|

시장보고서

상품코드

1998699

관상동맥 스텐트 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Coronary Stents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

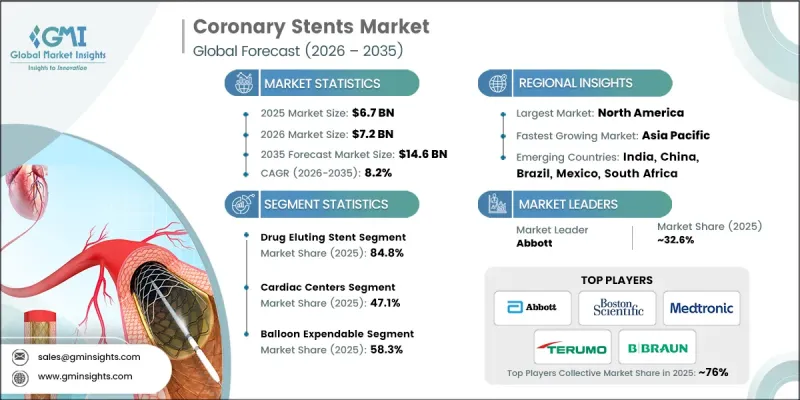

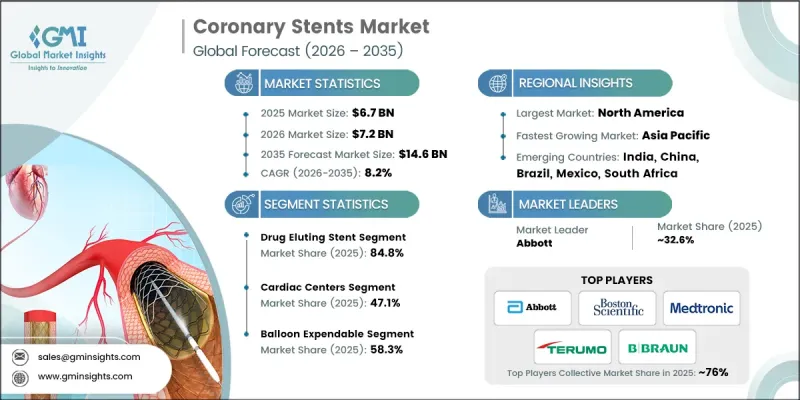

세계의 관상동맥 스텐트 시장은 2025년에 67억 달러로 평가되었고, CAGR 8.2%로 성장하여 2035년까지 146억 달러에 달할 것으로 예측됩니다.

시장 성장은 심혈관 질환의 유병률 증가, 고령화, 스텐트 기술의 발전, 최소침습 수술의 보급 확대에 의해 주도되고 있습니다. 관상동맥 스텐트는 좁아지거나 막힌 관상동맥에 삽입하여 혈관의 개통성을 유지하고 혈류를 개선하며 심근경색을 예방하는 역할을 하는 관상동맥 스텐트입니다. 전 세계 주요 사망원인인 관상동맥질환의 발생률 증가가 수요를 견인하고 있습니다. 약물용출형 스텐트, 생체흡수성 스캐폴드, 폴리머 프리 스텐트 등의 기술 혁신은 재협착과 혈전증을 최소화하여 장기적인 치료 성적을 향상시키고 있습니다. 환자들의 인식이 높아지고, 임상의들의 신뢰도가 높아지며, 혈액 재건술이 확대되면서 더욱 확산되고 있습니다. 약물 용출형 스텐트, 생분해성 스텐트로의 전환, 환자 중심적 접근 등의 트렌드가 전 세계 산업 성장을 주도하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 67억 달러 |

| 예측액 | 146억 달러 |

| CAGR | 8.2% |

약물 용출형 스텐트 부문은 재협착을 최소화하고, 환자의 장기적인 예후를 개선하며, 최소 침습적 치료를 지원하는 능력으로 인해 2025년 84.8%의 점유율을 차지했습니다. 약물 용출형 스텐트는 과도한 조직 증식을 방지하기 위해 약물을 방출하기 때문에 베어메탈 스텐트에 비해 장기적으로 우수한 결과를 가져와 임상에서 널리 사용되고 있습니다.

코발트-크롬 합금 부문은 2035년까지 75억 달러에 달했습니다. 코발트-크롬 합금 스텐트는 높은 인장 강도와 내구성을 가지고 있으며, 동맥압 하에서도 혈관 확장을 유지하면서 더 얇은 스트럿 디자인을 가능하게 합니다. 이 얇은 스트럿은 동맥 손상을 줄이고, 혈류를 개선하고, 치유를 촉진하는 동시에 재협착과 혈전증의 위험을 최소화함으로써 이 부문의 성장을 주도하고 있습니다.

