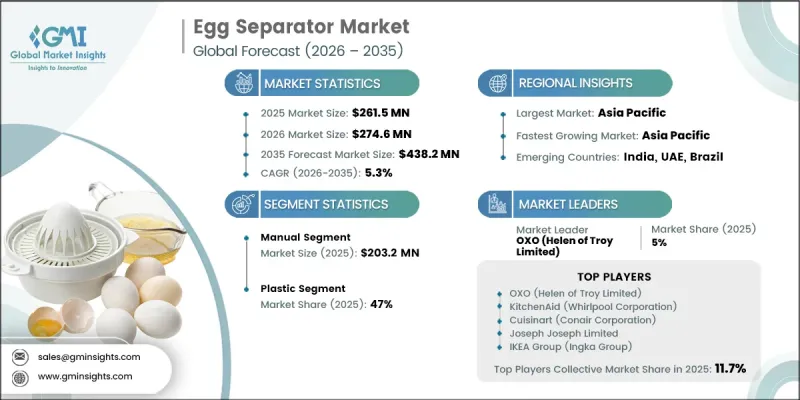

세계의 계란 분리기 시장은 2025년에 2억 6,150만 달러로 평가되었고, CAGR 5.3%로 성장하여 2035년까지 4억 3,820만 달러에 달할 것으로 추정되고 있습니다.

달걀 분리기(에그 세퍼레이터)는 노른자와 흰자를 효율적으로 분리하도록 설계된 전용 조리 도구로, 제빵, 제과, 요리 및 식품 가공 공정에서 필수적인 도구로 활용되고 있습니다. 이 시장은 전 세계 계란 소비량 증가, 최신 주방 가전제품의 보급 확대, 가정용 조리 기구의 고급화, 그리고 온라인 소매 생태계의 급속한 확대와 같은 요인들이 복합적으로 작용하여 성장하고 있습니다. 또한, 전 세계 달걀 분리기 업계에서는 제품 혁신, 소재 선호도, 사용 패턴, 유통망 등 구조적인 변화가 진행되고 있습니다. 여전히 기본적인 주방용품으로 분류되고 있지만, 편의성, 내구성, 디자인의 효율성에 대한 소비자의 기대 변화로 인해 시장은 재편되고 있습니다. 이러한 성장은 도시화의 진전, 중산층의 확대, 그리고 가정 내 조리 습관의 변화에 힘입어 강력하게 뒷받침되고 있습니다. 아시아태평양은 높은 계란 생산량과 소비 수준, 급속한 도시화, 그리고 동아시아 가정의 주방용품에 대한 활발한 수요에 힘입어 시장 규모와 성장 모멘텀 양면에서 선두를 달리고 있습니다. 동시에, 디지털 소매 채널이 구매 행동을 변화시키고 있으며, 온라인 플랫폼이 기존 소매점을 대체하는 추세가 더욱 뚜렷해지고 있습니다. 각 브랜드가 자사 판매 채널을 강화하는 가운데, 소비자에게 직접 판매하는 방식의 디지털 스토어프론트는 제3자 마켓플레이스보다 더 빠르게 성장하고 있습니다. 반면, 선진국 시장에서는 쇼핑몰 방문객 수의 감소와 소비자의 구매 선호도 변화로 인해 오프라인 소매 채널이 압박을 받고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 2억 6,150만 달러 |

| 예측 금액 | 4억 3,820만 달러 |

| CAGR | 5.3% |

수동식 달걀 분리기 부문은 2025년에 2억 320만 달러 규모에 달했습니다. 이 부문은 저렴한 비용과 사용 편의성, 그리고 일반 가정 및 소규모 외식 업계에서의 보급이 확대되고 있는 점에 힘입어 계속해서 시장을 주도하고 있습니다. 수동식 분리기는 전기가 필요 없고, 유지보수도 최소한으로 충분하며, 일상적인 요리나 제과에 필요한 실용적인 기능을 제공하기 때문에 여전히 인기를 끌고 있습니다.

2025년에는 플라스틱 부문이 47%의 점유율을 차지했습니다. 플라스틱은 저렴한 가격과 대량 생산의 효율성 덕분에, 달걀 분리기 제조에 여전히 가장 널리 사용되는 소재입니다. 그러나 스테인리스 스틸이나 실리콘 등 내구성이 더 뛰어난 대체 소재에 대한 수요가 증가하는 데다, 여러 지역에서 플라스틱 사용을 대상으로 한 규제가 강화되고 있어 이 부문은 점점 더 많은 과제에 직면해 있습니다. 환경에 대한 인식이 높아지면서 소비자의 선호에도 영향을 미치고 있으며, 지속가능성이 뛰어나고 제품 수명이 길며 재사용이 가능하고 내구성이 뛰어난 주방용품으로의 전환이 서서히 진행되고 있습니다.

