|

시장보고서

상품코드

2083392

식품 및 음료 포장기계 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Food and Beverages Packaging Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

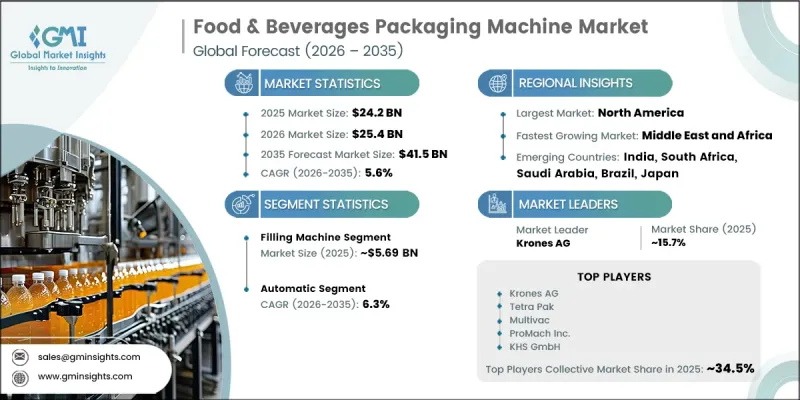

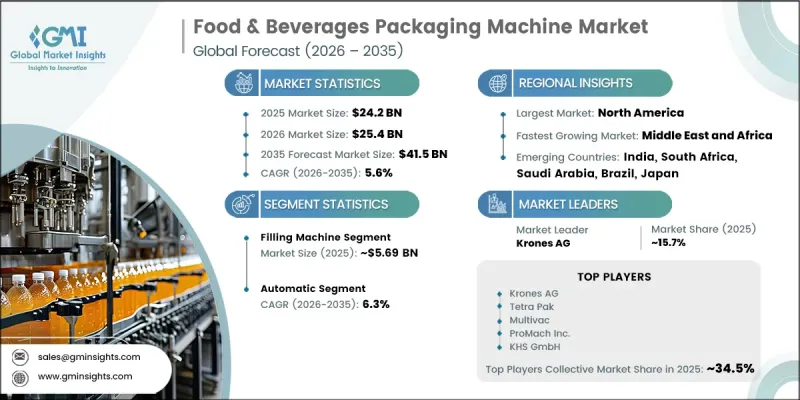

세계의 식품 및 음료 포장기계 시장은 2025년에 242억 달러로 평가되었고, CAGR 5.6%로 성장하여 2035년까지 415억 달러에 달할 것으로 추정되고 있습니다.

식품 및 음료 포장기계 시장은 특히 급속한 도시화가 진행되고 있는 지역에서 포장 및 가공 식품의 세계적 소비 증가에 힘입어 꾸준히 성장하고 있습니다. 가처분 소득 증가, 식생활의 변화, 그리고 현대적인 소매 인프라의 확충이 효율적인 포장 시스템에 대한 수요를 크게 끌어올리고 있습니다. 동시에, 선진국의 엄격한 식품 안전 및 위생 규제로 인해 제조업체들은 제품의 무결성, 추적성, 그리고 엄격한 품질 기준 준수를 보장하는 첨단 자동 포장 솔루션을 도입할 수밖에 없게 되었습니다. 인건비 급등은 자동화 전환을 더욱 가속화하고 있으며, 식품 가공업체들이 고속·다기능 포장 설비에 투자하도록 촉진하고 있습니다. 각 제조업체들은 효율성과 생산 능력을 향상시키기 위해 기존 생산 라인을 첨단 충전, 밀봉, 라벨링 및 최종 공정 시스템으로 업그레이드하는 움직임을 강화하고 있습니다. 주요 시장의 식품 안전 규정 준수 기준 등 규제 체계 역시 위생적이고 완전 자동화된 포장 인프라에 대한 지속적인 설비 투자를 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 242억 달러 |

