|

시장보고서

상품코드

1824266

연료전지 시장 : 예측(2025-2030년)Fuel Cells Market - Forecasts from 2025 to 2030 |

||||||

연료전지 시장은 2025년 65억 5,600만 달러에서 2030년에는 181억 2,900만 달러에 이르고, CAGR 22.56%를 보일 것으로 예측됩니다.

연료전지 시장은 청정에너지 수요 증가와 정부의 지원정책에 힘입어 급성장하고 있습니다. 수소나 다른 연료를 전기로 변환하는 전기화학 장치인 연료전지는 자동차, 유틸리티, 국방 등의 분야에서 인기를 끌고 있습니다. 지속 가능한 에너지 솔루션 제공에 있어 전기화학 장치의 역할은 전 세계 탈탄소화 목표에 부합하며, 예측 기간 동안 시장이 크게 확대될 것으로 보입니다.

시장 성장 촉진요인

연료전지 시장의 주요 촉진요인은 기후 변화와 환경오염에 대한 우려가 커지면서 청정 에너지원에 대한 수요가 증가하고 있다는 점입니다. 연료전지는 수소 및 기타 연료로부터 깨끗한 전기를 생산하여 기존 에너지원을 대체할 수 있는 저탄소 대체 에너지를 제공합니다. 연료전지는 기후 목표 달성에 있어 매우 중요한 역할을 하고 있습니다. 예를 들어, 중국과 같은 국가에서는 연구 투자 및 인센티브를 통해 연료전지 도입을 촉진하는 정책을 시행하고 있습니다. 압축천연가스(CNG) 버스를 연료전지 버스로 대체하는 한국의 노력은 이러한 추세를 상징적으로 보여줍니다. 또한, 기존 연료의 고갈로 인해 대체 에너지원의 필요성이 부각되면서 발전 분야에서 연료전지의 존재감이 더욱 부각되고 있습니다.

시장 동향

연료전지 시장은 전 세계적인 탈탄소화 및 에너지 전환의 추진과 함께 발전하고 있습니다. 수소경제는 연료전지를 Off-grid 및 도시 환경에서의 분산형 발전에 필수적인 무공해 기술을 뒷받침하는 중요한 원동력입니다. 연료전지는 국지적 발전을 가능하게 함으로써 에너지 안보를 강화하고 화석연료에 대한 의존도를 낮출 수 있습니다. 전력망 현대화 노력에 통합하여 재생에너지원을 보완하고 안정적이고 지속 가능한 에너지 공급을 실현할 수 있습니다. 연료전지 기술, 특히 연료전지 스택과 BoP(Balance of Plant) 부품의 혁신이 성능 향상을 촉진하고 있습니다. 철-질소-탄소와 같은 백금족 금속(PGM)이 없는 촉매와 같은 전극 재료의 발전은 값비싼 백금에 대한 의존도를 낮추고 전체 비용을 낮춥니다. 강화된 양성자 교환막 기술은 연료 효율과 출력 밀도를 향상시켜 연료전지를 자동차 및 고정형 용도로 실용화합니다. 내구성은 계속 초점을 맞추고 있으며, 동적 작동 조건에서 연료전지의 수명을 연장하기 위한 노력이 계속되고 있습니다. 이러한 추세는 세계 지속가능성 목표에 부합하는 것으로, 운송수단 및 고정식 전력 시스템에서 연료전지의 적용이 확대되고 있습니다.

시장 성장 억제요인

구체적으로 언급되지는 않았지만, 제조 비용의 상승, 수소 공급 인프라의 제약, 다른 재생 가능 기술과의 경쟁 등의 문제가 시장 성장의 걸림돌이 될 수 있습니다. 지속적인 혁신과 정책적 지원을 통해 이러한 장벽을 극복하는 것이 지속 가능한 확장을 위해 필수적입니다.