2025년, 미국의 달걀 분리기 시장은 89.9%의 점유율을 차지하며 6,240만 달러의 매출을 기록했습니다. 특히 저가대에서는 보급형 제품의 가정 내 보급률이 포화 상태에 가까워지고 있어, 시장이 성숙의 조짐을 보이고 있습니다. 이에 따라 경쟁의 초점은 프리미엄 제품으로의 업그레이드, 플라스틱에서 더 고급스러운 대체 소재로의 전환, 그리고 온라인 판매 채널에 대한 의존도 증가로 옮겨가고 있습니다. 계란을 사용한 요리 분야의 폭넓은 소비 동향은 주방용 분리 기구에 대한 꾸준하고 장기적인 수요를 지속적으로 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별, 2022년-2035년

제6장 시장 추산 및 예측 : 소재별, 2022년-2035년

제7장 시장 추산 및 예측 : 가격별, 2022년-2035년

제8장 시장 추산 및 예측 : 용량별, 2022년-2035년

제9장 시장 추산 및 예측 : 용도별, 2022년-2035년

제10장 시장 추산 및 예측 : 유통 채널별, 2022년-2035년

제11장 시장 추산 및 예측 : 지역별, 2022년-2035년

제12장 기업 개요

LSH 26.07.14The Global Egg Separator Market was valued at USD 261.5 million in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 438.2 million by 2035.

Egg separators are specialized kitchen tools designed to efficiently divide egg yolks from egg whites, serving as an essential utility in baking, confectionery preparation, culinary applications, and food processing workflows. The market is expanding due to a combination of rising egg consumption globally, increasing adoption of modern kitchen gadgets, premiumization of household cooking tools, and the rapid expansion of online retail ecosystems. The global egg separator industry is also undergoing structural changes across product innovation, material preferences, usage patterns, and distribution networks. Although still categorized as a basic kitchen accessory, the market is being reshaped by shifting consumer expectations toward convenience, durability, and design efficiency. Growth is strongly supported by increasing urbanization, expanding middle-class populations, and evolving home cooking habits. The Asia Pacific region leads both in market size and growth momentum, supported by high egg production and consumption levels, rapid urban expansion, and strong demand for kitchen utility products across East Asian households. At the same time, digital retail channels are transforming purchasing behavior, with online platforms increasingly replacing traditional retail outlets. Direct-to-consumer digital storefronts are expanding faster than third-party marketplaces as brands strengthen their owned sales channels. In contrast, offline retail channels are facing pressure due to reduced mall traffic and shifting consumer buying preferences in developed markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $261.5 Million |

| Forecast Value | $438.2 Million |

| CAGR | 5.3% |

The manual egg separator segment accounted for USD 203.2 million in 2025. This segment continues to lead the market due to its low cost, ease of use, and widespread adoption across households and small-scale food service operations. Manual separators remain popular because they do not require electricity, involve minimal maintenance, and offer practical functionality for everyday cooking and baking needs.

The plastic-based segment held 47% share in 2025. Plastic remains the most widely used material in egg separator manufacturing due to its affordability and mass production efficiency. However, the segment is increasingly challenged by growing demand for more durable alternatives such as stainless steel and silicone, along with tightening regulatory actions targeting plastic usage in multiple regions. Rising environmental awareness is also influencing consumer preferences, encouraging a gradual shift toward reusable, long-lasting kitchen tools that offer better sustainability performance and extended product lifecycles.

U.S. Egg Separator Market held 89.9% share, generating USD 62.4 million in 2025. The market is experiencing signs of maturity as household penetration levels for entry-level products approach saturation, particularly in the lower price range. This has shifted competitive focus toward premium product upgrades and material transitions from plastic to higher-end alternatives, alongside growing reliance on online distribution channels. Broader consumption trends in egg-based food preparation continue to support steady long-term demand for kitchen separation tools.

