|

시장보고서

상품코드

2083339

자동차 엣지 컴퓨팅 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Edge Computing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

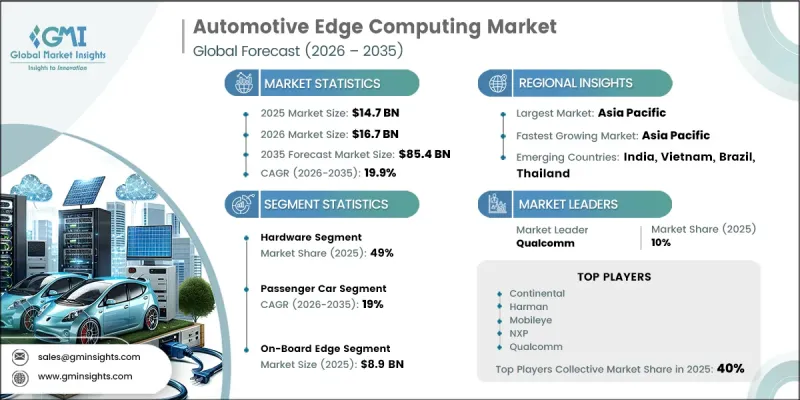

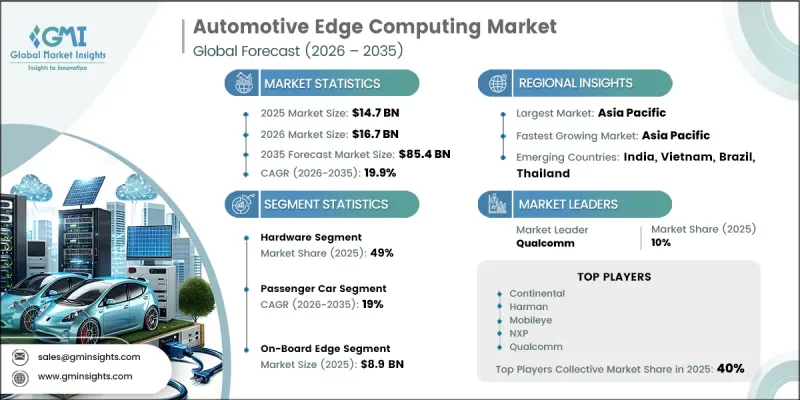

세계의 자동차 엣지 컴퓨팅 시장은 2025년에 147억 달러 규모로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 19.9%로 성장하여 854억 달러에 달할 것으로 추정되고 있습니다.

시장의 성장은 자동차 업계가 하드웨어 중심의 차량 아키텍처에서 소프트웨어 중심이며 지속적인 업그레이드가 가능한 차량 플랫폼으로 전환되고 있는 데 힘입고 있습니다. 현대 차량은 커넥티드 서비스, 지능형 자동화, 인공지능(AI) 용도, 원격 소프트웨어 기능 강화, 그리고 첨단 모빌리티 기능을 뒷받침하는 고성능 컴퓨팅 기능에 대한 의존도를 높이고 있습니다. 소프트웨어 정의 차량의 도입 확대는 차량 아키텍처를 크게 변화시키고 있으며, 기존의 분산형 시스템을 보다 중앙 집중화되고 효율적인 컴퓨팅 프레임워크로 대체하고 있습니다. 차량의 연결성과 데이터 처리량이 점점 더 증가함에 따라, 로컬 데이터 처리 능력에 대한 수요는 계속해서 확대되고 있습니다. 각 자동차 제조업체들은 실시간 분석, 첨단 차량 인텔리전스, 디지털 서비스의 원활한 통합을 지원할 수 있는 차세대 컴퓨팅 인프라에 막대한 투자를 하고 있습니다. 차량용 전자기기의 발전에 더해, 안전성, 편의성, 연결성 향상을 원하는 소비자 수요가 증가함에 따라 자동차 업계 전반에서 엣지 컴퓨팅 기술의 도입이 가속화되고 있습니다. 이러한 추세에 따라, 자동차 엣지 컴퓨팅은 전 세계의 미래 모빌리티 생태계와 지능형 교통 솔루션을 실현하기 위한 중요한 기반으로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 147억 달러 |