| 예측액 | 415억 달러 |

| CAGR | 5.6% |

충진기 부문은 2025년에 56억 9,000만 달러 시장 규모를 기록했으며, 2035년까지 연평균 성장률(CAGR) 4.8%로 성장할 것으로 전망됩니다. 이 부문은 액체, 분말, 과립, 페이스트, 점성 제품 등 다양한 제품을 취급하는 데 있어 매우 중요한 역할을 수행하고 있기 때문에 식품 및 음료용 포장기계 시장에서 계속해서 주요 성장 동력으로 작용하고 있습니다. 액체 충전 시스템은 음료 및 유제품 가공 업계의 활발한 수요에 힘입어 생산량이 가장 많습니다. 충진 기술은 고속화, 정밀도 향상, 위생 기준 강화에 대응하기 위해 지속적으로 발전하고 있으며, 대규모 식품 제조 사업에서 없어서는 안 될 요소가 되고 있습니다.

자동 부문은 2025년에 56.1%의 점유율을 차지했으며, 2035년까지 연평균 성장률(CAGR) 6.3%로 성장할 것으로 전망됩니다. 이러한 우위는 수작업 개입을 줄이면서 일관성과 가동 속도를 향상시키는 고효율 생산 시스템에 대한 수요 증가에 힘입고 있습니다. 생산성 향상, 오류 최소화, 그리고 엄격한 위생 기준 유지를 위해 식품 가공 시설에서는 자동화 기술이 널리 도입되고 있습니다. 또한, 특히 다양한 제품 범주에 걸쳐 유연성, 정밀한 취급 및 처리량 향상이 요구되는 포장 분야에서 로봇 및 반자동 솔루션이 주목받고 있습니다.

북미의 식품 및 음료 포장기계 시장은 고도로 발달하고 기술적으로 선진적인 식품 가공 산업의 견인에 힘입어 2025년에는 29.6%의 시장 점유율을 차지했습니다. 이 지역에서는 생산 효율을 높이고 엄격한 식품 안전 및 품질 규정을 준수하기 위해 자동화 및 현대적인 포장 인프라에 대한 막대한 투자가 계속되고 있습니다. 위생, 추적성, 예방적 안전 조치를 중시하는 강력한 규제 체계 덕분에 식품 및 음료 제조 시설 전반에 걸쳐 포장 시스템의 지속적인 업그레이드가 촉진되고 있습니다. 이러한 자동화와 규제 준수에 대한 지속적인 노력 덕분에, 세계 시장에서 북미의 확고한 입지가 계속해서 더욱 공고해지고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기계 유형별, 2022년-2035년

제6장 시장 추산 및 예측 : 용도별, 2022년-2035년

제7장 시장 추산 및 예측 : 자동화 레벨별, 2022년-2035년

제8장 시장 추산 및 예측 : 포장 유형별, 2022년-2035년

제9장 시장 추산 및 예측 : 유통 채널별, 2022년-2035년

제10장 시장 추산 및 예측 : 지역별, 2022년-2035년

제11장 기업 개요

LSHThe Global Food & Beverages Packaging Machine Market was valued at USD 24.2 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 41.5 billion by 2035.

The food & beverages packaging machine market is witnessing steady expansion driven by rising global consumption of packaged and processed food products, particularly in rapidly urbanizing regions. Increasing disposable incomes, changing dietary patterns, and the expansion of modern retail infrastructure are significantly boosting demand for efficient packaging systems. At the same time, stringent food safety and hygiene regulations across developed economies are compelling manufacturers to adopt advanced, automated packaging solutions that ensure product integrity, traceability, and compliance with strict quality standards. Rising labor costs are further accelerating the shift toward automation, encouraging food processors to invest in high-speed, multi-functional packaging equipment. Manufacturers are increasingly upgrading legacy production lines with advanced filling, sealing, labeling, and end-of-line systems to improve efficiency and output capacity. Regulatory frameworks such as food safety compliance standards in major markets are also driving continuous capital investment in hygienic and fully automated packaging infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.2 Billion |