경쟁 구도

연료전지 시장은 경쟁이 치열하며 Ballard Power Systems, FuelCell Energy, Hydrogenics 등 주요 기업들이 혁신을 주도하고 있습니다. 이들 기업은 기술 개발, 제휴, 인수 등의 전략을 통해 시장에서의 입지를 강화하고 있습니다. 예를 들어, 2025년 4월 도요타, Shudao, Sichuan Shudao 3사는 중국 남서부 시장에 수소연료전지 시스템을 생산하고 판매하는 합작회사를 설립했는데, 이는 업계가 지역 확대와 협력에 초점을 맞추고 있음을 반영합니다. 경쟁 구도는 시장 점유율 확보를 위한 전략적 거래와 함께 효율성 향상과 비용 절감을 위한 R&D 투자에 의해 형성되고 있습니다.

연료전지 시장은 전 세계적인 청정에너지로의 전환과 정부의 지원정책에 힘입어 강력한 성장세를 보이고 있습니다. PGM이 없는 촉매, 멤브레인 기술, 시스템 내구성의 혁신은 비용 효율성과 성능을 향상시키고, 운송 및 고정식 전력에 대한 응용을 확대합니다. 수소 경제와 전력망 현대화 노력은 지속가능한 에너지 시스템에서 연료전지의 역할을 더욱 증대시킬 것입니다. 업계 이해관계자들은 이 역동적인 시장의 과제를 극복하고 기회를 활용하기 위해 비용 절감과 인프라 구축의 진전을 우선순위에 두어야 합니다. 확장성과 친환경 솔루션에 초점을 맞춘 연료전지는 세계 에너지 전환의 핵심으로 자리매김하고 있습니다.

본 보고서의 주요 장점

- 통찰력 있는 분석 : 고객 부문, 정부 정책 및 사회경제적 요인, 소비자 선호도, 산업별, 기타 하위 부문에 초점을 맞춘 주요 지역 및 신흥 지역을 포괄하는 상세한 시장 분석을 얻을 수 있습니다.

- 경쟁 구도: 세계 주요 기업들이 채택하고 있는 전략적 전략을 이해하고, 적절한 전략을 통한 시장 침투 가능성을 파악할 수 있습니다.

- 시장 동향과 촉진요인 : 역동적인 요인과 매우 중요한 시장 동향, 그리고 그것들이 향후 시장 개척을 어떻게 형성할 것인가를 살펴봅니다.

- 실행 가능한 제안: 통찰력을 전략적 의사결정에 활용하고, 역동적인 환경 속에서 새로운 비즈니스 스트림과 수익을 발굴합니다.

- 다양한 사용자에 대응: 스타트업, 연구기관, 컨설턴트, 중소기업, 대기업에 유익하고 비용 효율적임.

어떤 용도로 사용되는가?

산업 및 시장 인사이트, 사업 기회 평가, 제품 수요 예측, 시장 진출 전략, 지리적 확장, 설비 투자 결정, 규제 프레임워크 및 영향, 신제품 개발, 경쟁의 영향

조사 범위

- 2022-2024년 과거 데이터 & 2025-2030년 예측 데이터

- 성장 기회, 과제, 공급망 전망, 규제 프레임워크 및 동향 분석

- 경쟁사 포지셔닝, 전략 및 시장 점유율 분석

- 매출 성장 및 예측 국가를 포함한 부문 및 지역별 분석

- 기업 프로파일링(특히 재무 및 주요 개발)

목차

제1장 주요 요약

제2장 시장 현황

- 시장 개요

- 시장의 정의

- 조사 범위

- 시장 세분화

제3장 비즈니스 상황

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 시장 기회

- Porter의 Five Forces 분석

- 업계 밸류체인 분석

- 정책 및 규제

- 전략적 제안

제4장 기술 전망

제5장 연료전지 시장 : 유형별

- 서론

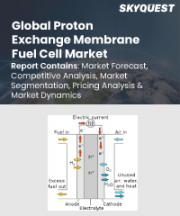

- 고분자 전해질막 연료전지(PEMFC)

- 고체 산화물 연료전지(SOFC)

- 용융 탄산염 연료전지(MCFC)

- 인산 연료전지(PAFC)

- 직접 메탄올 연료전지(DMFC)

- 알칼리성 연료전지(AFC)