| 예측액 | 854억 달러 |

| CAGR | 19.9% |

첨단 운전자 지원 시스템 및 자율 주행 기능의 도입 확대는 자동차 엣지 컴퓨팅 시장에서 여전히 가장 중요한 성장 요인 중 하나입니다. 현대 자동차에서는 정확한 의사결정을 지원하고 운전 안전성을 향상시키기 위해, 차량에 탑재된 여러 시스템에서 생성되는 방대한 양의 데이터를 실시간으로 처리할 수 있는 능력이 요구되고 있습니다. 이러한 요건을 충족하기 위해 자동차 제조업체들은 차량 내부 환경에서 저지연 성능과 고속 데이터 처리를 실현할 수 있는 중앙 집중형 컴퓨팅 플랫폼의 도입을 확대되고 있습니다. 또한, 차량 소프트웨어 시스템이 점점 더 복잡해짐에 따라, 고성능 프로세서 및 인공지능(AI)을 지원하는 컴퓨팅 솔루션에 대한 수요도 증가하고 있습니다. 자동차 제조업체들이 기존의 전자 제어 장치(ECU) 아키텍처에서 전환을 추진하는 가운데, 차세대 모빌리티 기술에 수반되는 방대한 데이터 워크로드를 관리하기 위해서는 고성능 컴퓨팅 플랫폼이 필수적이어지고 있습니다.

하드웨어 부문은 49%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 17.4%를 나타낼 것으로 예측됩니다. 이 부문의 성장은 커넥티드카 및 지능형 자동차에 필요한 자동차 등급 프로세서, 첨단 컴퓨팅 모듈, 메모리 기술, 그리고 통신 하드웨어의 도입 확대에 힘입어 이루어지고 있습니다. 자동차에서 생성되는 운영 데이터와 환경 데이터의 양이 증가함에 따라, 각 자동차 제조업체들은 정보를 실시간으로 처리할 수 있는 고성능 컴퓨팅 시스템에 대한 투자를 확대되고 있습니다. 차량의 지능화, 커넥티비티, 자동화 기술의 지속적인 발전으로 인해, 예측 기간 동안 하드웨어 부품에 대한 견조한 수요가 유지될 것으로 전망됩니다.

승용차 부문은 2025년에 67%의 시장 점유율을 차지했으, 2026년부터 2035년까지 연평균 성장률(CAGR) 19%로 성장할 것으로 전망됩니다. 커넥티드 기술, 디지털 사용자 경험, 지능형 안전 시스템, 소프트웨어 기반 기능 및 첨단 차량 내 서비스의 통합이 진행됨에 따라, 승용차는 도입 분야 중 가장 큰 비중을 차지하고 있습니다. 승용차 시스템이 점점 더 복잡해짐에 따라, 실시간 데이터 처리를 수행하고 여러 디지털 기능을 동시에 지원할 수 있는 강력한 컴퓨팅 플랫폼이 요구되고 있습니다. 이 부문은 차량의 지능화, 커넥티비티, 편의 기능 향상에 대한 소비자의 강력한 수요로 인해 계속해서 혜택을 보고 있으며, 승용차는 시장 전체의 확장을 이끄는 주요 원동력이 되고 있습니다.

2025년, 중국의 자동차 엣지 컴퓨팅 시장 규모는 30억 달러에 달했습니다. 이 나라의 선도적인 위상은 광범위한 전기차 제조 생태계와 스마트 교통 인프라에 대한 급속한 투자에 힘입어 유지되고 있습니다. 커넥티드 모빌리티 기술 및 중앙 집중형 차량 컴퓨팅 시스템의 도입을 가속화하기 위한 지속적인 노력이 계속해서 긍정적인 시장 환경을 조성하고 있습니다. 전국 각지의 자동차 제조업체들은 첨단 컴퓨팅 플랫폼, 지능형 차량 시스템, 차세대 소프트웨어 아키텍처를 향후 차량 개발 프로그램에 점점 더 많이 통합하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 컴포넌트별, 2022년-2035년

제6장 시장 추산 및 예측 : 차량별, 2022년-2035년

제7장 시장 추산 및 예측 : 도입 모드별, 2022년-2035년

제8장 시장 추산 및 예측 : 용도별, 2022년-2035년

제9장 시장 추산 및 예측 : 최종 용도별, 2022년-2035년

제10장 시장 추산 및 예측 : 지역별, 2022년-2035년

제11장 기업 개요

LSH 26.07.14The Global Automotive Edge Computing Market was valued at USD 14.7 billion in 2025 and is estimated to grow at a CAGR of 19.9% to reach USD 85.4 billion by 2035.