| Forecast Value | $41.5 Billion |

| CAGR | 5.6% |

The filling machine segment generated USD 5.69 billion in 2025 and is expected to grow at a CAGR of 4.8% through 2035. This segment remains a key contributor to the food & beverages packaging machine market due to its critical role in handling a wide range of liquid, powder, granule, paste, and viscous products. Liquid filling systems account for the highest production volumes, driven by strong demand from beverage and dairy processing industries. Filling technologies continue to evolve to support higher speed, improved accuracy, and enhanced hygiene standards, making them essential for large-scale food manufacturing operations.

The automatic segment accounted for 56.1% share in 2025 and is projected to grow at a CAGR of 6.3% during 2035. Its dominance is supported by increasing demand for high-efficiency production systems that reduce manual intervention while improving consistency and operational speed. Automation technologies are widely adopted across food processing facilities to enhance productivity, minimize errors, and maintain strict hygiene standards. In addition, robotic and semi-automated solutions are gaining traction, particularly in packaging applications that require flexibility, precision handling, and improved throughput performance across diverse product categories.

North America Food & Beverages Packaging Machine Market held 29.6% share in 2025, driven by its highly developed and technologically advanced food processing industry. The region continues to invest heavily in automation and modern packaging infrastructure to improve production efficiency and ensure compliance with stringent food safety and quality regulations. Strong regulatory frameworks emphasizing hygiene, traceability, and preventive safety measures are encouraging continuous upgrades in packaging systems across food and beverage manufacturing facilities. This sustained focus on automation and compliance continues to reinforce North America's strong position in the global market.

Major companies operating in the global food & beverages packaging machine market include Syntegon Technology GmbH, Ishida Co., Ltd., Omori Machinery Co., Ltd., Tetra Pak International S.A., Coesia Group, Gerhard Schubert GmbH, Multivac Group, Barry-Wehmiller Companies Inc., ULMA Packaging S. Coop., CAMA Group S.r.l., ProMach Inc., IMA Group S.p.A., KHS GmbH, Nichrome India Ltd., Rovema GmbH, Krones AG, TNA Solutions Pty Ltd., Fuji Machinery Co., Ltd., SACMI Group, Triangle Package Machinery Co., and Optima Packaging Group GmbH. Companies operating in the food & beverages packaging machine market are strengthening their competitive position by investing in advanced automation technologies, smart packaging systems, and high-speed production equipment that improve efficiency and operational accuracy. Many manufacturers are expanding research and development efforts to introduce innovative filling, sealing, and labeling solutions that meet evolving food safety and hygiene requirements. Strategic partnerships with food and beverage producers are helping companies expand market reach and strengthen customer relationships. Businesses are also focusing on modular machine designs, digital monitoring systems, and predictive maintenance capabilities to enhance productivity and reduce downtime.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Region

- 2.2.2 Machine Type

- 2.2.3 Application

- 2.2.4 Automation Level

- 2.2.5 Packaging Type

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for packaged & processed food products driven by urbanization & changing lifestyles

- 3.2.1.2 Stringent food safety & hygiene regulations compelling automation upgrades (FDA FSMA, EU Reg 852/2004)

- 3.2.1.3 Growth of e-commerce food & beverage channels requiring high-speed, flexible packaging lines

- 3.2.1.4 Labor cost pressures & workforce shortages accelerating shift to automated packaging systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital expenditure & long payback periods for advanced automated packaging machinery

- 3.2.2.2 Skilled labor shortage for programming, operation & maintenance of smart packaging systems

- 3.2.3 Opportunities

- 3.2.3.1 Sustainability-driven demand for machinery compatible with recyclable, bio-based & reduced-plastic formats