- 기타

제6장 연료전지 시장 : 용도별

- 서론

- 고정식 발전

- 운송

- 휴대용 전원

- 자재관리 장비(MHE)

- 보조 동력 장치(APU)

- 기타

제7장 연료전지 시장 : 최종사용자 업계별

- 서론

- 자동차 및 운송

- 유틸리티 및 발전

- 산업

- 상업시설 및 주택

- 헬스케어

- 군 및 방위

- 통신

- 물류 및 창고

- 항공우주

- 기타

제8장 지역별 연료전지 시장

- 서론

- 북미

- 유형별

- 용도별

- 최종사용자 업계별

- 국가별

- 미국

- 캐나다

- 멕시코

- 남미

- 유형별

- 용도별

- 최종사용자 업계별

- 국가별

- 브라질

- 아르헨티나

- 기타

- 유럽

- 유형별

- 용도별

- 최종사용자 업계별

- 국가별

- 영국

- 독일

- 프랑스

- 스페인

- 기타

- 중동 및 아프리카

- 유형별

- 용도별

- 최종사용자 업계별

- 국가별

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타

- 아시아태평양

- 유형별

- 용도별

- 최종사용자 업계별

- 국가별

- 중국

- 일본

- 인도

- 한국

- 대만

- 기타

제9장 경쟁 환경과 분석

- 주요 기업과 전략 분석

- 시장 점유율 분석

- 합병, 인수, 합의 및 협업

- 경쟁 대시보드

제10장 기업 개요

- Ballard Power Systems

- Plug Power Inc.

- FuelCell Energy, Inc.

- Bloom Energy Corporation

- Cummins Inc.

- Ceres Power Holdings plc

- Doosan Fuel Cell Co., Ltd.

- SFC Energy AG

- Panasonic Corporation

- Toyota Motor Corporation

제11장 부록

- 통화

- 전제조건

- 기준연도와 예측연도 타임라인

- 이해관계자의 주요 이점

- 조사 방법

- 약어

도표

표 리스트

LSH 25.10.13The Fuel Cells Market is expected to grow from USD 6.556 billion in 2025 to USD 18.129 billion in 2030, at a CAGR of 22.56%.

The fuel cells market is experiencing rapid growth, driven by increasing demand for clean energy and supportive government policies. Fuel cells, electrochemical devices that convert hydrogen or other fuels into electricity, are gaining traction in applications such as automobiles, utilities, and defense. Their role in delivering sustainable energy solutions aligns with global decarbonization goals, positioning the market for significant expansion during the forecast period.

Market Drivers

The primary driver of the fuel cells market is the rising demand for clean energy sources, spurred by heightened concerns over climate change and environmental pollution. Fuel cells generate electricity cleanly from hydrogen or other fuels, offering a low-carbon alternative to conventional energy sources. Governments worldwide are implementing measures to reduce carbon emissions, with fuel cells playing a pivotal role in achieving climate objectives. For instance, policies in countries like China promote fuel cell adoption through research investments and incentives. South Korea's initiative to replace compressed natural gas (CNG) buses with fuel cell-powered buses exemplifies this trend. Additionally, the depletion of conventional fuels underscores the need for alternative energy sources, further boosting fuel cell prominence in power generation.

Market Trends

The fuel cells market is advancing alongside the global push for decarbonization and energy transition. The hydrogen economy is a key enabler, supporting zero-emission technologies that position fuel cells as critical for distributed power generation in both off-grid and urban settings. Fuel cells enhance energy security by enabling localized power production, reducing dependence on fossil fuels. Their integration into grid modernization efforts complements renewable energy sources, providing stable and sustainable energy supplies. Innovations in fuel cell technology, particularly in Fuel Cell Stack and Balance of Plant (BoP) components, are driving performance improvements. Advances in electrode materials, such as platinum-group-metal (PGM)-free catalysts like iron-nitrogen-carbon, reduce reliance on costly platinum, lowering overall costs. Enhanced proton exchange membrane technology improves fuel efficiency and power density, making fuel cells viable for automotive and stationary applications. Durability remains a focus, with ongoing efforts to extend fuel cell lifespan under dynamic operating conditions. These trends align with global sustainability goals, expanding fuel cell applications in transportation and stationary power systems.