2025년 기준 북미 관상동맥 스텐트 시장은 39.6%의 점유율을 차지했습니다. 미국에서는 좌식생활, 고지방 식습관, 스트레스 등으로 인해 심혈관 질환의 부담이 심화되고 있으며, 이는 관상동맥 스텐트 삽입술에 대한 수요를 증가시키고 있습니다. 이 지역의 첨단 의료 인프라, 전문 심장센터, 숙련된 의료 전문가들의 존재로 인해 스텐트 삽입술이 널리 이용되고 있습니다. 병원과 중재적 심장병 센터의 혁신적인 스텐트 기술 도입은 이 지역의 성장을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별, 2022-2035

제6장 시장 추산 및 예측 : 유형별, 2022-2035

제7장 시장 추산 및 예측 : 재료별, 2022-2035

제8장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.04.23The Global Coronary Stents Market was valued at USD 6.7 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 14.6 billion by 2035.

Market growth is driven by the rising prevalence of cardiovascular diseases, an aging population, advancements in stent technologies, and the increasing adoption of minimally invasive procedures. Coronary stents are tubular devices inserted into narrowed or blocked coronary arteries to maintain vessel patency, enhance blood flow, and prevent heart attacks. The growing incidence of coronary artery disease, a leading cause of mortality worldwide, is fueling demand. Technological innovations such as drug-eluting stents, bioresorbable scaffolds, and polymer-free stents improve long-term outcomes by minimizing restenosis and thrombosis. Rising patient awareness, clinician confidence, and the expansion of revascularization procedures further support adoption. Trends such as the shift toward drug-eluting and biodegradable stents, as well as patient-centric approaches, are shaping industry growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.7 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 8.2% |

The drug-eluting stent segment held a share of 84.8% in 2025 owing to its ability to minimize restenosis, enhance long-term patient outcomes, and support minimally invasive interventions. Drug-eluting stents release medication to prevent excessive tissue growth, providing superior long-term results compared to bare-metal stents, which reinforces their widespread clinical adoption.

The cobalt-chromium alloy segment is expected to reach USD 7.5 billion by 2035. Cobalt-chromium stents offer high tensile strength and durability, maintaining vessel expansion under arterial pressure while allowing thinner strut designs. These thinner struts reduce arterial injury, improve blood flow, and accelerate healing, while minimizing the risk of restenosis and thrombosis, driving segment growth.

North America Coronary Stents Market held a 39.6% share in 2025. The U.S. faces a significant burden of cardiovascular diseases, driven by sedentary lifestyles, high-fat diets, and stress, which increases the demand for coronary stent procedures. The region's advanced healthcare infrastructure, specialized cardiac centers, and skilled medical professionals ensure widespread availability of stenting procedures. The adoption of innovative stent technologies across hospitals and interventional cardiology centers further fuels regional growth.

Prominent players in the Global Coronary Stents Market include Abbott, Medtronic, Boston Scientific, Biotronik, MicroPort Scientific, Stryker, Terumo, B. Braun, Biosensors International Group, Cook Medical, GENOSS, Elixir Medical, Andramed, Meril Life Science, and Sahajanand Laser Technology Limited. Companies in the Global Coronary Stents Market are strengthening their positions through continuous research and development to enhance stent safety, performance, and drug delivery capabilities. Firms are expanding their global footprint by entering emerging markets and forging partnerships with hospitals and healthcare providers. They focus on patient-centric and minimally invasive solutions, including bioresorbable and polymer-free stents, while integrating digital monitoring and smart stent technologies. Strategic marketing campaigns, clinician training programs, and collaborations with leading cardiac centers help companies improve adoption, build brand trust, and maintain a competitive edge in the global coronary stents industry.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Type trends

- 2.2.4 Material trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of coronary artery disease

- 3.2.1.2 Increasing demand for minimally invasive procedures

- 3.2.1.3 Technological advancement in developing economies

- 3.2.1.4 Increasing awareness and focus on preventive cardiac care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Product failure and recall

- 3.2.2.2 Stringent regulatory approvals

- 3.2.2.3 Dearth of skilled healthcare professional in developing economies

- 3.2.3 Market opportunities

- 3.2.3.1 Development of bioresorbable and next-generation stents

- 3.2.3.2 Integration of digital health & imaging technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario (Driven by primary research)

- 3.7 Future market trends

- 3.8 Pricing analysis, 2025 (Driven by primary research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Customer insights (Driven by primary research)

- 3.12 Start-up scenarios

- 3.13 Impact of AI and generative AI on the market

- 3.14 Investment landscape

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Drug eluting stent

- 5.3 Bioresorbable vascular scaffold (BVS)

- 5.4 Bare metal stent

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Balloon expendable stent

- 6.3 Self-expendable stent

Chapter 7 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Cobalt-chromium alloy

- 7.3 Stainless steel

- 7.4 Other materials

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Cardiac centers

- 8.3 Hospitals

- 8.4 Ambulatory surgical centers

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott

- 10.2 Andramed

- 10.3 B. Braun

- 10.4 Biosensors International Group

- 10.5 Biotronik

- 10.6 Boston Scientific

- 10.7 Cook Medical

- 10.8 Elixir Medical

- 10.9 GENOSS

- 10.10 Medtronic

- 10.11 Meril Life Science

- 10.12 MicroPort Scientific

- 10.13 Sahajanand Laser Technology Limited

- 10.14 Stryker

- 10.15 Terumo