- 3.2.3.2 Packaging-machine-as-a-service (MAAS) & lease-based procurement models lowering adoption barriers for SMES

- 3.2.3.3 Rapid expansion of food processing industries in Asia Pacific, MEA creating greenfield demand

- 3.2.3.4 Smart & IoT-connected machinery with AI-driven predictive maintenance & OEE optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 U.S. FDA Food Safety Modernization Act (FSMA) Implications

- 3.6.2 EU Regulation 852/2004 & Packaging & Packaging Waste Directive

- 3.6.3 PMMI & Industry Association Standards

- 3.6.4 Extended Producer Responsibility (EPR) Policy Impact

- 3.7 Trade data analysis (HS Code - 8422.30)

- 3.7.1 Import/Export Volume & Value Trends by Machine Type (Driven by Primary Research)

- 3.7.2 Key Trade Corridors & Tariff Impact on Packaging Machinery (Driven by Primary Research)

- 3.8 Impact of AI & generative AI on the market

- 3.8.1 AI-driven Disruption of Existing Packaging Line Business Models

- 3.8.2 GenAI Use Cases & Adoption Roadmap by Segment (Predictive Maintenance, Quality Inspection, Throughput Optimization)

- 3.8.3 Risks, Limitations & Regulatory Considerations of AI in Packaging Machinery

- 3.9 Pricing Analysis

- 3.9.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Consumer Behavior Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machine Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key Trends

- 5.2 Filling Machines

- 5.2.1 Liquid Filling Machines (Gravity, Piston, Volumetric, Flow Meter)

- 5.2.2 Powder & Granule Filling Machines (Auger, Net Weigh, Gross Weigh)

- 5.2.3 Paste & Viscous Product Filling Machines (Piston, Peristaltic, Rotary)

- 5.3 Sealing Machines

- 5.3.1 Heat Sealing Machines (Band Sealers, Impulse Sealers, Continuous Sealers)

- 5.3.2 Induction Sealing Machines

- 5.3.3 Vacuum Sealing Machines

- 5.4 Labeling Machines

- 5.4.1 Pressure-Sensitive Labeling Machines

- 5.4.2 Sleeve Labeling Machines (Heat Shrink, Roll-Fed)

- 5.4.3 Wrap-Around & Hot Glue Labeling Machines

- 5.4.4 Coding & Marking Systems (Inkjet, Laser, Thermal Transfer)

- 5.5 Wrapping Machines

- 5.5.1 Stretch Wrapping Machines

- 5.5.2 Shrink Wrapping Machines (Sleeve, Full-Body)

- 5.5.3 Flow Wrapping Machines (Horizontal & Vertical)

- 5.6 Form-Fill-Seal (FFS) Machines

- 5.6.1 Vertical Form-Fill-Seal (VFFS) Machines

- 5.6.2 Horizontal Form-Fill-Seal (HFFS) Machines

- 5.6.3 Thermoform-Fill-Seal (TFFS) Machines

- 5.7 Pouch Packaging Machines

- 5.7.1 Stand-Up Pouch Packaging Machines

- 5.7.2 Flat & Pillow Pouch Packaging Machines

- 5.7.3 Spouted & Fitment Pouch Packaging Machines

- 5.8 Others

- 5.8.1 Cartoning Machines (Horizontal & Vertical)

- 5.8.2 Case Packing & Tray Packing Machines

- 5.8.3 Palletizing & Depalletizing Machines (Conventional & Robotic)

- 5.8.4 Checkweighers, Vision Inspection & Metal Detection Systems

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key Trends

- 6.2 Beverages

- 6.2.1 Non-Alcoholic Beverages (Bottled Water, Carbonated Soft Drinks, Juices, Energy Drinks)

- 6.2.2 Alcoholic Beverages (Beer, Wine, Spirits)

- 6.2.3 Dairy Beverages (Milk, Flavored Milk, Plant-Based Drinks)