Market growth is driven by the automotive industry's transition from hardware-focused vehicle architectures toward software-centric and continuously upgradeable vehicle platforms. Modern vehicles increasingly rely on advanced computing capabilities that support connected services, intelligent automation, artificial intelligence applications, remote software enhancements, and advanced mobility functions. The growing adoption of software-defined vehicles is significantly transforming vehicle architecture, replacing traditional distributed systems with more centralized and efficient computing frameworks. As vehicles become increasingly connected and data-intensive, the need for localized data processing capabilities continues to expand. Automotive manufacturers are investing heavily in next-generation computing infrastructures that can support real-time analytics, advanced vehicle intelligence, and seamless integration of digital services. The evolution of vehicle electronics, combined with increasing consumer demand for enhanced safety, convenience, and connectivity, is accelerating the deployment of edge computing technologies across the automotive sector. These developments are positioning automotive edge computing as a critical enabler of future mobility ecosystems and intelligent transportation solutions worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.7 Billion |

| Forecast Value | $85.4 Billion |

| CAGR | 19.9% |

The growing deployment of advanced driver assistance technologies and autonomous driving capabilities remains one of the most significant growth drivers for the automotive edge computing market. Modern vehicles require the ability to process large volumes of data generated by multiple onboard systems in real time to support accurate decision-making and improve operational safety. To meet these requirements, automotive manufacturers are increasingly adopting centralized computing platforms capable of delivering low-latency performance and high-speed data processing within the vehicle environment. The rising complexity of vehicle software systems is also increasing demand for advanced processors and artificial intelligence-enabled computing solutions. As automakers continue to move away from traditional electronic control unit architectures, high-performance computing platforms are becoming essential for managing the expanding data workloads associated with next-generation mobility technologies.

The hardware segment held a 49% share, and is expected to grow at a CAGR of 17.4% from 2026 to 2035. Segment growth is supported by the increasing deployment of automotive-grade processors, advanced computing modules, memory technologies, and communication hardware required for connected and intelligent vehicles. As automobiles generate larger volumes of operational and environmental data, manufacturers are allocating greater investments toward high-performance computing systems capable of processing information in real time. The continued advancement of vehicle intelligence, connectivity, and automation technologies is expected to sustain strong demand for hardware components throughout the forecast period.

The passenger car segment held a 67% share in 2025 and is projected to grow at a CAGR of 19% between 2026 and 2035. Passenger vehicles represent the largest area of adoption due to the increasing integration of connected technologies, digital user experiences, intelligent safety systems, software-based functionality, and advanced in-vehicle services. The growing complexity of passenger vehicle systems requires powerful computing platforms capable of handling real-time data processing and supporting multiple digital functions simultaneously. The segment continues to benefit from strong consumer demand for enhanced vehicle intelligence, connectivity, and convenience features, making passenger vehicles a key contributor to overall market expansion.

China Automotive Edge Computing Market generated USD 3 billion in 2025. The country's leadership position is supported by its extensive electric vehicle manufacturing ecosystem and rapid investment in intelligent transportation infrastructure. Ongoing efforts to accelerate the deployment of connected mobility technologies and centralized vehicle computing systems continue to create favorable market conditions. Automotive manufacturers across the country are increasingly integrating advanced computing platforms, intelligent vehicle systems, and next-generation software architectures into future vehicle programs.

Major companies operating in the global automotive edge computing market include NVIDIA, Qualcomm, NXP, Continental, Harman, Mobileye, Renesas, Ericsson, and AWS. Companies participating in the automotive edge computing market are pursuing a variety of strategic initiatives to strengthen their market position and expand their technological capabilities. Significant investments in research and development are enabling the creation of advanced computing platforms, artificial intelligence processors, and software solutions designed to support next-generation vehicle architectures. Strategic collaborations with automotive manufacturers, technology providers, and mobility ecosystem participants are helping companies accelerate innovation and broaden market reach. Many organizations are focusing on developing scalable edge computing solutions that support autonomous driving, connected vehicle services, and intelligent transportation systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Component

- 2.2.2 Vehicle

- 2.2.3 Deployment Mode

- 2.2.4 Application

- 2.2.5 End use

- 2.2.6 Region

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Technology & platform providers

- 3.1.1.2 System integrators & implementation partners

- 3.1.1.3 OEM

- 3.1.1.4 Aftermarket

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Adoption of Autonomous & ADAS Technologies