Market Restraints

While not explicitly detailed, challenges such as high production costs, infrastructure limitations for hydrogen supply, and competition from other renewable technologies could hinder market growth. Addressing these barriers through continued innovation and policy support will be critical for sustained expansion.

Competitive Landscape

The fuel cells market is highly competitive, with key players like Ballard Power Systems, FuelCell Energy, Inc., and Hydrogenics driving innovation. These companies employ strategies such as technology development, partnerships, and acquisitions to strengthen their market position. For example, in April 2025, Toyota, Shudao, and Sichuan Shudao formed a joint venture to produce and sell hydrogen fuel cell systems for China's southwestern market, reflecting the industry's focus on regional expansion and collaboration. The competitive landscape is shaped by R&D investments aimed at improving efficiency and reducing costs, alongside strategic deals to capture market share.

The fuel cells market is poised for robust growth, propelled by the global shift toward clean energy and supportive government policies. Innovations in PGM-free catalysts, membrane technology, and system durability enhance cost-effectiveness and performance, broadening applications in transportation and stationary power. The hydrogen economy and grid modernization efforts further amplify fuel cells' role in sustainable energy systems. Industry stakeholders should prioritize advancements in cost reduction and infrastructure development to overcome challenges and capitalize on opportunities in this dynamic market. The focus on scalability and eco-friendly solutions positions fuel cells as a cornerstone of the global energy transition.

Key Benefits of this Report:

- Insightful Analysis: Gain detailed market insights covering major as well as emerging geographical regions, focusing on customer segments, government policies and socio-economic factors, consumer preferences, industry verticals, and other sub-segments.

- Competitive Landscape: Understand the strategic maneuvers employed by key players globally to understand possible market penetration with the correct strategy.

- Market Drivers & Future Trends: Explore the dynamic factors and pivotal market trends and how they will shape future market developments.

- Actionable Recommendations: Utilize the insights to exercise strategic decisions to uncover new business streams and revenues in a dynamic environment.

- Caters to a Wide Audience: Beneficial and cost-effective for startups, research institutions, consultants, SMEs, and large enterprises.

What do businesses use our reports for?

Industry and Market Insights, Opportunity Assessment, Product Demand Forecasting, Market Entry Strategy, Geographical Expansion, Capital Investment Decisions, Regulatory Framework & Implications, New Product Development, Competitive Intelligence

Report Coverage:

- Historical data from 2022 to 2024 & forecast data from 2025 to 2030

- Growth Opportunities, Challenges, Supply Chain Outlook, Regulatory Framework, and Trend Analysis

- Competitive Positioning, Strategies, and Market Share Analysis

- Revenue Growth and Forecast Assessment of segments and regions including countries

- Company Profiling (Strategies, Products, Financial Information, and Key Developments among others.

Fuel Cell Market Segmentation:

By Type

- Polymer Electrolyte Membrane Fuel Cells (PEMFC)

- Solid Oxide Fuel Cells (SOFC)

- Molten Carbonate Fuel Cells (MCFC)

- Phosphoric Acid Fuel Cells (PAFC)

- Direct Methanol Fuel Cells (DMFC)

- Alkaline Fuel Cells (AFC)

- Others

By Application

- Stationary Power Generation

- Transport

- Portable Power

- Material Handling Equipment (MHE)

- Auxiliary Power Units (APUs)

- Others

By End-User Industry

- Automotive & Transportation

- Utilities / Power Generation

- Industrial

- Commercial & Residential

- Healthcare

- Military & Defense

- Telecommunications

- Logistics & Warehousing

- Aerospace & Aviation

- Others

By Geography

- North America

- USA

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Taiwan

- Others

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

2. MARKET SNAPSHOT

- 2.1. Market Overview

- 2.2. Market Definition

- 2.3. Scope of the Study

- 2.4. Market Segmentation

3. BUSINESS LANDSCAPE

- 3.1. Market Drivers

- 3.2. Market Restraints

- 3.3. Market Opportunities

- 3.4. Porter's Five Forces Analysis

- 3.5. Industry Value Chain Analysis

- 3.6. Policies and Regulations

- 3.7. Strategic Recommendations

4. TECHNOLOGICAL OUTLOOK

5. FUEL CELL MARKET BY TYPE

- 5.1. Introduction

- 5.2. Polymer Electrolyte Membrane Fuel Cells (PEMFC)