Major companies operating in the global egg separator market include OXO, KitchenAid, Joseph Joseph, Cuisinart, IKEA Group, Kuhn Rikon, Chef'n Corporation, Norpro, Good Cook (Bradshaw Home), Prepworks by Progressive International, Trudeau Corporation, Tovolo, MSC International (Joie), RSVP International, Fox Run Brands, Hutzler Manufacturing Company, Westmark GmbH, Chef Craft, Pampered Chef, Wilton Brands, and Lakeland. Companies in the egg separator market are focusing on product innovation, premium material upgrades, and ergonomic design improvements to strengthen market positioning. Manufacturers are increasingly shifting from basic plastic designs toward stainless steel and silicone-based products to meet rising sustainability expectations and durability demands. Expansion of e-commerce channels, particularly direct-to-consumer platforms, is enabling brands to improve visibility and customer engagement while reducing dependence on traditional retail networks. Firms are also investing in branding, packaging innovation, and kitchenware ecosystem integration to enhance product differentiation. Strategic collaborations with online retailers and culinary influencers are supporting stronger product promotion.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Business trends

- 2.3 Type trends

- 2.4 Material trends

- 2.5 Price range trends

- 2.6 Capacity trends

- 2.7 End use trends

- 2.8 Distribution channel trends

- 2.9 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem and value chain analysis

- 3.1.1 Raw material & component suppliers

- 3.1.2 Manufacturers & assemblers

- 3.1.3 Distributors & wholesalers

- 3.1.4 Retailers & end-users

- 3.1.5 Profit margin analysis across value chain

- 3.2 Industry impact forces

- 3.2.1 Market Driver

- 3.2.2 Market challenges/pitfalls

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Industry ecosystem analysis

- 3.5 Regulatory framework

- 3.5.1 Food contact material safety standards (FDA, EU Regulation 10/2011)

- 3.5.2 BPA & chemical restriction regulations by region

- 3.5.3 Product safety & labeling compliance (CPSC, CE marking)

- 3.5.4 Sustainability & recyclability regulations impacting kitchenware

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (driven by primary research)

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7 Technology and innovation landscape

- 3.7.1 Emerging filter media technologies

- 3.7.2 Smart & condition-monitoring enabled filters

- 3.7.3 High-pressure & high-efficiency filtration innovations

- 3.8 Porter's Analysis

- 3.9 PESTEL Analysis

- 3.10 Trade data analysis (driven by primary research)

- 3.10.1 Import & export volume & value trends (HS code 8210)

- 3.10.2 Key trade corridors & tariff impact on kitchen tool flows

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of product design & consumer personalization

- 3.11.2 GenAI use cases & adoption roadmap by segment (DTC brands, retailers)

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.12.1 Channel coverage by region & format (modern vs. traditional trade) (driven by primary research)

- 3.12.2 Last-mile infrastructure gaps & emerging channel shifts (Q-commerce, social commerce) (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 APAC

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Electric

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Stainless Steel

- 6.4 Silicone

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Price Range, 2022 - 2035 ($ Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low (< $10)

- 7.3 Medium ($10-$30)

- 7.4 High (> $30)

Chapter 8 Market Estimates and Forecast, By Capacity, 2022 - 2035 ($ Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Single Egg

- 8.3 Multi-Egg

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.3.1 Professional Bakeries

- 9.3.2 Restaurants & Catering

- 9.3.3 Institutional (Hotels, Culinary Schools, Hospital Kitchens)

- 9.3.4 Others (Food Processing Units, Meal-Kit Manufacturers)

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce Platforms

- 10.2.2 Brand/Company Websites (D2C)

- 10.3 Offline

- 10.3.1 Specialty Kitchen Stores

- 10.3.2 Mega Retail / Hypermarkets

- 10.3.3 Others (Department Stores, Home Improvement Stores)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 KitchenAid

- 12.1.2 Cuisinart

- 12.1.3 OXO

- 12.1.4 Joseph Joseph

- 12.1.5 IKEA Group

- 12.1.6 Kuhn Rikon

- 12.1.7 Chef'n Corporation

- 12.2 Regional Players

- 12.2.1 Good Cook (Bradshaw Home)

- 12.2.2 Norpro

- 12.2.3 Prepworks by Progressive International

- 12.2.4 Trudeau Corporation

- 12.2.5 Tovolo

- 12.2.6 MSC International (Joie)

- 12.2.7 RSVP International

- 12.3 Niche & Specialist Players

- 12.3.1 Fox Run Brands

- 12.3.2 Hutzler Manufacturing Company

- 12.3.3 Westmark GmbH

- 12.3.4 Chef Craft

- 12.3.5 Pampered Chef

- 12.3.6 Wilton Brands

- 12.3.7 Lakeland