- 3.2.1.2 Growing Shift Toward Software-Defined Vehicles (SDVs)

- 3.2.1.3 Expansion of Connected Vehicle & V2X Ecosystems

- 3.2.1.4 Increasing Demand for Real-Time In-Vehicle Data Processing

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Cost of Advanced Automotive Compute Hardware

- 3.2.2.2 Software Complexity & Integration Challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI Accelerators & High-Performance Automotive Chips

- 3.2.3.2 Emergence of Multi-Access Edge Computing (MEC) in Smart Mobility

- 3.2.3.3 Growth of Centralized Vehicle Compute Architectures

- 3.2.3.4 Increasing Adoption of Edge-Based Cybersecurity Solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 OSHA Process Safety Management (PSM)

- 3.5.1.2 EPA Clean Air Act Regulations

- 3.5.1.3 Canadian Centre for Cyber Security Guidelines

- 3.5.2 Europe

- 3.5.2.1 GDPR (General Data Protection Regulation)

- 3.5.2.2 NIS2 Directive

- 3.5.2.3 WEEE Directive (Waste Electrical and Electronic Equipment Directive)

- 3.5.2.4 EU Industrial Emissions Directive (IED)

- 3.5.3 Asia-Pacific

- 3.5.3.1 China Data Security Law (DSL)

- 3.5.3.2 Japan Industrial Safety and Health Act

- 3.5.3.3 India Digital Personal Data Protection Act (DPDP Act)

- 3.5.3.4 Singapore Cybersecurity Act

- 3.5.4 Latin America

- 3.5.4.1 Brazil General Data Protection Law (LGPD)

- 3.5.4.2 Mexico Federal Law on Protection of Personal Data

- 3.5.5 MEA

- 3.5.5.1 Saudi National Cybersecurity Authority (NCA) ECC Framework

- 3.5.5.2 UAE Information Assurance Standards (IAS) Initiatives

- 3.5.1 North America

- 3.6 Technology and Innovation Landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Use cases

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 Automated design optimization

- 3.11.3 Supply chain AI for demand forecasting

- 3.11.4 GenAI use cases & adoption roadmap by segment

- 3.11.5 Risks, Limitations & Regulatory Considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - key macro & industry variables driving CAGR

- 3.12.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Edge nodes

- 5.2.2 Gateways

- 5.2.3 Edge servers

- 5.2.4 Others

- 5.3 Software

- 5.3.1 Edge device management

- 5.3.2 Analytics & processing software

- 5.3.3 Security software

- 5.3.4 Others

- 5.4 Services

- 5.4.1 Professional

- 5.4.1.1 System integration & deployment

- 5.4.1.2 Consulting & strategy

- 5.4.1.3 Training & support

- 5.4.2 Managed

- 5.4.2.1 Remote monitoring & management

- 5.4.2.2 Maintenance & updates

- 5.4.2.3 Security management

- 5.4.1 Professional

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Medium commercial vehicles

- 6.3.3 Heavy commercial vehicles

- 6.4 Off-highway and Specialty Vehicles

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 On-Board Vehicle Edge

- 7.3 Network/Infrastructure Edge (MEC)

- 7.4 Hybrid Edge

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Autonomous and connected driving

- 8.3 In-vehicle experience & infotainment

- 8.4 Predictive maintenance & diagnostics

- 8.5 Fleet & traffic management

- 8.6 V2X Communication & Smart Mobility

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 OEMs (Original Equipment Manufacturers)

- 9.3 Fleet Operators

- 9.4 Aftermarket & Service Providers

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.3.9 Thailand

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

- 10.5.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 AWS

- 11.1.2 Continental

- 11.1.3 Ericsson

- 11.1.4 Harman International (Samsung)

- 11.1.5 Hewlett Packard Enterprise (HPE)

- 11.1.6 IBM

- 11.1.7 Intel (Mobileye)

- 11.1.8 Microsoft

- 11.1.9 NVIDIA

- 11.1.10 Qualcomm Technologies

- 11.1.11 Robert Bosch

- 11.2 Regional players

- 11.2.1 Aptiv

- 11.2.2 Astemo

- 11.2.3 Vodafone

- 11.2.4 Siemens

- 11.2.5 NXP Semiconductors

- 11.2.6 Renesas Electronics

- 11.3 Emerging players

- 11.3.1 Apex.AI

- 11.3.2 Sibros Technologies

- 11.3.3 Sonatus