- 5.3. Solid Oxide Fuel Cells (SOFC)

- 5.4. Molten Carbonate Fuel Cells (MCFC)

- 5.5. Phosphoric Acid Fuel Cells (PAFC)

- 5.6. Direct Methanol Fuel Cells (DMFC)

- 5.7. Alkaline Fuel Cells (AFC)

- 5.8. Others

6. FUEL CELL MARKET BY APPLICATION

- 6.1. Introduction

- 6.2. Stationary Power Generation

- 6.3. Transport

- 6.4. Portable Power

- 6.5. Material Handling Equipment (MHE)

- 6.6. Auxiliary Power Units (APUs)

- 6.7. Others

7. FUEL CELL MARKET BY END-USER INDUSTRY

- 7.1. Introduction

- 7.2. Automotive & Transportation

- 7.3. Utilities / Power Generation

- 7.4. Industrial

- 7.5. Commercial & Residential

- 7.6. Healthcare

- 7.7. Military & Defense

- 7.8. Telecommunications

- 7.9. Logistics & Warehousing

- 7.10. Aerospace & Aviation

- 7.11. Others

8. FUEL CELL MARKET BY GEOGRAPHY

- 8.1. Introduction

- 8.2. North America

- 8.2.1. By Type

- 8.2.2. By Application

- 8.2.3. By End-User Industry

- 8.2.4. By Country

- 8.2.4.1. USA

- 8.2.4.2. Canada

- 8.2.4.3. Mexico

- 8.3. South America

- 8.3.1. By Type

- 8.3.2. By Application

- 8.3.3. By End-User Industry

- 8.3.4. By Country

- 8.3.4.1. Brazil

- 8.3.4.2. Argentina

- 8.3.4.3. Others

- 8.4. Europe

- 8.4.1. By Type

- 8.4.2. By Application

- 8.4.3. By End-User Industry

- 8.4.4. By Country

- 8.4.4.1. United Kingdom

- 8.4.4.2. Germany

- 8.4.4.3. France

- 8.4.4.4. Spain

- 8.4.4.5. Others

- 8.5. Middle East and Africa

- 8.5.1. By Type

- 8.5.2. By Application

- 8.5.3. By End-User Industry

- 8.5.4. By Country

- 8.5.4.1. Saudi Arabia

- 8.5.4.2. UAE

- 8.5.4.3. Others

- 8.6. Asia Pacific

- 8.6.1. By Type

- 8.6.2. By Application

- 8.6.3. By End-User Industry

- 8.6.4. By Country

- 8.6.4.1. China

- 8.6.4.2. Japan

- 8.6.4.3. India

- 8.6.4.4. South Korea

- 8.6.4.5. Taiwan

- 8.6.4.6. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

- 9.1. Major Players and Strategy Analysis

- 9.2. Market Share Analysis

- 9.3. Mergers, Acquisitions, Agreements, and Collaborations

- 9.4. Competitive Dashboard

10. COMPANY PROFILES

- 10.1. Ballard Power Systems

- 10.2. Plug Power Inc.

- 10.3. FuelCell Energy, Inc.

- 10.4. Bloom Energy Corporation

- 10.5. Cummins Inc.

- 10.6. Ceres Power Holdings plc

- 10.7. Doosan Fuel Cell Co., Ltd.

- 10.8. SFC Energy AG

- 10.9. Panasonic Corporation

- 10.10. Toyota Motor Corporation

11. APPENDIX

- 11.1. Currency

- 11.2. Assumptions

- 11.3. Base and Forecast Years Timeline

- 11.4. Key benefits for the stakeholders

- 11.5. Research Methodology

- 11.6. Abbreviations

LIST OF FIGURES

LIST OF TABLES