- 6.2.4 Hot Beverages (Ready-to-Drink Coffee & Tea)

- 6.3 Processed Food

- 6.3.1 Ready-to-Eat & Ready-to-Cook Meals

- 6.3.2 Frozen Foods

- 6.3.3 Snacks & Savory Products

- 6.3.4 Condiments, Sauces & Dressings

- 6.4 Bakery Products

- 6.4.1 Bread, Rolls & Buns

- 6.4.2 Pastries, Cakes & Pies

- 6.4.3 Cookies & Crackers

- 6.5 Confectionery

- 6.5.1 Chocolate & Chocolate-Based Products

- 6.5.2 Sugar Confectionery, Gums & Jellies

- 6.6 Meat, Poultry & Seafood

- 6.6.1 Fresh & Chilled Meat & Poultry

- 6.6.2 Frozen Meat, Poultry & Seafood

- 6.6.3 Processed, Cured & Deli Products

- 6.7 Dairy Products

- 6.7.1 Fluid Milk & Cream

- 6.7.2 Cheese & Butter

- 6.7.3 Yogurt & Fermented Dairy Products

- 6.8 Fruits & Vegetables

- 6.8.1 Fresh & Pre-Cut Produce (MAP Packaging)

- 6.8.2 Frozen Fruits & Vegetables

- 6.8.3 Dried & Dehydrated Produce

- 6.9 Others (Health Foods, Nutritional Supplements, Infant Formula, Pet Food)

Chapter 7 Market Estimates & Forecast, By Automation Level, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key Trends

- 7.2 Automatic Packaging Machines

- 7.2.1 Fully Automatic Continuous Motion Systems

- 7.2.2 Fully Automatic Intermittent Motion Systems

- 7.2.3 Robotic & Collaborative Automation Systems

- 7.3 Semi-Automatic Packaging Machines

- 7.3.1 Operator-Assisted Filling & Sealing Systems

- 7.3.2 Semi-Automatic Labeling & Coding Systems

- 7.3.3 Semi-Automatic Case Packing & Bundling Systems

- 7.4 Manual Packaging Machines

- 7.4.1 Hand-Operated Filling & Sealing Equipment

- 7.4.2 Entry-Level Manual Wrapping & Labeling Solutions

Chapter 8 Market Estimates & Forecast, By Packaging Type, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key Trends

- 8.2 Flexible Packaging

- 8.2.1 Pouches & Bags

- 8.2.2 Films, Wraps & Laminates

- 8.2.3 Sachets & Single-Serve Formats

- 8.3 Rigid Packaging

- 8.3.1 Bottles & Jars (PET, Glass, HDPE)

- 8.3.2 Cans & Metal Containers (Aluminum, Tin)

- 8.3.3 Cartons & Paperboard Boxes

- 8.4 Semi-Rigid Packaging

- 8.4.1 Thermoformed Trays & Clamshells

- 8.4.2 Blister Packs & Skin Packs

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key Trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key Trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Tetra Pak International S.A.

- 11.2 Krones AG

- 11.3 Syntegon Technology GmbH

- 11.4 Multivac Group

- 11.5 IMA Group S.p.A.

- 11.6 Coesia Group

- 11.7 KHS GmbH

- 11.8 ULMA Packaging S. Coop.

- 11.9 Barry-Wehmiller Companies Inc.

- 11.10 ProMach Inc.

- 11.11 Ishida Co., Ltd.

- 11.12 TNA Solutions Pty Ltd.

- 11.13 Rovema GmbH

- 11.14 Gerhard Schubert GmbH

- 11.15 CAMA Group S.r.l.

- 11.16 Fuji Machinery Co., Ltd.

- 11.17 SACMI Group

- 11.18 Optima Packaging Group GmbH

- 11.19 Triangle Package Machinery Co.

- 11.20 Nichrome India Ltd.

- 11.21 Paxiom Group Inc.

- 11.22 Omori Machinery